PVDF demand to increase chlor-alkali consumption

PVDF demand to increase chlor-alkali consumption

The demand growth of polyvinylidene fluoride (PVDF) is dependent on lithium-ion batteries for battery-operated electric vehicle (EV) demand and stationery electrical storage. Argus forecasts global lithium-ion battery demand in EVs to reach 3.8GWh by 2034 from 0.7GWh in 2023. EV sales are expected to rise at an average growth rate of 10pc in the next 10 years reaching more than 46mn units.

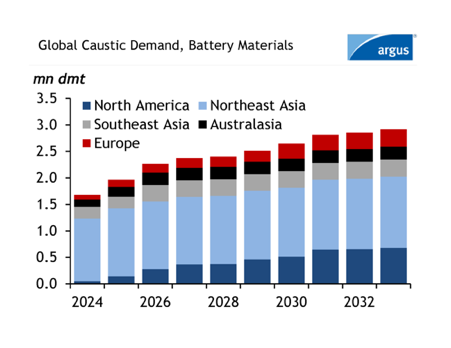

Global caustic soda demand into battery materials for leading regions is shown in the figure. Argus’s latest caustic soda analytics forecast explains an exponential rise in caustic soda consumption for battery material processing. Global caustic soda consumption in the processing of lithium hydroxide, lithium carbonate, cathode materials and recycled black mass was at 1.5mn dmt in 2023 and is expected to reach 3mn dmt in 2033 at a CAGR of 10pc in the first five years.

The relationship between chlor-alkali products and battery materials is gaining focus in the market. With increasing Lithium-based battery capacity globally, demand for associated battery materials is expected to rise. Among the other components of the Li-ion battery stack, PVDF plays an important role as a binder and separator coating, optimizing energy storage efficiency and reducing battery weight in EVs.

PVDF utilizes caustic soda and chlorine in its production at different stages. Primary feedstock includes vinylidene chloride or vinylidene fluoride, which are derivatives of caustic soda and chlorine.

Some significant developments in PVDF capacity are taking place in North America and Northeast Asia. Belgian chemical company Solvay entered into a joint venture with Mexico-based PVC producer Orbia to build the largest production facility of battery-grade suspension PVDF in North America with a capacity of 20,000 t/yr. Commercial production is expected to start in 2026 and the expected caustic soda and chlorine demand can be 8,000 t/yr and 12,000 t/yr respectively.

Solvay has doubled its capacity in Changshu, China in the past five years and raised its capacity in France by 35pc reaching 35,000 t/yr making it the largest production site in Europe. Another major producer French chemical company Arkema increased production capacity by 50pc last year at its Changshu site in China.

Japan-based producer Kureha is undergoing expansion at its Iwaki site in Japan, having a production capacity of 6,500 t/yr. The expansion is in two phases, first is a new capacity of 8,000 t/yr and another 2,000 t/yr in the second phase by debottlenecking resulting in a total capacity of 20,000 t/yr by 2026.

This article was created using data and insight from Argus Caustic Soda Analytics and Argus Battery Materials.

Spotlight content

Related news

US housing bill to become law without Trump

US housing bill to become law without Trump

Houston, 10 July (Argus) — A bill aimed at improving US housing affordability and approved by Congress is set to become law today without the signature of President Donald Trump, a win for the homebuilding sector. The ROAD to Housing Act contains over 50 provisions designed to improve housing affordability, including streamlining federal permitting processes, expanding access to government lending programs, and creates a pilot home repair grant program to shore up an aging housing stock. The bill has been lauded by the homebuilding sector, which in recent years has struggled with poor consumer demand and elevated borrowing rates that have stymied both mortgage applicants and homebuilders seeking financing for projects. The "landmark legislation would expand housing opportunities for buyers and renters, strengthen homeownership, and help tackle the affordability challenges facing communities nationwide", the National Association of Home Builders said last month. The bill was approved by the US House of Representatives and Senate with broad bipartisan support, but its status has been in limbo for over a week after Trump cancelled a planned signing ceremony scheduled for 24 June in an attempt to force passage of an unrelated bill that would implement voting restrictions. "I will not sign the Housing Bill, which has been fully approved by Congress and sent to the White House, in PROTEST over the fact that the United States Senate is not capable of passing THE SAVE AMERICA ACT," Trump said Friday on social media, referring to the voting bill. Nevertheless, the housing legislation is set to become law Friday. Under the Constitution, bills presented to the president become law in 10 days, excluding Sundays, if no action is taken. The bill officially reached Trump's desk on 29 June. Trump is highly unlikely to veto the bill, a move that Congress likely could override given the legislation's broad support. By Gordon Pollock Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil’s inflation slows to 4.64pc in June

