A rise in European TTF gas prices along the forward curve has widened the spread between US and European LNG prices to 2029, as damage to Qatari export infrastructure diminishes the prospect of LNG oversupply.

Iran's attacks on QatarEnergy's (QE) 77mn t/yr Ras Laffan LNG export terminal, the largest in the world, damaged trains with a combined 12.8mn t/yr of capacity. Traders are now factoring in QE's expectations that it will take three to five years to repair the trains and also the likelihood that 48mn t/yr of expansions at Ras Laffan due to begin later this decade will be delayed. This would keep long-term US LNG contracts profitable overseas to the end of the decade and reduce the chances of cargo cancellations in the US.

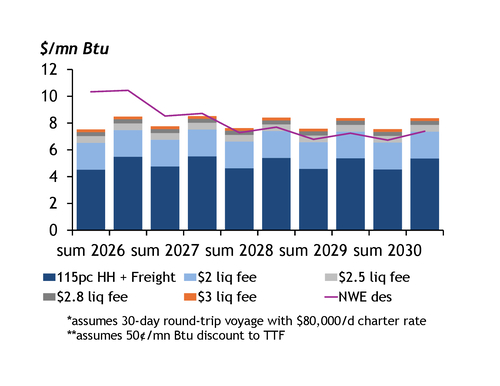

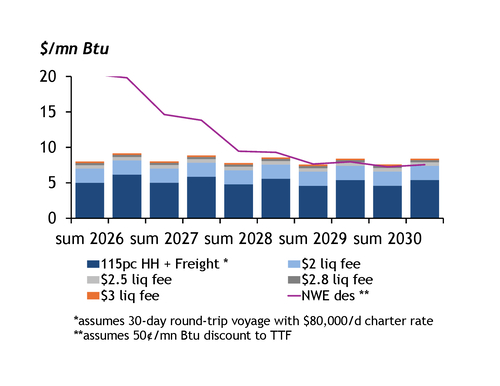

Prior to the loss of Qatari supplies, the forward curve reflected an LNG surplus beginning in 2027, which would have minimised the downward delivery tolerances in the annual delivery plans between US terminal operators and their customers. The elevated TTF curve now has US LNG term contracts with $3/mn Btu liquefaction fees profitable in delivered European LNG markets until winter 2029-30, assuming freight rates of $80,000/d and a 50¢/mn Btu delivered discount to the TTF (see 19 March graph). Before the war lifted the curve, the value of those contracts exceeded European LNG prices in summer 2028, which would have raised the possibility of US LNG customers pushing for lower delivery tolerances or even cargo cancellations (see 27 February graph).

This pricing environment would probably drive a more urgent global need for US LNG. US developers are adding 117.9mn t/yr of capacity between now and the end of 2030, on top of the 139mn t/yr already in operation.

Prices at the Henry Hub, the US gas benchmark and primary variable cost in US LNG contracts, are insulated from volatility in the global market. The 2027-calendar strip for Nymex gas delivered to the Henry Hub was $3.92/mn Btu on 20 March, within this winter's range of $3.64-4.07/mn Btu. US LNG contracts typically comprise 115pc of the Henry Hub plus a liquefaction fee of $2-3/mn Btu.

By contrast, TTF prices for 2027 were up to $15.61/mn Btu on 20 March, from $8.60-9.97/mn Btu this winter before the war broke out, Argus data show. Some traders are now hedging their TTF-Henry Hub exposure further along the forward curve because of the wider spread, market participants said.