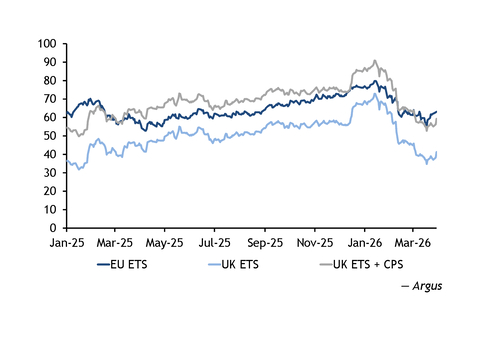

The benchmark front-year contract under the UK emissions trading scheme (ETS) significantly widened its discount to the EU throughout the first quarter of this year, as scant signs of progress on efforts to link the two systems reduced previous optimism of an impending price convergence, and the UK supply-demand balance remained more relaxed than the EU's.

The UK ETS front-year contract closed on average around £14.75/t of CO2 equivalent (CO2e) below its EU counterpart in Argus assessments over January-March, having widened from a low of £6.85/t CO2e in mid-January to a high of £25/t CO2e this week.

This compares with an average discount of £13.50/t CO2e in the fourth quarter of last year, within a narrower range of £8.80-17.70/t CO2e, and is the widest average discount for any quarter since the first quarter of last year's £21.80/t CO2e.

Linkage plans squeeze spread

The UK's discount to the EU began to narrow significantly after the UK government said in a statement in March 2025 that it was "actively considering" linking its ETS back to the EU's, a position confirmed by both sides as part of their common understanding agreement concluded between the UK and EU at a summit in May last year.

The markets separated in 2021 as part of Brexit, and while the EU-UK trade and co-operation agreement signed as part of that process committed the two sides to giving "serious consideration" to linking the schemes, no meaningful steps towards a link had previously been taken.

The news dramatically narrowed the spread between the two markets, with the UK front year's discount to the EU squeezed to an average of £9.90/t CO2e in the second quarter of 2025. A linkage would logically lead to a convergence of UK and EU ETS prices, as the allowances issued under the two schemes would be fungible.

Momentum on the issue continued over the remainder of the year and early 2026, as the European Commission set out in July its recommendation for the legal basis for linkage negotiations, approved by member states in November, and the first round of negotiations kicked off in January.

But while the EU and UK said that they aimed to complete talks on the linkage before the next UK-EU summit in 2026, no date for the meeting has been set, and updates on negotiations have in recent months been notable by their absence.

Recent events have likely pushed ETS linkage down the political agenda, whether on the domestic front — Keir Starmer's position as UK prime minister came under pressure in February — or internationally, most notably as the US-Iran war sparked a renewed energy crisis.

EU supply-demand balance tightens

Changes to key fundamentals have also tightened the EU ETS supply-demand balance this year in a way that hasn't been seen in the UK ETS, further widening the spread between the markets.

Both the maritime and aviation sectors will have to pay for 100pc of their 2026 emissions covered by the EU ETS, after shipping was phased gradually into the system over the previous two years and free allocations for airlines were phased out. Free allocations for industrial sectors covered by the EU's carbon border adjustment mechanism (CBAM) are also scheduled to start decreasing from this year alongside the measure's introduction, and some CBAM-exposed firms have begun purchasing EU ETS allowances to hedge their expected costs.

The UK also ended free allocations for aviation under its ETS this year. But the maritime sector will not be included at all until July this year, and then will only apply to domestic voyages until at least 2028. And the UK CBAM does not launch until 2027.

The UK ETS authority also opted late last year not to introduce a supply adjustment mechanism to the scheme, which could otherwise have reduced allowance auction volumes if the total number of allowances in circulation surpassed a certain level.

Short-term fundamentals diverge

The US-Iran war has prompted further divergence between the markets. EU ETS prices rallied in tandem with natural gas prices on the expectation that more coal plants would come on line, increasing the carbon intensity of the bloc's generation mix and therefore compliance demand for allowances. The UK, by contrast, has no operational coal-fired units.

This has seen carbon costs even for power generators become consistently cheaper in the UK than the EU for the first time since February last year, despite the UK's additional £18/t CO2e carbon price support (CPS) charge on the sector. The discount of the UK ETS to the EU including the CPS stood at an average of around £3.25/t CO2e in March.

UK ETS prices could find some support over the coming weeks from last-minute buying in the run-up to the scheme's annual compliance deadline on 30 April, upward pressure that will not be seen in the EU ETS with its 30 September deadline, which could narrow the spread between the markets in the short term.

But participants will otherwise be awaiting more clarity on linkage. And with the Middle East conflict dragging on, the approach of local elections in the UK and the planned EU ETS review in July, plenty of factors could slow completion of the talks.