New EU oil sanctions spark spiralling complexity

New EU sanctions on Russian oil that come into effect on 21 January could have the second-greatest impact on oil trade since the invasion of Ukraine — but they are also some of the most complicated. They are generating a wide range of interpretations, with private self-sanctions leaving the actual letter of the sanctions far behind, and could spark sharp price movements in the coming weeks.

What are the new sanctions?

The sanctions are billed as banning oil products made from Russian crude, regardless of where the refining happens. They could have the biggest impact on oil trade since the EU banned direct crude and product imports from Russia in 2022-23. But like most sanctions, the new measures do not quite live up to their title.

The EU will only apply its new sanctions to products classed under customs code CN2710, meaning many are exempt. One exempt category is defined by containing more than 50pc aromatic molecules, under code CN2707. This includes reformate, a gasoline blending component, as well as most residual fuel oil. Another key exempt product is bitumen, used to surface roads and classed under code CN2713.

Private actors are mostly aligned in applying their rules only to CN2710, including the Energy LEAP group. But some price reporting agencies — not including Argus — are excluding all products, regardless of customs code, made from Russian crude from their platforms and assessments. And the same material can shift between exempt and non-exempt categories through blending, either inside or outside the EU, leading to careful discussion of fringe cases between EU oil companies in recent weeks.

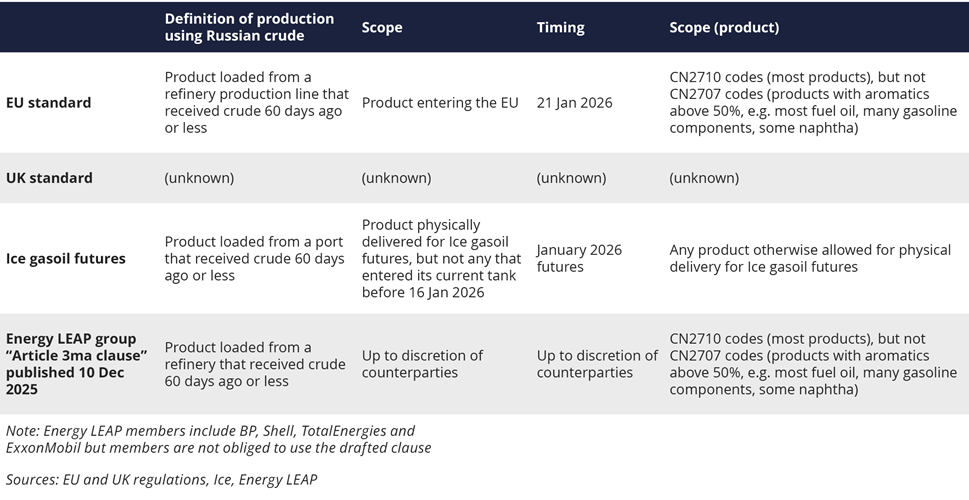

Divergence between the sanctions and private self-sanctioning measures widens with the definition of a product made from Russian crude.

No laboratory test can verify whether products were refined from Russian crude, so the EU defines its target products as those that load within 60 days of receipt of Russian crude at the same facility. The EU is prepared to distinguish between production lines at the same refinery — if the product loads from a production line that has not received Russian crude in the last 60 days, it can be shipped to the EU.

But some private actors are taking a much more restrictive line. The Energy LEAP group of large oil companies published an example contract clause that refuses to distinguish between production lines at the same refinery, and the Intercontinental Exchange (Ice) refuses even to distinguish between refineries at the same port. Each individual company is writing its own rules, somewhere on this spectrum. For example, TotalEnergies has placed bids in public platforms with restrictions in terms of port, rather than refinery or production line.

Finally, the greatest question mark of all sits just across the North Sea — the UK says it will ban products made from Russian crude in 2026 but has not given a date nor details. Product price spreads could develop between the UK and EU in the meantime, and even within the UK if some companies self-sanction in anticipation.

Europe's scattered rules on oil product origin

How are refineries outside the EU reacting?

