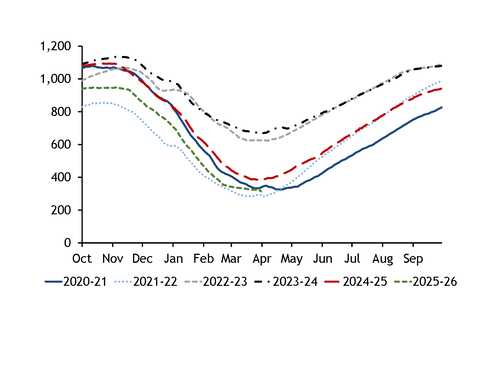

Europe faces its toughest gas injection season since 2022, because stocks are at a four-year low and the continent must secure LNG cargoes at a time of tightened global supply.

Underground inventories across the EU were at just 314TWh on 1 April, equivalent to 27.7pc of capacity. This was down from 387TWh a year earlier and well below the three-year average of 561TWh for the date. Bridging the 73TWh year-on-year deficit is equivalent to the bloc securing an additional 4.7mn t of LNG — or roughly 65 standard-sized cargoes.

But securing supply to fill storage will be harder this year because the Middle East conflict has tightened the global LNG market considerably. Europe will be unable to import LNG from Qatar or the UAE — which made up about 7pc of its LNG supply in 2025 — while the strait of Hormuz remains closed. And European buyers may have to compete for Atlantic basin cargoes with Asian buyers, some of which are already scrambling to secure replacement cargoes for lost Mideast Gulf supply ahead of their peak cooling demand season.

Given these challenges, the European Commission has encouraged member states to make use of the flexibility built into the EU storage regulation and aim to have 80pc of capacity filled between 1 October and 1 December instead of the headline 90pc target. The legislation also permits an additional 10-percentage point deviation under persistent unfavourable market conditions or technical constraints. Some countries, such as Austria and Latvia, are granted larger derogations, for instance because their storage capacity exceeds domestic consumption. EU member states already made use of these derogations and additional flexibility under the regulation last year. Stocks peaked at 949TWh on 13 October, equivalent to 83.2pc of capacity.

If countries that targeted 90pc last year adjust their 2026 requirement to 80pc, and once existing derogations are factored in, the effective EU-wide target would drop to 68.5pc, compared with 71.2pc last year. But even in this case, the EU would need to inject 469TWh this summer, up from 425TWh last year — a difference equivalent to 39 LNG cargoes. And even then, national obligations, security of supply considerations and the level of national regulatory intervention may have a greater impact than compliance with the EU's storage law.

Inverted market signals

Unfavourable summer-winter price spreads have discouraged storage capacity bookings, further complicating the task of refilling storage sites. Differing levels of state intervention will mean uneven filling rates across the bloc this summer.

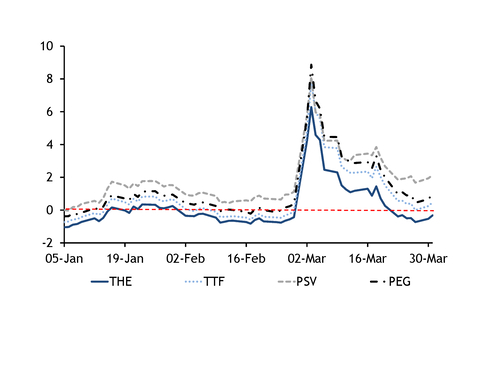

Summer 2026 contracts at the Dutch, German, Italian and French hubs jumped above corresponding winter 2026-27 contracts at the start of March just after the Middle East war broke out. By the time the summer 2026 contract expired at the end of March, only the German summer price had slipped back to a discount to the front winter.

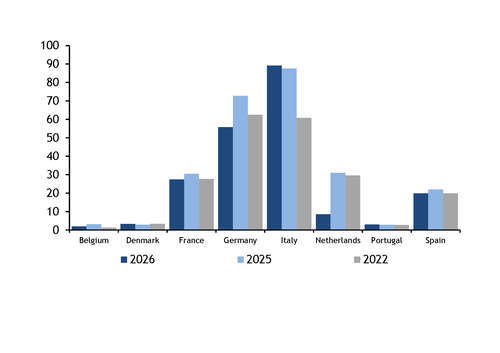

Germany has the EU's largest working gas capacity at 245TWh — 22pc of the bloc's total. German sites ended the winter at only 21pc of capacity, the lowest for any year since 2018.

Argus estimates that firms had booked roughly 63pc of German storage capacity for April 2026-March 2027 by the start of April. Near-curve prices will need to maintain a discount to the front-winter contract to spur further bookings and injections, if Germany is to reach its national fill target of 70pc.

The German energy ministry has told Argus repeatedly that it will leave storage filling to the market, arguing that state intervention would pass on huge costs to consumers. Other EU countries have instead opted to offer incentives to ensure inventories are replenished.

Italy, the EU's second-largest capacity holder with 203TWh, has announced an incentive mechanism aimed at offsetting the unfavourable market conditions, consisting of bonus payments to firms based on their end-of-October stocks. And the Netherlands — with a technical capacity of 144TWh — has strengthened its state backstop for this injection season. State-owned EBN is empowered to fill up to 80TWh, a much higher mandate than the 25TWh last summer.

France's regulated storage system should also ensure sites are filled regardless of summer-winter spreads. Firms have contractual obligations to fill booked capacity, and all capacity has been booked thanks to reserve costs being set at zero for 2026-27 capacity, with storage operators compensated through transmission tariffs. France has 126TWh of technical storage capacity.

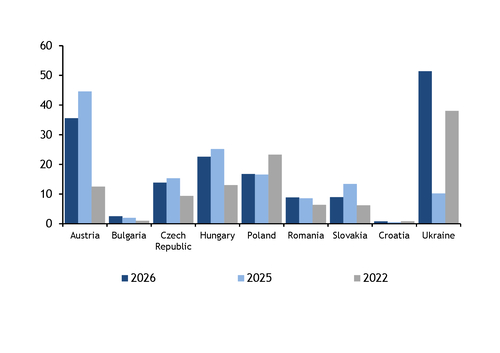

Countries in central and eastern Europe may also be able to only partly rebuild gas stocks this summer. But a higher share of long-term pipeline deliveries and domestic supply within their supply mix could provide a more stable injection profile than in markets with heavier LNG exposure. Stocks in Austria, Bulgaria, Croatia, the Czech Republic, Hungary, Poland, Romania and Slovakia were at a combined 102TWh on 1 April, 21.4TWh lower than a year earlier and the lowest for the day since 2022. This equated to 29pc of capacity, higher than the EU average (see CEE stocks graph).