Physical crude differentials in Europe are poised for a rebound in the coming weeks, traders said, as the effects of recent price containment measures wear off.

Prices for many grades relative to the North Sea Dated benchmark hit all-time highs in the first half of April, with acute shortages of crude caused by the effective closure of the strait of Hormuz. Many grades reached more than $20/bl premiums to Dated, eroding refinery economics. The situation changed from mid-April, as governments began to introduce price mitigation measures including drawing down inventories of products and using up crude from floating storage.

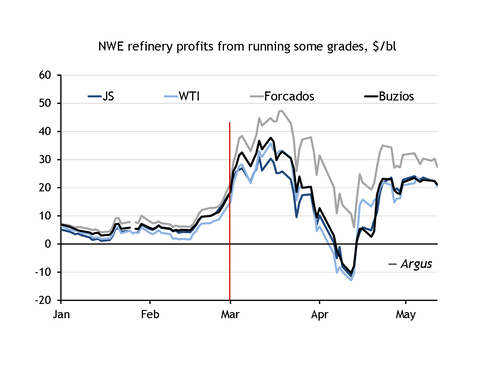

Argus' calculations show returns for a northwest European refinery from running Europe's staple grade US WTI, Norway's medium sour Johan Sverdrup and Brazilian medium sweet Buzios, all flipped negative in the first half of April because of record differentials and expensive freight (see graph). The calculation uses the value of grades in terms of oil products that an average refinery can produce, or Refinery Gate Values (RGVs), and deducts the cost of crude and freight.

Only some west African grades, like Nigerian medium sweet Forcados, remained profitable because of superior product yields.

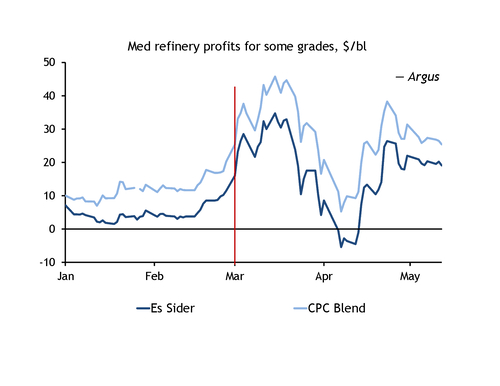

Refining profits in the Mediterranean region dipped, with running Libyan Es Sider becoming loss-making, and profits from running Caspian CPC Blend shrinking.

Crude differentials then dropped to near pre-war levels in May, with two measures notably making a difference, traders said. China reduced imports by nearly 2mn b/d by cutting runs, using commercial stocks and even reselling some cargoes back to the spot market, and the US crude stock releases resulted in around 400,000 b/d of discounted crude from the country heading to Europe for arrival in May and June.

Trader said these two factors have shielded the crude market from even higher prices and crashed prompt prices. Refinery profits have bounced back, and although they are $10-15/bl below March record highs, they are $15-20/bl above January averages for many grades.

Now, any prompt excess has been depleted, and traders said June is going to get tight and prices will climb again, with some evidence noticeable in cargoes trading further ahead.

Far out prices at premiums

Europe's market can be roughly divided into two tiers in terms of the timing of crude trade — prompt, for loading/delivery 2-4 weeks ahead, and cargoes due 1-2 months ahead. Prices for the latter are already at substantial premiums to prompt supplies.

Freight-adjusted UK Forties crude, which typically trades promptly, averaged an almost $9/bl premium to CPC Blend cif Augusta, which trades a bit further ahead, in the second half of April, signalling a shortage of prompt supply. But since 5 May, prompt Forties has been $1.20/bl below CPC Blend.

Similarly, WTI for prompt delivery was largely at parity to supplies arriving more than one month ahead in mid-April, but is now at a $4/bl discount on average.

Traders said crude differentials will be not as high as they were in April, but said pre-war differentials are unsustainable as long as Hormuz remains closed.

The Dated-to-frontline contracts (DFL) for May and June, which reflect the strength of physical market relative to the futures in a given month, also suggest physical prices are likely to increase. The May DFL fell to $2-$3/bl in early May, but was above $5/bl on 13 May. The June DFL rose from $4/bl in early May to above $5/bl. For comparison, the front-month DFL was negative in February, when the European market looked oversupplied, and the second-month DFL was well below $1/bl in the same period.