Fertilizer freight rates on certain routes have begun to rise following a steady slide since mid-March, adding to the pressure on some phosphates suppliers' fob levels.

Freight rates to ship phosphates posted the largest weekly increase in recent months, as fuel oil bunker prices have begun to rise since hitting lows at the end of April.

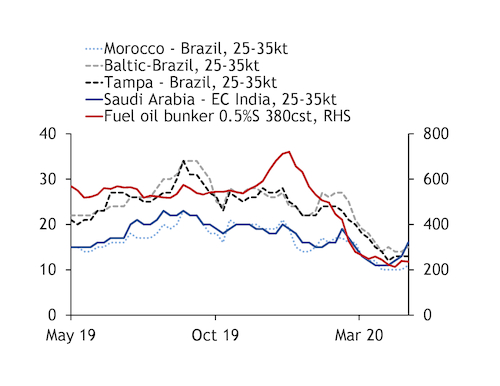

Argus has examined the cost of shipping in four key phosphate trade routes — three to Brazil from Morocco, US and Baltic ports, and one from Saudi Arabia to India. The average cost of freight rose by $1.25/t this week, Argus calculates, up from modest rises of $0.25/t in the previous two weeks.

Phosphate fertilizer suppliers' netbacks had benefited from the Covid-19 outbreak, because of the ensuing fall in trade, the collapse of energy prices and the accompanying drop in freight rates. Rates across these four routes had fallen for seven weeks in a row prior to the recent rises, from the second half of March to the end of April. The cost of shipping fell by an average of $9.50/t in those seven weeks.

But fertilizer shipments to major markets continued, despite lockdowns. Many governments designated fertilizers of strategic importance in the wake of the coronavirus outbreak, given the role they play in the food chain.

But finished phosphates freight rates began to reverse this trend at the start of May, as marine fuel prices ticked up. The price of bunker fuel, with a 0.5pc sulphur content, in Singapore — widely viewed as a benchmark of marine fuel prices (see chart) — began to pick up from the end of April, supporting freight rates.

A continued rise in freight rates could threaten suppliers' fob levels in the coming weeks, as major phosphate import markets Brazil and India seek to secure tonnage. Phosphate prices have been under pressure since the end of March, and competition is ramping up in these markets among suppliers, particularly east of Suez.

But MAP prices in Brazil increased this week to $300-308/t cfr, following a drop from the mid/high-$320s/t cfr in the second half of March. Another round of MAP purchases is expected to pick up in the coming weeks ahead of application to the safra soybean crop in September, and the window for purchases is closing. But any modest rise in cfr levels could equally be cancelled out by increasing freight rates.