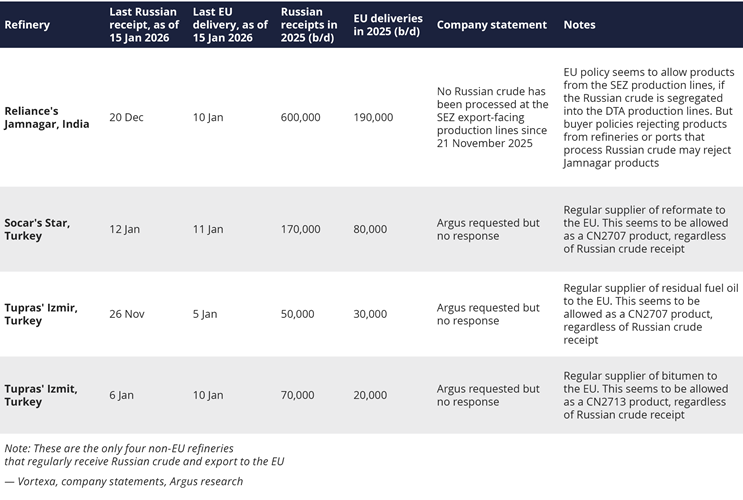

The impact of the sanctions on markets depends largely on how non-EU refineries react. Four — one in India and three in Turkey — will be significantly affected, being the only ones that both imported Russian crude regularly since 2022 and exported products regularly to the EU. Many other refineries process Russian crude, especially in India and China, but they never or hardly ever export products to the EU.

The four affected refineries have been divided in their reactions. Indian firm Reliance’s Jamnagar says it has stopped running Russian crude in the section that exports products to the EU. In Turkey, Tupras’ Izmir has not said anything, but appears to have stopped running Russian crude at the time of writing. Meanwhile, Tupras’ Izmit and Socar’s Star continue to run Russian crude as before.

Reactions of key non-Russian, non-EU refineries to new EU sanctions

- Reliance’s 1.4mn b/d Jamnagar refinery in India

Reliance’s 1.4mn b/d Jamnagar refinery in India, the largest in the world, is at the centre of these sanctions in practice. It has been the largest user of Russian crude in the world since 2023, using around 480,000 b/d on average — although that is a minority of its total crude usage. Peak usage was around 700,000 b/d in the second and third quarters of 2025. Reliance is also one of the largest external suppliers of diesel and jet fuel to the EU.

Reliance publicly stated that its export-facing segment — called the SEZ — would receive no more Russian crude “from 20 November”. The company said that would mean none of the refinery’s product exports were made from Russian crude from 1 December. EU rules would seem to regard 20 January as the transitional date, being 60 days after the last Russian crude receipt. If EU customs authorities are satisfied, then products loading from the SEZ at Jamnagar from 20 January onward could be exported to the EU.

But self-sanctioning means that some private companies look set to reject Reliance SEZ products, on the basis that the same refinery — Jamnagar as a whole — or the same port has received Russian crude less than 60 days before the product loaded. One or two diesel buyers in Europe in December even began to require non-Indian origin, traders told Argus, although this would be a very imprecise translation of the sanctions at best.

The other segment of the Jamnagar refinery — called the DTA — is big enough to process all the Russian crude Reliance has received even at the highest volumes, so there may be no change in overall Russian crude receipts at Jamnagar. But its overall Russian crude receipts dropped to a 19-month low of 350,000 b/d in December, half their summer peak. - Tupras’ 238,000 b/d Izmir and 227,000 b/d Izmit refineries in Turkey

Tupras is Turkey’s largest refiner and one of the world’s largest users of Russian crude. It mainly serves domestic Turkish fuel demand but intermittently exports surplus products to destinations including the EU. Tupras has not made any public statement about strategy in response to the new EU sanctions. Nor has it responded to Argus queries on the subject.

The 227,000 b/d Izmit refinery continues to receive Russian crude, so is likely to stop exporting most products to the EU when the sanctions take effect. But as of 15 January, analytics firms Vortexa and Kpler agree that no Russian crude has arrived at the 238,000 b/d Izmir refinery since 26 November. If the Izmir refinery does not receive any more Russian crude, then on 26 January it could start loading products that would be allowed in the EU under the new sanctions, because it would have been 60 days since the last Russian receipt.

The EU received around 600,000t of refined products from Tupras refineries in the fourth quarter of 2025, according to Vortexa tracking. Most of that was diesel, residual fuel oil and bitumen. The latter two of those are both likely unaffected by sanctions, because of their customs codes — unless EU buyers choose to avoid them. One senior EU market participant told Argus in recent weeks that he expects most buyers to avoid residual fuel oil made from Russian crude, even though it is exempt from the sanctions.

