Steam cracker capacity addition: relief in sight

Global steam cracker operating rates have been trending downward from 89pc in 2018 to 79pc in 2023, driven by the combination of high-capacity increase and slower economic growth in recent years.

In Argus's latest Ethylene Analytics, a recovery is forecast to take place in the coming years as the recent wave of new capacity cools off, absorbing demand growth before the second wave of capacity addition outgrows demand from 2027-2029. This recovery is based on a modelled assumption of modest growth in the global economy and a slowdown in capacity expansion. Historically, olefins demand growth has trended in line with GDP growth on a global basis; in recent years this relationship has disconnected. This was a result of the imbalance between the service and manufacturing industries, but we anticipate the trend will revert sooner or later moving forward.

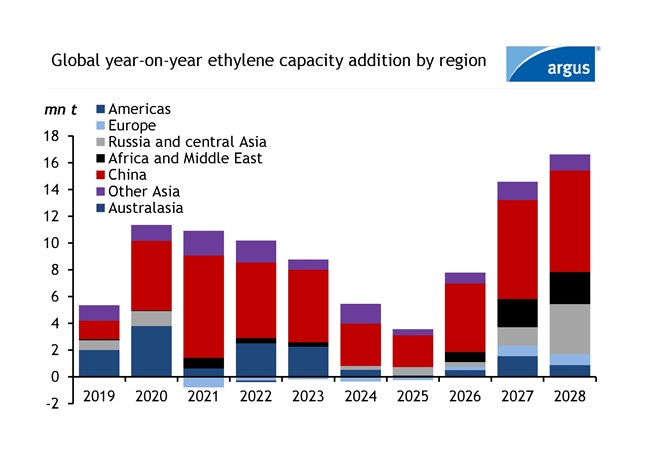

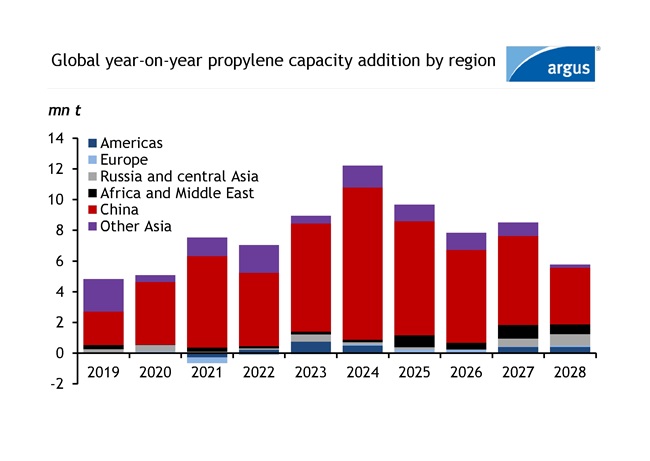

The petrochemical industry is experiencing high levels of upcoming capacity over the next five years. On a global level, ethylene and propylene capacity is expected to increase by 47.4mn t (4pc) and 44.0mn t (5pc), respectively, over the next five years while global capacity growth from 2018 to 2023 averaged at 4.5pc/yr for both ethylene and propylene. Most investment in ethylene production has gone into steam crackers where ethylene is the main product and propylene is produced as a co-product. Propylene will see a high-capacity increase from not only steam crackers but also from propane dehydrogenation (PDH) projects, which will delay the recovery of global propylene operating rates.

The first wave of ethylene capacity addition is cooling off, but a second wave is expected to kick off in 2026. However, propylene is currently undergoing its wave of capacity addition before seeing a slowdown from 2028 onward. On the propylene side of the olefins chain, 50pc of the upcoming capacity will come from PDH, 34pc from steam crackers and the rest will be a combination of sources from refinery, coal, and methanol.

Operating rates in all regions are being negatively impacted by the combination of high-capacity increase and slower global economic growth. Olefins demand has experienced slower growth over the past two years, with negative growth in 2022 as a result of high inflation and lower consumer spending.

