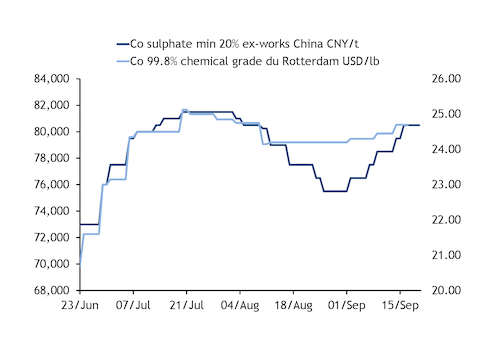

Strong cobalt demand outlooks and a concentrated supply chain are rattling pricing conventions for the latest round of long-term contracts (LTCs), with discounts narrowing significantly and some trading firms pushing to charge premiums in a shift that one described as "unprecedented".

"Discounts [to cobalt metal indexes] are disappearing, and we hope to achieve a premium even on long-term contracts that lock in supply. Our metal inventories are at an all-time low, so there is no rush to sell. Hydroxide payables are still above 90pc, so why should anyone give discounts this year?" a producer said. "Everybody is expecting the market to tighten so we will not be locking in small premiums and small margins."

One trading company said LTC discounts of up to 10pc have since narrowed to about 1pc, and they might need to introduce a premium for those customers aiming to lock in material for further down the line — another growing trend as several consumers seek longer-term commitments of up to three years rather than the traditional single-year LTCs, and with ever-increasing volumes requested for future years. Meanwhile, another producer said they had already achieved slight premiums on 6-12 month contracts with Asian buyers.

Bottlenecks loom

European and US ambitions for regional battery supply chains could hit a major stumbling block when it comes to refining cobalt chemicals, further contributing to the tight market outlook on future years.

One cobalt supplier said large volumes — 50-100t/month — of chemical-grade metal are being requested on long-term contracts beyond 2023. The supplier said they are "shocked" by how rapidly customers expect their consumption to ramp up, not to mention the assumption that so much additional supply can be made available so quickly.

If Europe is to consume this much cobalt sulphate in the coming years, the region may need to look more closely into building more facilities that can produce it, particularly given that it is problematic to transport cobalt sulphate long distances because of how it reacts to moisture. More sulphate production will require more cobalt metal of a suitable quality to dissolve in sulphuric acid — squeezing an already-tight market for briquettes and broken-cathode material. The use of hydroxide in Europe — as an alternative approach — is problematic because of environmental issues. Other projects under development in Brazil and Scandinavia also may require briquettes, which in combination with other European and North American developments, may result in several thousand tonnes of additional demand in the coming years.

Global briquette supply totalled about 6,300t last year, based on production at Canada's Sherritt, Australia's Minara and Madagascar's Ambatovy plants. While there are several giga-factories in development and cobalt mines are expanding in the Democratic Republic of the Congo and other global locations, cobalt chemical refining is still largely centred in China.

"Some original equipment manufacturers have started to understand this [cobalt refining bottleneck], but public bodies are still too focused on mines," a developing cobalt sulphate producer said.