PVDF demand to increase chlor-alkali consumption

PVDF demand to increase chlor-alkali consumption

The demand growth of polyvinylidene fluoride (PVDF) is dependent on lithium-ion batteries for battery-operated electric vehicle (EV) demand and stationery electrical storage. Argus forecasts global lithium-ion battery demand in EVs to reach 3.8GWh by 2034 from 0.7GWh in 2023. EV sales are expected to rise at an average growth rate of 10pc in the next 10 years reaching more than 46mn units.

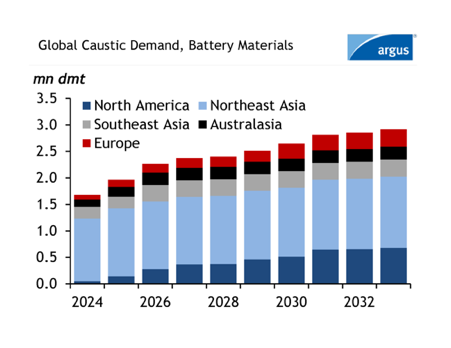

Global caustic soda demand into battery materials for leading regions is shown in the figure. Argus’s latest caustic soda analytics forecast explains an exponential rise in caustic soda consumption for battery material processing. Global caustic soda consumption in the processing of lithium hydroxide, lithium carbonate, cathode materials and recycled black mass was at 1.5mn dmt in 2023 and is expected to reach 3mn dmt in 2033 at a CAGR of 10pc in the first five years.

The relationship between chlor-alkali products and battery materials is gaining focus in the market. With increasing Lithium-based battery capacity globally, demand for associated battery materials is expected to rise. Among the other components of the Li-ion battery stack, PVDF plays an important role as a binder and separator coating, optimizing energy storage efficiency and reducing battery weight in EVs.

PVDF utilizes caustic soda and chlorine in its production at different stages. Primary feedstock includes vinylidene chloride or vinylidene fluoride, which are derivatives of caustic soda and chlorine.

Some significant developments in PVDF capacity are taking place in North America and Northeast Asia. Belgian chemical company Solvay entered into a joint venture with Mexico-based PVC producer Orbia to build the largest production facility of battery-grade suspension PVDF in North America with a capacity of 20,000 t/yr. Commercial production is expected to start in 2026 and the expected caustic soda and chlorine demand can be 8,000 t/yr and 12,000 t/yr respectively.

Solvay has doubled its capacity in Changshu, China in the past five years and raised its capacity in France by 35pc reaching 35,000 t/yr making it the largest production site in Europe. Another major producer French chemical company Arkema increased production capacity by 50pc last year at its Changshu site in China.

Japan-based producer Kureha is undergoing expansion at its Iwaki site in Japan, having a production capacity of 6,500 t/yr. The expansion is in two phases, first is a new capacity of 8,000 t/yr and another 2,000 t/yr in the second phase by debottlenecking resulting in a total capacity of 20,000 t/yr by 2026.

This article was created using data and insight from Argus Caustic Soda Analytics and Argus Battery Materials.

Spotlight content

Related news

Indian polyolefin importers wary on Middle East risks

Indian polyolefin importers wary on Middle East risks

Mumbai, 3 August (Argus) — Polyolefin buyers in India have slowed import purchases because the latest flare-up in the US-Iran war pushed prices higher and created uncertainty over delivery schedules. Prices of several polyethylene (PE) and polypropylene (PP) grades have risen in recent weeks on the back of higher Brent crude values, prompting caution among traders even towards booking China-origin material. Argus assessed linear low-density polyethylene (LLDPE) prices at $1,180-1,220/t cfr India for the week ended 31 July, compared with $1,090-1,150/t cfr India for the week ended 26 June. PP raffia prices were assessed at $1,190-1,240/t cfr India last week, compared with $1,100-1,140/t cfr India for the week ended 26 June. Many bought in a panic in April and will not repeat the same mistake now, said a Mumbai-based trader, referring to a surge of imports in the initial days of the war. India's PP imports rose rose by 39pc on the month to a record 201,732t in May on the back of a surge of China-origin arrivals because of tight domestic supply, Global Trade Tracker (GTT) data show. A subsequent price decline in June on the back of the interim peace deal also made importers cautious about committing to shipments given that prices could fall if freight shipping conditions change. Buyers would only pay a premium if the sellers can guarantee prompt shipments, the trader added. Higher freight charges are also stopping Middle East-based producers from cutting offers. Shipping companies signalled surcharges of up to $140/t for movement through the Bab el-Mandeb strait after attacks on Saudi energy vessels. The waterway is especially important for Saudi producers exporting polyolefins to key Asian demand hubs. But Saudi producer Sabic has not observed any disruption to container vessel traffic so far through the strait, it said last week. Buying could pick up in the coming days if domestic inventories are drawn down quickly, a Middle East producer said. Buying shifts to domestic producers Many traders are turning to domestic producers in the short term. The government's reintroduction of petrochemical import duties and the recent jump in import offers had encouraged some buyers to shift to Indian polyolefin suppliers, a key market participant said. Curbs on feedstock usage were mostly removed by New Delhi, prompting most Indian petrochemical producers to raise operating rates to offset the fall in imports. Major Indian producers have lifted LLDPE prices by 11,000 rupees/t ($115/t) and PP raffia prices by Rs12,500/t since 23 July because of higher crude prices and a slowdown in import bookings. If import bookings stay low, supply could tighten from end-August when converters seek material ahead of India's festive season, which typically begins in September. By Sourasis Bose Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil approves new rules for federal gas sales: Update

