Rising costs, a rebound in the Australian dollar and weaker iron ore prices are squeezing the margins of Australia's small- to medium-size iron ore producers, as underlined by analysis of Mineral Resources' (MinRes) full-year production results.

MinRes shipped 19.21mn wet metric tonne (wmt) of iron ore from Western Australia in the 2021-22 fiscal year to 30 June, up from 17.21mn wmt the previous year and expects to come inside its cost guidance of A$80-104/wmt ($56-73/wmt). At its average realised price of A$103.90/wmt for 2021-22 the iron ore operations are likely to make a cash profit. But 2022-23 could be a tougher proposition, with costs set to keep rising, the Australian dollar strengthening and the iron ore price outlook weaker.

This combination of obstacles will be felt across Australia's iron ore industry, although the large-scale producers — BHP, Rio Tinto, Fortescue and Roy Hill — are starting from a much lower cost base largely because of their rail networks that deliver ore to port. MinRes and the rest of the smaller exporters, which combined accounted for around 30mn t of Australia's 871mn t of iron ore exports in 2021, are in a much more precarious position.

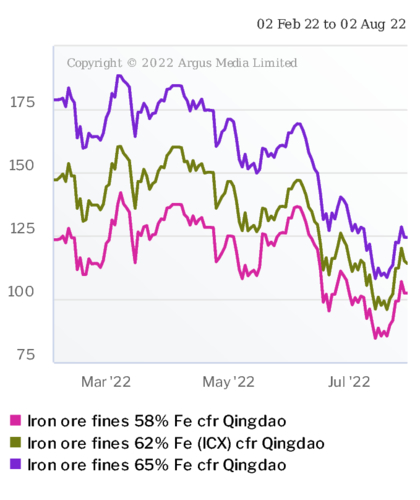

For MinRes, which ships around a 57.5pc Fe ore, and other low-grade producers the narrowing discount that has accompanied the slide in iron ore prices since 1 April has been a small bonus but it does little to offset the other issues.

The Argus 58pc Fe price fell to an average of $94.89/dry metric tonne (dmt) in July from $121.69/dmt in the April-June quarter. The Australian dollar, which had eased from $0.75 to the US dollar on 1 April to $0.68 on 1 July, recovered to $0.70 on 1 August with the prospect of more interest rate rises adding upwards pressure. A stronger Australian dollar puts pressure on iron ore mining margins by increasing A$ denominated costs relative to US$ denominated received prices.

Inflationary effect

The large interest rate rises, albeit from a low base, are designed to curb inflation in Australia, which hit 6.1pc during April-June and is expected to peak at 7.75pc for October-December. Inflation in the mining industry is running ahead of baseline Australian inflation because of its high energy consumption. This is particularly the case for mid-tier iron ore mining firms most of which truck iron ore large distances from mine to port. Wage increases, labour shortages and the high price of key consumables are also adding to costs.

Considering the 22pc drop in the average Argus 58pc Fe price in July compared with April-June alone, MinRes needs its costs for the month to come in at the bottom of its A$80-104/wmt guidance for 2021-22 for its iron ore operations to breakeven. This seems unlikely given the other obstacles.

MinRes is fortunate to run a profitable mining service division that has allowed it to operate its iron ore mines through the cycle before. But others are not so lucky and even MinRes has previously run its mines more slowly once they start making a loss.

MinRes will release its full-year financial reports on 29 August.

| MinRes iron ore | (mn wmt) | ||||

| Apr-Jun '22 | Jan-Mar '22 | Apr-Jun '21 | FY 2021-22 | FY 2020-21 | |

| Production | |||||

| Yilgarn | 2.08 | 2.02 | 2.70 | 9.27 | 11.00 |

| Pilbara | 2.95 | 2.87 | 2.54 | 11.22 | 8.47 |

| Total | 5.03 | 4.89 | 5.24 | 20.49 | 19.47 |

| Sales | |||||

| Yilgarn | 2.13 | 2.13 | 3.03 | 8.68 | 10.50 |

| Utah Point | 2.56 | 2.54 | 2.21 | 10.53 | 6.77 |

| Total | 4.69 | 4.67 | 5.24 | 19.21 | 17.27 |

| Source: MinRes | |||||