The EU rapeseed sector is facing a second year of low supply from the world's top exporters, at a time when the impact of unfavourable weather on crops in parts of Europe could increase the bloc's reliance on imports.

Cold weather in spring and several heatwaves in Europe in the past two months could result in an EU rapeseed crop of below 20mn t in a low-case scenario, down from the 20.4mn t currently forecast by Argus analytics for the 2026-27 marketing year that started on 1 July.

A 20.2mn t EU rapeseed crop for the 2025-26 marketing year meant that the bloc was largely able to offset lower supply and uncompetitive prices from its top global suppliers. But the EU's import options in 2026-27 remain limited for the second year in a row.

Australian canola output could fall to 6.35mn t in the 2026-27 marketing year starting on 1 November from 7.76mn t a year earlier, while exports could decline by 500,000t on the year to 4.9mn t in the upcoming season, Argus projected.

A strong El Nino weather pattern that could develop this growing season poses a high risk to yields from dry, hot weather in Australia's main canola-producing regions. El Nino has not yet caused any adverse effects, and growing conditions have been favourable so far, supported by adequate rainfall, but yields may still fall as a result of lower fertiliser application in recent months, owing to Australia being one of the countries most affected by fertiliser supply disruptions and price increases caused by the US-Iran war.

Australia may also direct rising volumes of its canola to China in the coming months. At present, only some state-owned firms in China are permitted to import Australian canola, but market participants expect China to soon open the market to private crushers as well. If so, China could increasingly switch from Canadian canola to Australian origin, potentially leaving less Australian supply available to the EU.

As for Canada's exports to the EU, supply is uncertain because of Canada's growing domestic crush sector, supported by strong demand for canola oil from US biofuel producers. Argus forecasts Canada's canola exports at 8mn t in the 2026-27 year starting 1 August, down from 8.5mn t a year earlier, despite expectations of higher output next season, as producers struggle to keep up with growing demand from crushers.

Ukraine is expected to see just a marginal increase in rapeseed output and exports in 2026-27, according to Argus forecasts. Export duties and strong demand from Ukrainian crushers — market participants expect the crush sector to process 1.5mn t of rapeseed this year, even higher than last year's surge to 1.2mn t — mean the domestic market could absorb all additional rapeseed.

As a result, EU imports of Ukrainian rapeseed oil (RSO) could continue to rise. The EU imported 523,000t of RSO in 2025-26, up from 320,000t a year earlier. Ukraine accounted for the bulk of the volume at 354,000t, European Commission data show, with the EU being the main export destination for Ukrainian RSO.

EU rapeseed imports at four-year low in 2025-26

EU rapeseed imports fell to 5.4mn t in 2025-26, down by 29pc on the year and the lowest since 2021-22, commission data show.

EU imports from all its main suppliers fell, with receipts from Australia — the largest source of imported rapeseed to the EU — showing the steepest decline (see table). A relatively large rapeseed crop within the EU made imports less attractive, with Australian canola particularly uncompetitive against the EU's own rapeseed earlier in the season and later in spring 2026, when the US-Iran war pushed up freight rates. Australia directed canola elsewhere, stepping up exports to the UAE and restarting shipments to China at the end of 2025.

The EU's imports of Ukrainian rapeseed also fell sharply, after an export duty on Ukrainian rapeseed introduced in September 2025 redirected more of the country's production to the domestic crush sector.

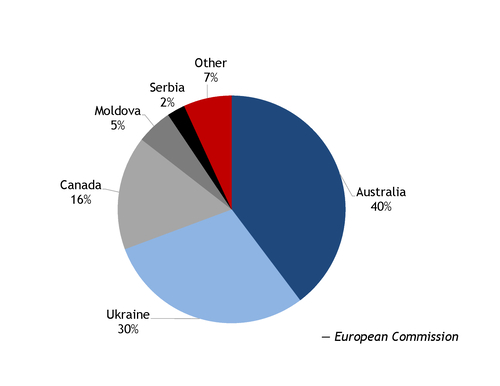

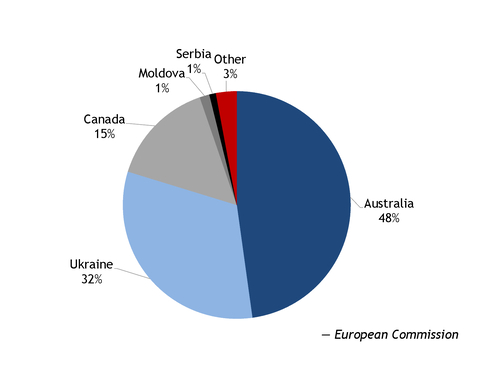

EU imports of Canadian canola also declined in 2025-26, but Canada increased its share of the EU rapeseed market by around one percentage point at the expense of Australian and Ukrainian market shares (see charts). Canada is typically the EU's third-largest source of imported rapeseed, and competitive prices in December prompted a wave of purchases to top up supply within the bloc.

Some smaller exporters, including Moldova, also increased their supplies to the EU in 2025-26. Moldovan exports to the bloc could rise further this season because the country is expecting a larger crop.

| EU rapeseed imports | 000t | ||

| 2025-26 | 2024-25 | ±% | |

| Australia | 2,143 | 3,608 | -41 |

| Ukraine | 1,596 | 2,410 | -34 |

| Canada | 874 | 1,132 | -23 |

| Moldova | 274 | 105 | 161 |

| Serbia | 138 | 70 | 97 |

| Other | 369 | 222 | 66 |

| Total | 5,394 | 7,547 | -29 |

| — European Commission | |||