Brazil approves new rules for federal gas sales: Update

Adds large energy consumers association Abrace's comments. Sao Paulo, 30 July (Argus) — Brazil's national energy council CNPE approved a resolution on 30 July that will allow federally owned natural gas to be sold directly to the liberalized market through auctions, a move the government said could cut gas prices by more than 50pc and boost industrial competitiveness. The measure updates Brazil's policy for marketing state-owned gas and authorizes state-owned commodity trading firm PPSA to hold short-term auctions for 2026-30 and long-term auctions from 2030. The gas will be offered on an economic and competitive basis, with priority given to gas-intensive industries such as chemicals, petrochemicals, fertilizers and steelmaking, the government said. The mines and energy ministry estimates that state-owned gas prices could fall to about $5/mmBtu from around $12/mmBtu currently paid for gas commercialized by state-controlled Petrobras, according to minister Alexandre Silveira. The resolution is part of Brazil's gas-for-jobs program, which aims to increase domestic gas supply and improve competition in Brazil's gas market. The government said studies by state-owned energy research firm Epe indicate that the measure, together with ongoing regulatory actions by hydrocarbons regulator ANP, could generate R95bn ($17bn) in investments and add R79bn to Brazil's GDP. The government also expects the policy to lower gas costs for thermoelectric generation and compressed natural gas transportation. Large energy consumers association Abrace also backed the rules, saying they will create a more competitive environment and provide mechanisms to reduce gas prices for the industry. Abrace also highlighted other advancements made by ANP, such as the wider access to key gas infrastructures , which also help expand Brazil's open gas market. By Rebecca Gompertz Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil approves new rules for federal gas sales

Brazil approves new rules for federal gas sales

Sao Paulo, 30 July (Argus) — Brazil's national energy council CNPE approved a resolution on 30 July that will allow federally owned natural gas to be sold directly to the liberalized market through auctions, a move the government said could cut gas prices by more than 50pc and boost industrial competitiveness. The measure updates Brazil's policy for marketing state-owned gas and authorizes state-owned commodity trading firm PPSA to hold short-term auctions for 2026-30 and long-term auctions from 2030. The gas will be offered on an economic and competitive basis, with priority given to gas-intensive industries such as chemicals, petrochemicals, fertilizers and steelmaking, the government said. The mines and energy ministry estimates that state-owned gas prices could fall to about $5/mmBtu from around $12/mmBtu currently paid for gas commercialized by state-controlled Petrobras, according to minister Alexandre Silveira. The resolution is part of Brazil's gas-for-jobs program, which aims to increase domestic gas supply and improve competition in Brazil's gas market. The government said studies by state-owned energy research firm Epe indicate that the measure, together with ongoing regulatory actions by hydrocarbons regulator ANP, could generate R95bn ($17bn) in investments and add R79bn to Brazil's GDP. The government also expects the policy to lower gas costs for thermoelectric generation and compressed natural gas transportation. By Rebecca Gompertz Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US tariffs to cut Brazil's tallow exports