With one rejecting and the other still taking Russian crude, the Izmir and Izmit refineries may be able to reallocate some EU customers for non-EU customers, maybe even preserving Tupras’ sales overall. Tupras’ strongest export margins are probably earned on its diesel, which has been trading at least $30/bl higher than residual fuel oil in Europe in recent months. Tupras can meet EU diesel standards, which are relatively strict and high value, and the company may see a significant financial reward for preserving diesel sales to the EU. -

Socar’s 220,000 b/d Aliaga ‘Star’ refinery in Türkiye

The Star refinery operated by Azeri state-owned Socar continues to receive Russian crude, taking Russian Urals as recently as 12 January from the tanker Marjorie, according to Vortexa tracking. Socar’s Turkish office is now handling product sales from the Star refinery, European buyers say. The firm’s Geneva office only handles products that are not derived from Russian crude.

The Star refinery can probably continue exporting reformate — a high-octane gasoline blending component — to the EU, because it is more than 50pc aromatics and therefore classed under CN2707. That product may be blended into gasoline after entering the EU. Reformate from the Star refinery on the tanker MRC Beliz discharged in the EU on 11 January, according to Vortexa tracking.

How is this moving markets?

In the short term, the EU could witness sudden and large changes in supply and prices.

The most exposed market is jet fuel, which is subject to the sanctions as a CN2710 product. EU jet fuel supply has tightened structurally in recent years, as the bloc’s demand has grown while many of its refineries have closed. Reliance is a dominant supplier of the EU’s jet fuel imports, with around 15pc market share. Jet fuel prices are therefore highly sensitive to the divergence between EU rules that appear to allow Reliance supply, and decisions by private companies to self-sanction by rejecting it. There may soon be two prices for jet fuel in the EU — one for those who buy from Reliance and one for those who do not. If the spread is wide enough, and if EU customs are seen to allow Reliance products to discharge, pressure could mount on those choosing to pay the higher price.

If 20 November were the date on which Reliance’s SEZ segment stopped receiving Russian crude, then only its loadings from 20 January onward would be allowed in the EU, in theory. These would only begin to arrive in the EU from late February, given tanker journey times. Between the sanctions taking effect on 21 January, and the first of those arrivals in late February, Reliance product may not be allowed in the EU under any interpretation of the rules.

One tanker to watch is the Suezmax Aesop, carrying 140,000t of diesel from Jamnagar. It was off Namibia heading north on 15 January, according to Vortexa, and was on track to reach northwest Europe at the start of February. It could easily discharge in west Africa or the UK, for example. But it could be offered to EU buyers, with possibly interesting results.

Beyond jet, the likely loss of supply from Tupras’ Izmit and Socar’s Star refineries will require some adaptation by EU diesel markets. They supply around 2.5mn t/yr of diesel and other gasoil, or around 5pc of those products entering the EU from external suppliers.

To some extent, Izmit and Star diesel could be replaced with diesel from Tupras’ Izmir refinery, and from the Middle East — especially if Izmit and Star redirect their exports to sanction-free markets such as Africa, displacing Middle Eastern diesel.

Diesel looks less vulnerable than jet to supply disruption because EU diesel demand is declining. The EU may not need to replace the entire 5pc of supply that Izmit and Star previously supplied. Around 2-3pc of German diesel demand is expected to be substituted with renewable fuels in 2026, because that country is ending the double-counting of renewables towards greenhouse-gas emission reduction targets. New diesel car sales in Italy fell by 35pc year on year in 2025, according to the Italian automotive industry association. These are both examples of patterns seen across western Europe.

In Russian crude markets, volumes may prove more resilient than prices. Tupras has been using Russian crude for no more than a third of its feedslate at each refinery, so the same combined Russian volume could perhaps run entirely through Izmit. And at the right price, there are refiners around the world that are likely to be willing to use any Russian crude that Reliance stops taking. But that price looks lower than it once did. Together with other recent sanctions, such as those targeting Russian firms Rosneft and Lukoil specifically, these new EU sanctions seem to have depressed the price of Russian crude. Urals fob Primorsk has been trading around $25/bl cheaper than North Sea Dated since November, roughly twice the discount of the preceding months.

Author name: Benedict George, Editor, Argus European Products, Oil

{kind=link}

{kind=link}