PVDF demand to increase chlor-alkali consumption

PVDF demand to increase chlor-alkali consumption

The demand growth of polyvinylidene fluoride (PVDF) is dependent on lithium-ion batteries for battery-operated electric vehicle (EV) demand and stationery electrical storage. Argus forecasts global lithium-ion battery demand in EVs to reach 3.8GWh by 2034 from 0.7GWh in 2023. EV sales are expected to rise at an average growth rate of 10pc in the next 10 years reaching more than 46mn units.

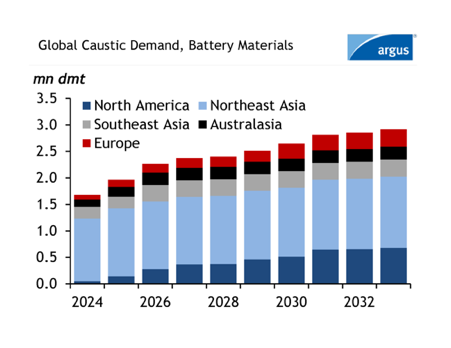

Global caustic soda demand into battery materials for leading regions is shown in the figure. Argus’s latest caustic soda analytics forecast explains an exponential rise in caustic soda consumption for battery material processing. Global caustic soda consumption in the processing of lithium hydroxide, lithium carbonate, cathode materials and recycled black mass was at 1.5mn dmt in 2023 and is expected to reach 3mn dmt in 2033 at a CAGR of 10pc in the first five years.

The relationship between chlor-alkali products and battery materials is gaining focus in the market. With increasing Lithium-based battery capacity globally, demand for associated battery materials is expected to rise. Among the other components of the Li-ion battery stack, PVDF plays an important role as a binder and separator coating, optimizing energy storage efficiency and reducing battery weight in EVs.

PVDF utilizes caustic soda and chlorine in its production at different stages. Primary feedstock includes vinylidene chloride or vinylidene fluoride, which are derivatives of caustic soda and chlorine.

Some significant developments in PVDF capacity are taking place in North America and Northeast Asia. Belgian chemical company Solvay entered into a joint venture with Mexico-based PVC producer Orbia to build the largest production facility of battery-grade suspension PVDF in North America with a capacity of 20,000 t/yr. Commercial production is expected to start in 2026 and the expected caustic soda and chlorine demand can be 8,000 t/yr and 12,000 t/yr respectively.

Solvay has doubled its capacity in Changshu, China in the past five years and raised its capacity in France by 35pc reaching 35,000 t/yr making it the largest production site in Europe. Another major producer French chemical company Arkema increased production capacity by 50pc last year at its Changshu site in China.

Japan-based producer Kureha is undergoing expansion at its Iwaki site in Japan, having a production capacity of 6,500 t/yr. The expansion is in two phases, first is a new capacity of 8,000 t/yr and another 2,000 t/yr in the second phase by debottlenecking resulting in a total capacity of 20,000 t/yr by 2026.

This article was created using data and insight from Argus Caustic Soda Analytics and Argus Battery Materials.

Spotlight content

Related news

Brazil's chemical industry decries new US tariffs

Brazil's chemical industry decries new US tariffs

Sao Paulo, 22 July (Argus) — Brazil's chemical industry association Abiquim said the newly confirmed 25pc US tariff on Brazilian exports is unjustified, arguing the measure targets a sector in which the US already holds a trade surplus and could increase costs for US manufacturers. The US exported about $11.5bn of chemicals to Brazil in 2025 and imported around $2.1bn, leaving a trade surplus of more than $9bn in favor of the US, Abiquim said. While tariff exemptions cover 493 of the 1,177 chemical HS6 codes and 64-71pc of export value, 684 codes remain subject to the additional 25pc duty. The association estimates the measure could add about $66mn in costs by the end of 2026, or $133mn/yr. Coatings, synthetic textile fibers, soaps and detergents are expected to be among the most affected segments. Abiquim called for the Brazilian government to draw up support measures for companies and to keep negotiating with Washington to expand the list of exempted products. By Isabela Mendes Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Hormuz transits sparse after US-Iran clashes: Update

