The German merit order has been pushing deeper into the country's gas-burning generation stack with the NCG and Gaspool front-month contracts at the end of last week moving below the level at which a highly efficient 59pc gas-fired plant can compete with an older lignite-fired unit, while even medium-efficient gas units would be able to replace most of Germany's coal-fired plants next month at prevailing prices.

Daily average gas burn at 3.9GW has exceeded average coal-fired generation at 3.7GW on 1-17 March, preliminary data from German research institute Fraunhofer Ise show. Fossil-fuel power generation has come under pressure from a sustained period of high wind power generation, rising output from hydropower plants and unseasonably mild weather conditions across most of central west Europe, with the latter limiting demand for electric heating in the wider region.

But rising coal-to-gas fuel switch potential in the German day-ahead market — the NCG day-ahead has held comfortably below the level at which a 55pc-efficient gas-fired unit can compete with a 40pc-efficient coal plant so far this month — and with combined heat and power (CHP) generation dominated by gas-fired units in Germany, power sector coal burn has come under more sustained pressure in week 10 and again last week, on 11-17 March.

Prevailing forward prices suggest that Germany's merit order will push even deeper into gas burning territory in hours or on days with lower renewable power generation in April and persisting downside pressure on the German gas hub has opened the possibility for efficient gas-fired units to compete with old lignite plants next month.

German gas hub prices

Slow German gas withdrawals in recent months — helped by mild weather and quick imports — have weighed on NCG and Gaspool prices from the front of the curve.

The stockdraw has remained slow this month with unseasonably mild weather. NCG and Gaspool prompt prices mostly at a discount to front-summer markets provided little incentive for brisk withdrawals and even encouraged net injections on some days.

Inventories of 121.9TWh yesterday morning were 48.3TWh above the three-year 17 March average. And more mild weather is expected in the coming weeks, which could continue to curb withdrawals and may allow for stocks to open an even wider surplus before the start of the summer.

German storage sites could struggle to absorb as much supply as in recent summers in April-September, even if they are to be completely filled before the start of next winter, which may require power sector gas burn to step up considerably.

That said, NCG and Gaspool April contracts held a discount to third-quarter 2019 markets in recent weeks, which could provide an incentive to load a larger share of injections into next month, in favour of turning down the stockbuild later in the summer.

Gas vs lignite, coal

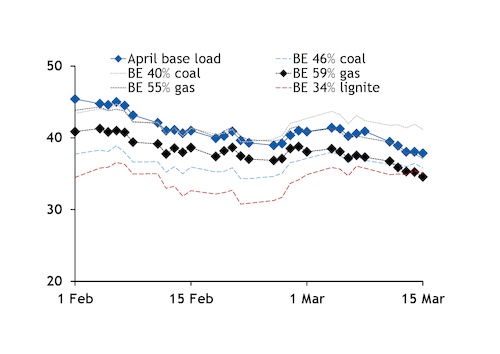

Marginal breakeven costs for 59pc-efficient gas-fired plants in the NCG gas hub area and delivery in April ended the 15 March session at €34.56/MWh while in the Gaspool hub marginal costs stood at €34.05/MWh, based on Argus assessments. This compared with marginal breakeven costs for 34pc-efficient lignite plants at €35.09/MWh, assuming marginal fuel costs of €2.85/MWh. The front-month Gaspool contract edged below the level at which a 59pc-efficient gas plant could compete with 34pc-efficient lignite units only once before this decade, for a number of sessions in March 2010.

Based on confirmed and assumed plant efficiencies of Germany's gas-fired generation stack, installed market-based gas-fired power capacity — excluding units in reserve schemes — with an efficiency of 59pc or more could rise to 4.8GW from 1 April should the 300MW Lichterfelde combined-cycle gas turbine (CCGT) and combined heat and power (CHP) plant start commercial operations as scheduled.

But even if the Lichterfelde start-up is delayed, installed gas-fired capacity of 4.5GW could replace some of the 6.8GW of lignite-fired capacity with an efficiency of 34pc or lower, an analysis of the efficiency of Germany's remaining lignite plants shows.

Most of Germany's lignite plants are operated by German utility RWE and Czech-owned Leag. The firms are likely to have concluded long-term hedges at lower EU ETS prices, and hence more attractive clean lignite spreads and could run their units based on these hedges.

But the plant operators might find incentive to scale back production from their lignite plants in times when wholesale day-ahead or intra-day power prices move below their marginal costs of power generation. Lignite-fired power generation ran at an average of just 8.4GW on 1-17 March, putting lignite burn on track to reach the lowest for any month since at least January 2011, suggesting that plant operators scaled back production.

It would be largely gas-fired plants ahead of coal units that could replace lignite-fired production should plant operators choose to implement optimisation measures in April, especially when depressed day-ahead or intra-day prices weigh heavily on the profitability of lignite plants over a more sustained period. This could force older units off the grid and with cold start-up times for lignite units typically longer than other fossil-fuel plants, gas burn could step in when demand for thermal power generation firms.

In any case, prevailing prices suggest that gas burn will be embedded in the German merit order next month even if lignite units run on long-term hedges with the exception of days with exceptionally high renewable power feed-in and low demand. This is because of strong coal-to-gas fuel switch potential.

The Gaspool front-month contract on 15 March was below the level at which a 59pc-efficient plant could compete with a 46pc-efficient coal unit, the highest efficiency for coal in Germany. And 55pc-efficient gas units in the Gaspool and the NCG gas hub could replace a 42pc-efficient coal plant in the expected merit order for April, at prevailing prices. Germany has an installed market-based gas-fired capacity of around 15.3-15.6GW compared with around 13-14GW of market-based coal-fired capacity with an efficiency of 43pc or lower.

The German April-based load power contract has moved closely in line with the marginal break-even costs of a 55pc-efficient gas-fired plant this month while moving below the breakeven costs for 43pc-efficient coal units on expectations that load hours for Germany's gas-fired fleet will find support from the increasing competitiveness of gas with coal in particular and with lignite to a certain extent in the expected merit order for next month.