Steam cracker capacity addition: relief in sight

Global steam cracker operating rates have been trending downward from 89pc in 2018 to 79pc in 2023, driven by the combination of high-capacity increase and slower economic growth in recent years.

In Argus's latest Ethylene Analytics, a recovery is forecast to take place in the coming years as the recent wave of new capacity cools off, absorbing demand growth before the second wave of capacity addition outgrows demand from 2027-2029. This recovery is based on a modelled assumption of modest growth in the global economy and a slowdown in capacity expansion. Historically, olefins demand growth has trended in line with GDP growth on a global basis; in recent years this relationship has disconnected. This was a result of the imbalance between the service and manufacturing industries, but we anticipate the trend will revert sooner or later moving forward.

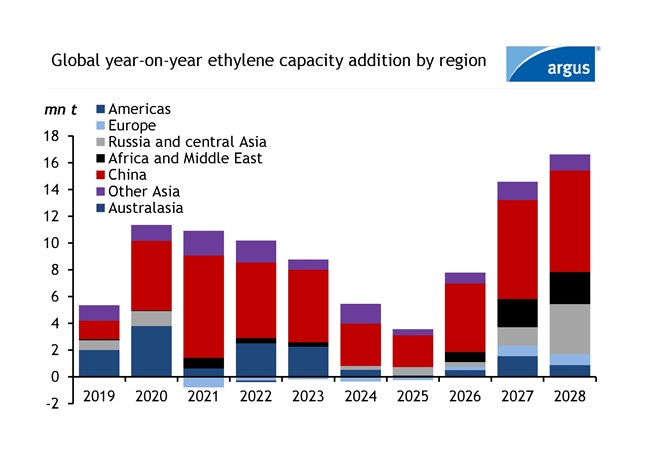

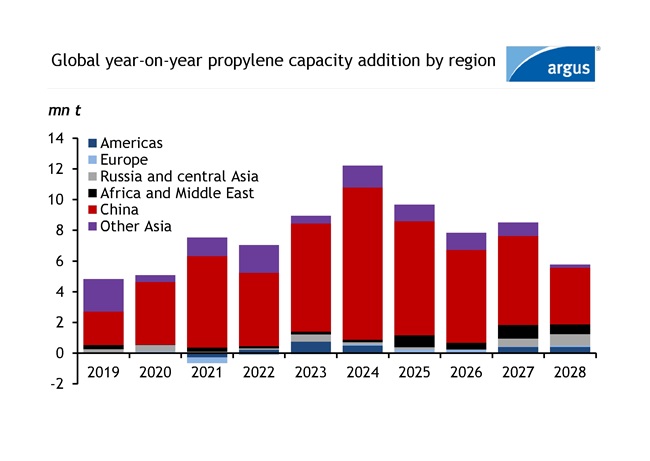

The petrochemical industry is experiencing high levels of upcoming capacity over the next five years. On a global level, ethylene and propylene capacity is expected to increase by 47.4mn t (4pc) and 44.0mn t (5pc), respectively, over the next five years while global capacity growth from 2018 to 2023 averaged at 4.5pc/yr for both ethylene and propylene. Most investment in ethylene production has gone into steam crackers where ethylene is the main product and propylene is produced as a co-product. Propylene will see a high-capacity increase from not only steam crackers but also from propane dehydrogenation (PDH) projects, which will delay the recovery of global propylene operating rates.

The first wave of ethylene capacity addition is cooling off, but a second wave is expected to kick off in 2026. However, propylene is currently undergoing its wave of capacity addition before seeing a slowdown from 2028 onward. On the propylene side of the olefins chain, 50pc of the upcoming capacity will come from PDH, 34pc from steam crackers and the rest will be a combination of sources from refinery, coal, and methanol.

Operating rates in all regions are being negatively impacted by the combination of high-capacity increase and slower global economic growth. Olefins demand has experienced slower growth over the past two years, with negative growth in 2022 as a result of high inflation and lower consumer spending.

Based on current market fundamentals there have been project delays across most regions and also rationalisation from uncompetitive units. With steam crackers running at lower-than-normal operating rates, rationalization of capacities is a significant unknown as what assets are to shut down are dependent on many factors such as company financials, politics, and integration factors. This makes the rationalization of specific units tough to predict.

As western nations are experiencing slower GDP growth, developing nations will be the key regions for olefins growth. We are seeing a slowdown in Chinese and northeast Asian GDP, but south Asian GDP has been holding strong. Polymer demand, which accounts for more than half of olefins consumption will be the main driver of olefins demand (65pc of ethylene gets consumed into PE and 71pc of propylene gets consumed into PP globally). From a supply perspective, 17pc (8mn t) of all upcoming cracker projects have yet to start construction, which will give operating rates a boost if delayed. Given the slowdown in global economic growth in the past two years, high interest rates, and inflation, the overall outlook is fairly bearish. Consumer spending, household disposable income, economic growth, project timelines, and rationalization from uncompetitive production facilities will be the main indicators of how quickly it will take for operating rates to recover.

Current announced projects

In the past five years, most steam cracker capacity increases took place in China and the trend is expected to persist over the next five years based on announced projects, but most regions are investing. Other Asian countries such as India, South Korea, Vietnam, and Indonesia are also investing. A total of 25.6mn t and 32.9mn t of ethylene and propylene capacity is expected to come online in China over the next five years. Below is the summary of upcoming stream cracker projects globally.

Chinese projects that are currently under construction include Wanhua Chemial, Yulongdao Refining & Petrochemical, Sinopec, Jilin Petrochemical and more. Joint venture steam cracker projects in China between domestic producers and multinational corporations have also started construction which includes Sabic-Fujian Petrochemical, Ineos Sinopec Tianjin, Shell CNOOC Petrochemical, BASF Zhanjiang, and ExxonMobil. These projects will increase ethylene capacity by 21.8mn t over the upcoming five years. Asian nations excluding China includes S-oil South Korea, Hindustan Petroleum India, Lotte Chemical Indonesia have also started construction which totals 5.2mn t of ethylene capacity.

Borouge, SATORP and a joint venture between CP Chem and Qatar Energy in the Middle East are also investing in new crackers with a total capacity addition of 5.2mn t. In Europe, Ineos Project One and PKN Orlen have announced projects while Sabic UK invested in a green project. The Sabic project involves restarting and converting its current cracker to run on hydrogen.

Russia has steam cracker projects slated to start up in the five-year span, including Nizhnekamskneftekhim, Irkutsk Oil, Baltic Chemical, and Amur GCC while Uzbekistan has also announced an expansion from Gas Chemical Complex. North America has three projects slated to come on over the next five years that will increase its capacity by 3.6mn t. North American projects include Shintech US, Joint venture CP Chem Qatar Energy, and Dow in Canada.

Argus’s Ethylene Analytics includes a global plant-level capacity dataset detailing expected project timelines.

Author: Dhanish Kalayarasu

Date: 15/05/2024