The Netherlands may miss its domestic fill level target as gas injections must triple from their current rate, which is unlikely given the Grijpskerk site's unbooked status. But the country could reach its EU-mandated fill level target — which could possibly be relaxed — even if Grijpskerk remains empty.

The sluggish start to the Dutch stockbuild is narrowing the scope for the country reaching its government-mandated 80pc — or 115TWh — fill level target by 1 November. Combined net injections into the country's four seasonal storage sites have averaged 208 GWh/d over 1-21 May, half the three-year average of 401 GWh/d and well below the year-earlier level of 476 GWh/d. This has left Dutch sites at a 13pc fill level, holding 18TWh of gas. If the country aims to reach the national 1 November target, it must nearly triple injections from their current rate and hold them at 595 GWh/d until that date to fill an additional 97TWh into sites.

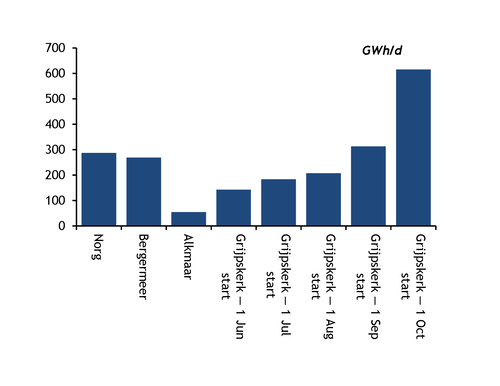

This seems extremely unlikely given the current level of storage bookings and lack of incentives to inject. There are currently no injections at the Grijpskerk and Alkmaar sites, while Bergermeer has seen net withdrawals of gas over the past month because of a prolonged cold spell. The only injections happening in the country are at Norg.

To reach the target, Norg and Bergermeer, the two largest sites, must each inject in the range of 270–290 GWh/d, while Alkmaar — which cannot begin injections until 1 August — needs to inject around 54 GWh/d across its 92-day window. This is theoretically achievable, but leaves little room for prolonged outages or weak market incentives to inject.

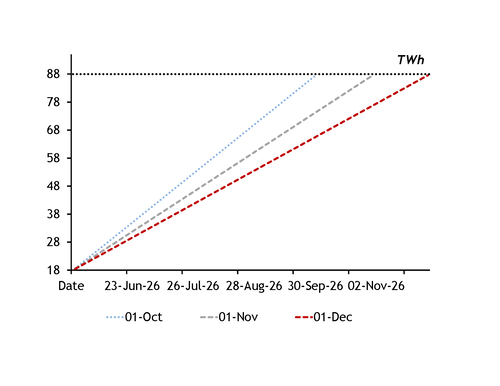

The most uncertain variable is Grijpskerk. If operator Nam allocates the space over the next week and injections begin on 1 June, injections would have to average 142 GWh/d, against a maximum injection rate of 160 GWh/d, until 1 November. A July start narrows the scope significantly, after accounting for the 1-19 July planned works at the site, pushing the required injection average to around 183 GWh/d — beyond what the site can physically deliver. Any start date from August onwards makes hitting Grijpskerk's 80pc target impossible at maximum injection rates (see table).

Nam has been unable to allocate space at the Grijpskerk site because of little market interest. The issue could arise from the fact that any firm that is interested in Grijpskerk has to book its entire storage space due to the site's physical constraints, according to Nam.

EU target potentially offers more leeway

The Netherlands could still technically meet its EU-mandated fill level, even if Grijpskerk remains empty, but injections must still rise by at least 80pc from their current rate.

The Netherlands has to hit a 74pc fill level target during 1 October-1 December under EU regulation, and the target could even be lower, as the European Commission encouraged member states to use a 10-percentage-point relaxation, which could potentially bring the target down to 64pc. A 64pc fill level target would be much more achievable, as it could be achieved at a 430 GWh/d injection rate for a 1 November deadline or a 362.5 GWh/d rate for a 1 December deadline. But both these rates still require injections to pick up significantly from their current rates.

In any case, a 64pc fill level would also provide more flexibility for a decision to be made on Grijpskerk. At the latest, injections at the site could begin on 27 August if the target is reached by 1 December.

But the 64pc fill level target allows Nam to not have to allocate space at Grijpskerk. If Norg and Bergermeer fill to around 80pc, the 64pc EU target can be reached without Grijpskerk. This is physically feasible, but it shifts 15.26TWh of storage burden onto both sites, which both sites could sustain given their maximum injection capacities.

Also, a 64pc fill level target means the Netherlands would have to fill around 88TWh — just 8TWh less than EBN's filling mandate of 80TWh. If EBN covers that level, only 8TWh would be left for the market, which could happen later this summer if storage spreads normalise. And as long as the market is not incentivised to fill, EBN will continue filling storage sites, as it injects when market-based, spread-driven injections are insufficient.

The TTF May price closed at a €1.78/MWh premium to the following winter on 21 May. The spread gets wider further down the curve, peaking at its widest point in August at €2.04/MWh.

| Grijpskerk scenarios | GWh/d | |||

| Start date | Net injection days | Avg needed | pc of max capacity (160 GWh/d) | Feasible |

| 1 Jun 2026 | 134.0 | 142.4 | 89pc | Yes - tight |

| 1 Jul 2026 | 104.0 | 183.5 | 114pc | No - exceeds max cap |

| 1 Aug 2026 | 92.0 | 207.4 | 130pc | No - exceeds max cap |

| 1 Sep 2026 | 61.0 | 312.8 | 196pc | No - exceeds max cap |

| 1 Oct 2026 | 31.0 | 615.5 | 384pc | No - exceeds max cap |

| Argus | ||||