US tariffs to cut Brazil's tallow exports

Sao Paulo, 29 July (Argus) — New US tariffs are expected to curb Brazilian beef tallow exports to its largest overseas market, increasing domestic availability and potentially channeling more supply into biodiesel production. Brazilian beef tallow now faces a combined 37.5pc import tariff into the US, comprising a new 12.5pc duty imposed by the administration of President Donald Trump on 24 July and an existing 25pc tariff on Brazilian imports effective since 22 July. The feedstock has lost its competitive edge in the US Gulf coast market, which is a major demand center. Including beef tallow costs, freight costs for cargoes of up to 5,000 metric tonnes (t), the recently imposed tariffs and the value generated by the 45Z clean fuel production tax credit — which could be viewed as an additional cost since it only applies to US domestic feedstocks — imported Brazilian tallow carries an effective cost of around $1,936/t, according to Argus calculations. By comparison, US tallow at the US Gulf coast is available at roughly $1,700/t. Market participants expect only limited volumes of beef tallow to continue flowing to the US, primarily to producers that can take advantage of duty drawback provisions. These provisions allow some renewable diesel and sustainable aviation fuel (SAF) producers to recover duties paid on imported feedstocks when the finished fuel is subsequently exported to destinations such as Canada, Europe and other international markets. 1H export drop Brazilian tallow exports had fallen by approximately 40pc to 141,000t in the first half of 2026 from the same period in 2025, according to trade ministry Mdic data. This reflected the impact of previous US import tariffs, which created market uncertainty and disrupted trade flows to the product's primary export destination. Brazilian beef tallow prices are trending downward as export demand weakens following the closure of the US arbitrage. Further losses, however, are likely to be limited by production costs and slower cattle slaughter rates after Brazil filled its beef export quota to China, reducing tallow output. A drop in the price of the feedstock material will be insufficient to reopen the arbitrage opportunity to the US in the short term, according to traders. Falling beef tallow prices are likely to boost demand from biodiesel producers with the flexibility to process waste-based feedstocks. Tallow in Brazil's central-western Mato Grosso state is currently priced at R5,150 ($1,009)/t, a discount of R625/t to soybean oil, according to Argus indicators published on 24 July. But demand for the biofuel is not reacting as expected, given the backdrop of the conflict between the US and Iran, which has driven up fuel prices and altered economic dynamics worldwide. External demand With Brazil facing the highest tariff burden, US biofuel producers could increasingly turn to alternative sources of tallow, including Australia, New Zealand, and potentially Europe and other South American countries. More favorable tariff treatment for Asian suppliers could also support continued imports of used cooking oil (UCO) into the US, displacing some demand for tallow. But UCO arbitrage opportunities have narrowed in recent weeks, as the spread between origin markets and the US Gulf coast has become less attractive than it was in June. The US Environmental Protection Agency (EPA) finalized its record-high 2026 and 2027 biomass-based diesel blending mandates in March, covering renewable diesel, biodiesel, and SAF. The 2026 mandate represents a 60pc increase from the previous year, with targets set at 9.07bn renewable identification numbers (RINs) for 2026 and 9.20bn RINs for 2027. The announcement removed much of the uncertainty that had weighed on the industry throughout 2025 and provided a clearer demand outlook for biofuel feedstocks in the US. The higher mandates translated into stronger demand for feedstocks such as tallow on the US Gulf coast, where prices climbed to a record high of $1,995.81/t on 3 June. Elevated domestic prices opened arbitrage opportunities for imports during the first half of the year, supporting a recovery in overseas shipments. Although US tallow imports have yet to exceed their historical highs in 2026, they have rebounded significantly from lower levels early in the year. The recovery had boosted confidence among overseas suppliers, who expected import demand to continue strengthening through the remainder of 2026. But the new tariff measures have added fresh uncertainty to that outlook, raising questions about future trade flows and the competitiveness of different supplying regions. This has renewed attention on Europe as a potential destination for Brazilian tallow. European traders do not expect the US tariffs on Brazilian tallow to result in a significant increase in imports into the EU. Market participants had explored diverting Brazilian volumes to Europe when US tariffs reached 50pc in the second half of 2025, but shipments were limited, partly because veterinary approvals, certification requirements and border controls restricted market access. As a result, only small volumes arrived in early 2026 despite concerns over a potential influx. The latest 37.5pc tariff is therefore unlikely to change trade flows materially. Although Spain's RED III implementation is expected to support category 3 demand from 2027 by rewarding greenhouse gas emissions savings and leaving category 3 outside the 1.7pc Annex IX Part B cap, traders said freight costs, high energy prices and regulatory hurdles continue to prevent a viable Brazil-Europe arbitrage. Some market participants instead expect lower US imports from Brazil to support European exports to the US. Most European suppliers to the US do not expect an immediate impact from the latest tariff measures, noting it is too early to assess any shift in trade flows. Under EU animal-by-product rules, tallow is classified into categories 1, 2 and 3. Categories 1 and 2 are recognized as waste feedstocks under RED III Annex 9 Part B, while category 3, although not listed under Annex 9, remains an established biofuel feedstock. Typically, lower-grade category 3 tallow with 10-15pc free fatty acid (FFA) content is exported to the US, while higher-quality material with 5pc FFA or below is consumed within Europe. By Natalia Dalle Cort, Beatriz Pacheco, Anna Prokhorova and Jamuna Gautam Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.