Iron ore’s future in balance as China jettisons benchmark

China has adopted new indexes to price iron ore imports, divorcing the physical market from the reference underpinning a vast futures ecosystem.

China has adopted new indexes to price iron ore imports, divorcing the physical market from the reference underpinning a vast futures ecosystem. This forms part of a broader reframing of the pricing mechanism that is under way: a change in typical grades has disrupted long‑term offtake agreements and altered the basis of futures; China is consolidating buying power; and futures markets have grown large enough to influence the physical markets on which they depend.

Index pricing — previously of limited interest to anyone not in the industry (and indeed many in it) — has in recent months been drawing coverage from mainstream financial news outlets as producers adjust pricing formulas in negotiations with Chinese buyers. This has largely focused on the move away from the long-used index that settles financial contracts, replaced by alternatives, including the growing use of Argus as part of an index average.

These changes affect long-term contracts in China. But similar trends are playing out in the spot market that sets references used globally in iron ore procurement. Here too, a growing share of cargoes used in price formation reference indexes or combinations other than the futures settlement index.

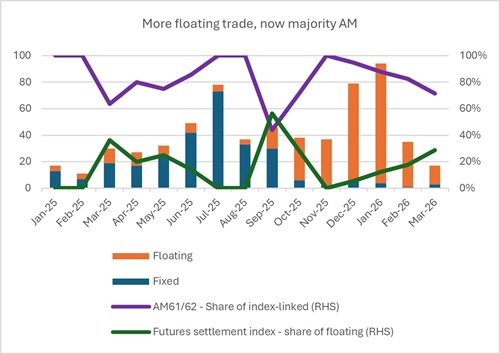

Since October, more than 80pc of spot deals reported to Argus have been index‑linked, with nearly 85pc of these tied to the Argus/Mysteel average (see chart).

Why now?

Despite the recent focus, the shift itself is not new but reflects a long-running push from Chinese mills to reduce reliance on a single settlement index.

Basket pricing — the averaging of two or more references — has been on the agenda for years. And as China’s purchasing power has consolidated, negotiating this outcome has become easier. The result has typically been a combination of domestic and international references, most commonly the Argus/Mysteel basket.

Baskets have become a midpoint position at a time when proposals for a full shift towards yuan-denominated portside pricing have started to circulate. Its proponents argue that portside trade is liquid, high frequency and rooted in fixed-price physical activity. And the desire for a grounding in regular and observable physical trade plays into unease with the influence of overseas financial markets on iron ore prices.

As commodity futures volumes grow far beyond underlying physical trade, pricing can drift away from the value of real cargoes and begin to reflect the needs of financial participants rather than the physical market. The effects of this are already visible in iron ore. January’s shift on the futures settlement index from 62pc to 61pc left companies with long-dated exposure scrambling to adjust to a timetable aligned with the requirements of the financial market.

Participants also worry that a single settlement index capturing a short window of end-of-day activity leaves only a narrow physical connection to a much larger and increasingly influential financial market. Baskets offer a hedge against any one individual index methodology.

However, severing the link with financial markets creates a paradox. Price risk management is now an essential part of the iron ore pricing mechanism, as is the role of floating trade in price formation. Yet changing the index in physical contracts brings increased basis risk and weakens the connection anchoring financial markets to real trade.

Getting match fit

This has set the stage for a multi-year discussion around the future of iron ore pricing. While there is clear appeal in China for portside pricing in local currency, elsewhere price formation will require a US dollar-based system with tools to manage price risk. The two can co-exist but the current fragmentation — in which a futures market continues to settle on a seaborne reference with rapidly diminishing physical usage — is unsustainable.

A sustainable seaborne mechanism would refocus price formation on physical market activity and restore a clearer link between physical exposure and cash-settled risk management. The debate between China and its suppliers is ultimately about ensuring that real cargoes reflecting market prices set the baseline for both physical and paper pricing. Liquidity is central to that.

Seaborne spot liquidity is already stronger than in most bulk commodities. The challenge now is to build enough confidence and data around a reference that reflects the trade both sides are using. The most widely used reference in the spot market has become the Argus/Mysteel average, which a growing share of long-term contracts are settling against. It is the point at which Chinese preferences for a more representative basket meet producers’ need for continuity and international basis alignment. All-day volume-weighted indexes average the maximum amount of available spot trade at a time when the physical industry is interested in increasing spot liquidity even further.

The missing link

With mining companies and mills tracking several indexes, and with trade tensions affecting quality differentials, daily basis risk between indexes is rising. Managing this without a hedge aligned to the price that most physical supplies reference is increasingly difficult. The Argus/Mysteel average already exists as a single licensable number. Given how central it has become to physical trade, a cash-settled contract against this combined reference would give the market a tool that matches the basis on which iron ore is increasingly priced.

Without moves in this direction, the risk is that a growing financial market will continue to set terms by default. That could hardwire a settlement price shaped by a shortened end-of-day window against which few cargoes are now priced. At a time when buyers and sellers are pushing toward the same goal — indexes grounded in broader, more liquid physical spot activity — this is not an outcome either side wants, and one that risks hardening positions, pushing both sides of the market toward more extreme stances.

Author name: Oscar Tarneberg, VP, Business Development, Metals and Tim Hard, SVP, Energy Transition, Metals