Low hydropower stocks have changed market dynamics in parts of Europe this year and some trends seen in the first quarter look likely to continue, at least in the short term.

Strong run-of-river output in France has offset record low hydropower stocks at the beginning of April and helped meet some of the shortfall in neighbouring Spain, with flows switching direction compared with the same time last year. Forward price spreads suggest the trend may continue at least in the short term.

French net power imports totalled 1.69TWh in March, the highest monthly level on record, according to grid operator REE and were around 376.8GWh during the first week of April, while Spain was exporting to France in the same period last year. The Spanish April contract expired at a €9.60/MWh ($10.18/MWh) premium to France, while the second quarter expired €13.35/MWh above the equivalent French assessment, although the spread between the two markets was reversed last year.

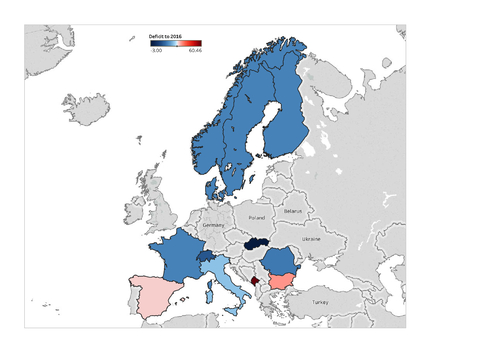

Hydropower reserves in Spain were at their lowest since 2008 at the beginning of April at 10.2TWh of capacity and below the five-year average of 14.5TWh. French hydropower stocks reached a new low at the beginning of April but total hydropower output was mostly unaffected as run-of-river output remained strong.

Lower Spanish hydro reserves could also support power sector gas demand as it did in July 2015 when a heatwave landed and hydropower generation weakened. The 1GW Almaraz nuclear plant is scheduled to be off line from 20 June to 31 July which is also likely to leave more room for gas burn in the power mix.

Strong run-of-river hydropower in France counteracting lower hydro stocks has had a more limited impact on French forward prices. Output from reservoirs accounted for just 2.5pc of the generation mix in March, down from 3.5pc a year earlier. While second and third quarter have held premiums to equivalent 2016 prices, a significant part of the support has come from stronger fuels prices. Weaker hydrological conditions could have an impact later this year if they lead to restrictions on cooling water used for nuclear reactors.

France has retained its usual discount to Italy, where hydropower reserves dropped to a seven-year low, and where hydropower accounts for less than 15pc of the country's demand. The Italian second-quarter contract expired €10.15/MWh and €10.10/MWh higher than equivalent French and Swiss contracts, respectively, little changed year on year, while the third-quarter contract premiums have also been little changed this year.

The government is concerned that low hydro stocks will lead to reduced output in summer and said it may call for some mothballed thermal plants to remain available to the grid. Italian utility Enel's 144MW Genoa 3 and 130MW Bastardo 1 and 2 coal-fired units, and utility A2A's 373MW Chivasso 2 gas-fired plant could remain operational to ensure the safety of the Italian system, deputy economy minister Teresa Bellanova said earlier this year, although the ministry has since authorised the closure of Genoa. Hydropower generation rose by more than one fifth year on year in January at 2.7TWh as demand spiked with cold weather. This combined with weak rainfall to leave reserves at their lowest since at least 2010 at 2.24TWh in February, the last month for which data are available.

Italian peak-load prompt premiums to Hungary are tightening as is normal in the second quarter, but Italian prompt contracts switched to an unusual discount to Hungary at the end of January and early February, as weaker hydrological conditions changed market dynamics in the Balkans. Italy will compete with Hungary and Serbia for power flows through Croatia and Slovenia heading into summer, although Romania is stepping up its role in the second quarter.

Reservoirs and hydropower generation throughout southeast Europe are at strong deficits to 2016, leading to a stark difference in market dynamics compared with last year. Flows have switched direction on some of Hungary's borders — it has been exporting to Serbia this year and has switched to being a net exporter on the Romanian border this month, which has pushed the Romanian front month to an unusual premium to Hungary and tightened its third-quarter discount.

May monthly cross-border capacity from Romania to Hungary sold at less than half the usual level at €0.92/MWh and only €0.40/MWh more than capacity in the opposite direction, suggesting Romania could import more next month if hydropower remains weak, and in particular on days of low wind, as is happening this month.

And Hungary looks likely to continue exporting to Serbia at least in the short term as Serbian state-owned utility EPS has been a buyer since the end of October last year and continues to issue near-term purchase tenders, while EPS was a seller throughout the second and third quarters last year as hydrological conditions were significantly stronger. Hungary-Serbia May cross-border capacity sold at its highest monthly level this year at €0.95/MWh. Hydropower strengthened unexpectedly in the first quarter last year, which saw the Hungarian Hupx spot deliver at €26.42/MWh in February, after the contract expired at €40.25/MWh as the front month. In neighbouring Croatia, utility Hep — usually a seller — issued a buy tender for June, July, and third-quarter base load last month, indicating expectations for a tight supply-demand balance over the summer.

Nuclear maintenance throughout the Balkans will increase the potential for spot price spikes in the second and third quarters, in particular if hydropower remains weak and the weather turns hot and dry. No maintenance is planned at Slovenia's 696MW Krsko nuclear plant this year as it runs on an 18-month fuel cycle. A 1GW unit at the Kozloduy nuclear plant in Bulgaria is due to go off line over 22 April-12 June, a 700MW unit at Cernavoda in Romania will go off line over 6 May-5 June, and 500MW of capacity at Paks in Hungary is due to go off line over 31 July-27 September.

But expectations for an increase in run-of-river hydropower generation in Turkey led grid operator Teias to not offer any monthly import capacity on its borders with Bulgaria and Greece for the second consecutive month in May, in a move to avoid oversupply, especially in Turkey's western and Marmara regions. Turkish spot prices have turned out at a premium to Bulgaria this month, despite the lack of inflows on that border, but Turkey has still been exporting to Bulgaria, with power likely transiting through to higher-priced markets in Serbia, Romania and Hungary.

The Exist day-ahead settled below expectations at TL108.98/MWh (€28.06/MWh) and TL118.48/MWh in March and April last year, respectively. Prices turned out below expectations as hydropower strengthened during the spring months, meaning there was less room for thermal power plants in the merit order. But colder weather this year has delayed snowmelt, and hydro generation dropped by 1.4GW year on year to 7.6GW in March and has been running at 7.7GW in April, compared with 9.7GW last year. Scheduled hydro output by Euas, which owns 13.2GW of the total 27GW of installed hydro capacity, dropped to 3.1GW and 3GW from 3.7GW and 4GW, respectively, in March and April. Euas may be storing water to replenish its stocks after increasing its generation in winter to make up for curtailments to gas use for power plants.

Flows have also switched their typical direction in countries in and bordering the Nordics, where hydropower stocks are at their lowest for at least four years. Norway, typically a net exporter, turned out a net power importer from Denmark throughout February and March for the first time for at least two years. Below-average hydropower stocks in Sweden saw the country's monthly net exports to Finland and Poland fall by around 30pc and 12pc year on year in the first quarter, although low hydro stocks in November last year had pushed Sweden to the unusual role of net importer on its Polish border while exports to Finland dropped sharply. Nordic forward prices all hold strong discounts to Polish equivalents, but the lower hydro stocks have helped the Nordic third-quarter 2017 Nasdaq OMX base-load contract retain a premium to the equivalent 2016 contract, with support also coming from the planned decommissioning of Sweden's 475MW unit 1 at the Oskarshamn nuclear unit at the end of June.