Brazil’s inflation slows to 4.64pc in June

Sao Paulo, 10 July (Argus) — Brazil's inflation slowed to an annual 4.64pc in June, with lower motor fuel prices helping offset higher electricity bills. The consumer price index IPCA decelerated from 4.72pc in May , national statistics agency IBGE said on Friday, after accelerating from 4.39pc in April. Housing costs, appointed as the largest contributors to the monthly gain in the index in June, decelerated to 5.85pc from 6.22pc a month earlier, mostly thanks to electricity bills and tax readjustments for power supply in some southern states. Food and beverage costs, which weigh heavily on the index, contributed the most with the monthly decrease in the IPCA, decelerating to an annual 3.82pc in June from 3.87pc in May. Lower prices for coffee, fruits and meat drove the result, IBGE said. Transport costs slowed to 3.95pc in the month from 4.05pc in May. Lower prices for ethanol, diesel, gasoline and compressed natural gas (CNG) weighed on motor fuel costs, despite an increase in airfares. The annual gain for June was down from 5.35pc in June 2025. Inflation expectations, as calculated by the central bank's Focus survey, remain above target at 5.3pc for 2026 and recently ticked up to 4.18pc for 2027. Brazil's central bank lowered its target rate to 14.25pc in June. By João Curi Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US/Canada June PE contracts settle down 15¢/lb

US/Canada June PE contracts settle down 15¢/lb

Houston, 9 July (Argus) — June contracts in the US/Canada polyethylene (PE) market settled down by 15¢/lb, the first decrease since May 2025, as high inventories and lower export prices forced producers to give back some of the 45¢/lb in increases added since the beginning of the US-Iran war. The decline came following extended negotiations with some producers attempting to hold the decline to 10¢/lb. However, when faced with enough competitive offers at a decline of 15¢/lb, even those producers agreed to the lower settlement. The price decline follows steep declines in export prices, which have fallen by more than 30¢/lb, depending upon grade, since late April. Using LLDPE butene as an example, prices are down by 31.35¢/lb since reaching a peak on 17 April. Export prices began to decline in late April as low prices out of China pressured global values. The decline continued in May, as US and Canadian producers added more than 800mn lb to inventories at the end of the month on a combination of healthy production levels and weak domestic and export demand. Market participants expect July contracts to fall further, with some participants saying they expect prices to be down by at least 30¢/lb by the end of the month. The drop of 15¢/lb "is not enough", said one US PE buyer. "It seems like a lot, and it is a lot, but it is not enough." The buyer said that with producers selling to the export market at prices more than 20¢/lb below US contract levels, they are putting domestic customers at a disadvantage to Asian converters. Asian converters can produce finished goods using the lower-priced resin and send that product back to the US, undercutting US converters, particularly for items such as film, which is easily shipped. Some market participants suggested that the recent escalation of the Middle East war could shift sentiment and eventually price direction. If crude prices continue to rise, it could push global PE prices higher, which might allow US producers to raise their prices again. By Michelle Klump Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US home remodeling index rises in 2Q

US home remodeling index rises in 2Q

Houston, 9 July (Argus) — US home remodeling activity inched higher during the second quarter, led by smaller home improvement projects, the National Association of Home Builders (NAHB) said in its quarterly report. The NAHB/Westlake Royal Remodeling Market Index (RMI) rose by 2 points from a year earlier to 61 in the second quarter. The index, measured on a scale of 100, indicates generally bullish sentiment in the sector when readings are above 50. While remodelers wrestle with economic uncertainty and elevated interest rates, demand for home improvement is proving resilient, NAHB said. Slower new construction rates mean older houses and homeowner equity are "keeping the remodeling market relatively strong", even as building material costs rise, NAHB economist Robert Dietz said. The index for small remodeling projects of less than $20,000 rose by 4 points from a year earlier to 74 during the quarter, with projects in excess of $50,000 increasing by 2 points to 64 during the same period. US polyvinyl chloride (PVC) demand was mostly steady during the second quarter, with infrastructure demand for pipe and PVC used primarily in multifamily builds proving resilient, sources said. US contract PVC prices, though, have increased by 20pc since the start of the year, largely fueled by supply constraints stemming from US-Iran war. This is making planning more difficult for remodelers already constrained by high borrowing costs. By Gordon Pollock Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.