Hormuz transits sparse after US-Iran clashes: Update

Updates with details throughout London, 12 July (Argus) — Ship transits through the strait of Hormuz fell further following fresh clashes between the US and Iranian militaries over the weekend. US and Iranian forces both expanded their attacks for two consecutive days on Saturday and Sunday, hitting defense targets and, in the case of Iran, resuming attacks on ships and oil infrastructure in the Mideast Gulf. US forces launched another round of attacks against Iran at 22:00 GMT on Sunday, according to US Central Command (Centcom), which oversees Middle East-based US forces. Iran's forces earlier on Sunday targeted Kuwaiti border checkpoints and an offshore oil facility, Kuwait's defense ministry said. Iran's Islamic Revolution Guards Corps (IRGC) said early on Sunday that the strait of Hormuz would be closed until further notice, after the US on Saturday carried out another round of strikes on Iranian military targets. IRGC also claimed that its attacks on a Kuwait-based US military base resulted in US casualties. Centcom disputed the claim. Centcom also disputed Tehran's claim of having shut down Hormuz. "Iran does not control the strait," Centcom said in a social media post. "Traffic is flowing." But visible AIS data from MarineTraffic showed no traffic through the strait, although vessels may be transiting with tracking systems switched off. The growing security risk could limit such attempts and threaten the nascent recovery in Gulf crude and product exports. Iran's forces appeared to have attacked Cyprus-flagged containership GFS Galaxy as it transited the strait of Hormuz via the southern route near Oman on Saturday. The vessel was hit nine nautical miles east of the Omani coast, prompting the crew to abandon the ship in a lifeboat. The lifeboat has since been rescued by local authorities, the UK Maritime Trade Operations (UKMTO) said. The vessel appeared to have its AIS tracking switched off at the time. In a separate IRGC statement carried by the Sepah news agency early on Sunday, the force claimed its aerospace arm had struck logistics support centres and refuelling platforms linked to US aircraft carriers at Duqm port in Oman. Duqm is a significant distance from the strait of Hormuz and was hit in the early days of the war, but it has been less severely affected since. Oman's state news agency also reported drone strikes across Musandam governorate, Oman's northernmost governorate. Oman condemned the attacks, the agency added. By John Ollett, Rithika Krishna and Haik Gugarats Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US housing bill to become law without Trump

US housing bill to become law without Trump

Houston, 10 July (Argus) — A bill aimed at improving US housing affordability and approved by Congress is set to become law today without the signature of President Donald Trump, a win for the homebuilding sector. The ROAD to Housing Act contains over 50 provisions designed to improve housing affordability, including streamlining federal permitting processes, expanding access to government lending programs, and creates a pilot home repair grant program to shore up an aging housing stock. The bill has been lauded by the homebuilding sector, which in recent years has struggled with poor consumer demand and elevated borrowing rates that have stymied both mortgage applicants and homebuilders seeking financing for projects. The "landmark legislation would expand housing opportunities for buyers and renters, strengthen homeownership, and help tackle the affordability challenges facing communities nationwide", the National Association of Home Builders said last month. The bill was approved by the US House of Representatives and Senate with broad bipartisan support, but its status has been in limbo for over a week after Trump cancelled a planned signing ceremony scheduled for 24 June in an attempt to force passage of an unrelated bill that would implement voting restrictions. "I will not sign the Housing Bill, which has been fully approved by Congress and sent to the White House, in PROTEST over the fact that the United States Senate is not capable of passing THE SAVE AMERICA ACT," Trump said Friday on social media, referring to the voting bill. Nevertheless, the housing legislation is set to become law Friday. Under the Constitution, bills presented to the president become law in 10 days, excluding Sundays, if no action is taken. The bill officially reached Trump's desk on 29 June. Trump is highly unlikely to veto the bill, a move that Congress likely could override given the legislation's broad support. By Gordon Pollock Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil’s inflation slows to 4.64pc in June

Brazil’s inflation slows to 4.64pc in June

Sao Paulo, 10 July (Argus) — Brazil's inflation slowed to an annual 4.64pc in June, with lower motor fuel prices helping offset higher electricity bills. The consumer price index IPCA decelerated from 4.72pc in May , national statistics agency IBGE said on Friday, after accelerating from 4.39pc in April. Housing costs, appointed as the largest contributors to the monthly gain in the index in June, decelerated to 5.85pc from 6.22pc a month earlier, mostly thanks to electricity bills and tax readjustments for power supply in some southern states. Food and beverage costs, which weigh heavily on the index, contributed the most with the monthly decrease in the IPCA, decelerating to an annual 3.82pc in June from 3.87pc in May. Lower prices for coffee, fruits and meat drove the result, IBGE said. Transport costs slowed to 3.95pc in the month from 4.05pc in May. Lower prices for ethanol, diesel, gasoline and compressed natural gas (CNG) weighed on motor fuel costs, despite an increase in airfares. The annual gain for June was down from 5.35pc in June 2025. Inflation expectations, as calculated by the central bank's Focus survey, remain above target at 5.3pc for 2026 and recently ticked up to 4.18pc for 2027. Brazil's central bank lowered its target rate to 14.25pc in June. By João Curi Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.