The competitiveness of recycled polymers compared with their virgin equivalents in Europe have extended records in April, as exports of plastic and petrochemical feedstocks from the Middle East remain highly disrupted.

Demand for recycled polymers increased, particularly for less-demanding and cost-saving applications. But many recyclers are concerned about the longer-term implications of the entirely supply-driven price rally on their demand and margins.

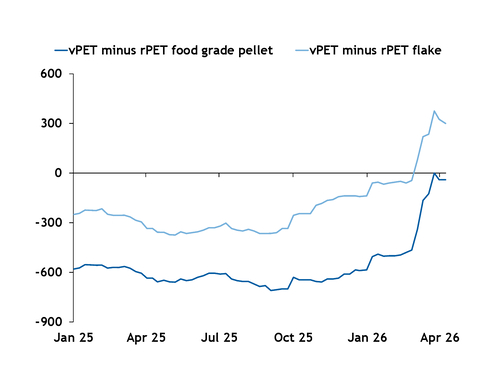

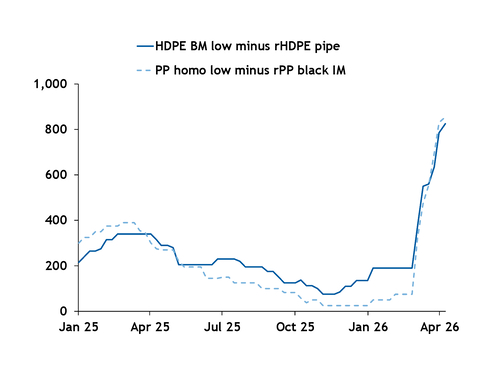

Based on spot prices, the current cost comparison between virgin and recycled polyolefins and polyethylene terephthalate (PET) is the most skewed in favour of recyclates as a cheaper option since Argus began assessments. Data start in 2022 for polyolefins and in early 2024 for PET, when Argus launched its delivered northwest Europe PET resin spot assessment.

In polyolefins, buyers of low- and linear low-density polyethylene (LDPE and LLDPE) on the spot market to make black or dark-coloured films could save more than 50pc by using recycled pellets, notwithstanding additional processing costs. Manufacturers of corrugated HDPE pipes could save 40-50pc by switching to recycled material.

For PET, rPET flakes are now €300/t less expensive than virgin PET, having only become cheaper — for the first time in two years — in early March.

Higher virgin polymer prices result from growing tightness and rising production costs, particularly because of disruption to exports of polyethylene (PE), polypropylene (PP), crude oil and naphtha through the strait of Hormuz. Recyclate prices have risen to a much lesser extent than the virgin equivalents, as the direct effects of the war on recycled supply chains has been much less.

Higher demand for recyclates is particularly prevalent in non-packaging applications with fewer technical barriers to material substitution. It can also be seen in more complex applications where converters may not have maximised their allowance for recycled content in 2025 and early 2026 because of cheap virgin polymer prices.

The increase in demand is leading recyclers to target margin improvement, following a long period in which cheap virgin polymers squeezed profitability in the industry. Margins for rPET, rHDPE pipe and rLDPE/LLDPE have increased since the start of the war. Margins for rPP have not yet gained by much, owing to rising feedstock costs, but more upward pressure on rPP pellet prices is likely in the coming weeks.

Downstream demand at risk

Recyclers may be benefitting from geopolitical turmoil in the short term, but many are concerned about the longer-term effects.

Unlike in the Covid-19 pandemic, when virgin polymer prices rose in part because of higher consumer spending power, price inflation arising from the war is likely to negatively effect demand. The latest S&P Global eurozone construction Purchasing Managers' Index (PMI) survey showed the most pronounced fall in new orders since October, with firms pointing to surging energy prices as a key factor. Consumer confidence in the EU27 countries hit a 2.5-year low in March, Eurostat data show.

Converters are concerned about their ability to pass through the recent cost increases within supply chains. Many downstream customers may not yet have seen the full extent of the increases, which are passed down the chain with a delay. Some converters said they are at a juncture, where some production lines would need to be stopped if downstream buyers are unwilling to pay higher prices.

Recyclers are already facing higher energy costs, with tighter global natural gas supply because of Emirati and Qatari LNG outages. European gas and electricity price increases have been capped since the start of the conflict by higher year-on-year supply from elsewhere, relatively warm recent temperatures and market expectation of a return to 'normal' supply in the coming months. In a scenario where a ceasefire is agreed and supply starts to normalise within the next four to six weeks, Argus Consulting projections suggest Europe can avoid a significant storage deficit into the winter. But the risk of major tightness increases the longer the war continues, and the risk of low EU natural gas storage levels heading into next winter is a concern for the recycling industry, with gas-fired generation setting the marginal power price in most of Europe.