Based on current market fundamentals there have been project delays across most regions and also rationalisation from uncompetitive units. With steam crackers running at lower-than-normal operating rates, rationalization of capacities is a significant unknown as what assets are to shut down are dependent on many factors such as company financials, politics, and integration factors. This makes the rationalization of specific units tough to predict.

As western nations are experiencing slower GDP growth, developing nations will be the key regions for olefins growth. We are seeing a slowdown in Chinese and northeast Asian GDP, but south Asian GDP has been holding strong. Polymer demand, which accounts for more than half of olefins consumption will be the main driver of olefins demand (65pc of ethylene gets consumed into PE and 71pc of propylene gets consumed into PP globally). From a supply perspective, 17pc (8mn t) of all upcoming cracker projects have yet to start construction, which will give operating rates a boost if delayed. Given the slowdown in global economic growth in the past two years, high interest rates, and inflation, the overall outlook is fairly bearish. Consumer spending, household disposable income, economic growth, project timelines, and rationalization from uncompetitive production facilities will be the main indicators of how quickly it will take for operating rates to recover.

Current announced projects

In the past five years, most steam cracker capacity increases took place in China and the trend is expected to persist over the next five years based on announced projects, but most regions are investing. Other Asian countries such as India, South Korea, Vietnam, and Indonesia are also investing. A total of 25.6mn t and 32.9mn t of ethylene and propylene capacity is expected to come online in China over the next five years. Below is the summary of upcoming stream cracker projects globally.

Chinese projects that are currently under construction include Wanhua Chemial, Yulongdao Refining & Petrochemical, Sinopec, Jilin Petrochemical and more. Joint venture steam cracker projects in China between domestic producers and multinational corporations have also started construction which includes Sabic-Fujian Petrochemical, Ineos Sinopec Tianjin, Shell CNOOC Petrochemical, BASF Zhanjiang, and ExxonMobil. These projects will increase ethylene capacity by 21.8mn t over the upcoming five years. Asian nations excluding China includes S-oil South Korea, Hindustan Petroleum India, Lotte Chemical Indonesia have also started construction which totals 5.2mn t of ethylene capacity.

Borouge, SATORP and a joint venture between CP Chem and Qatar Energy in the Middle East are also investing in new crackers with a total capacity addition of 5.2mn t. In Europe, Ineos Project One and PKN Orlen have announced projects while Sabic UK invested in a green project. The Sabic project involves restarting and converting its current cracker to run on hydrogen.

Russia has steam cracker projects slated to start up in the five-year span, including Nizhnekamskneftekhim, Irkutsk Oil, Baltic Chemical, and Amur GCC while Uzbekistan has also announced an expansion from Gas Chemical Complex. North America has three projects slated to come on over the next five years that will increase its capacity by 3.6mn t. North American projects include Shintech US, Joint venture CP Chem Qatar Energy, and Dow in Canada.

Argus’s Ethylene Analytics includes a global plant-level capacity dataset detailing expected project timelines.

Author: Dhanish Kalayarasu

Date: 15/05/2024

Spotlight content

Related news

Indian polyolefin importers wary on Middle East risks

Indian polyolefin importers wary on Middle East risks

Mumbai, 3 August (Argus) — Polyolefin buyers in India have slowed import purchases because the latest flare-up in the US-Iran war pushed prices higher and created uncertainty over delivery schedules. Prices of several polyethylene (PE) and polypropylene (PP) grades have risen in recent weeks on the back of higher Brent crude values, prompting caution among traders even towards booking China-origin material. Argus assessed linear low-density polyethylene (LLDPE) prices at $1,180-1,220/t cfr India for the week ended 31 July, compared with $1,090-1,150/t cfr India for the week ended 26 June. PP raffia prices were assessed at $1,190-1,240/t cfr India last week, compared with $1,100-1,140/t cfr India for the week ended 26 June. Many bought in a panic in April and will not repeat the same mistake now, said a Mumbai-based trader, referring to a surge of imports in the initial days of the war. India's PP imports rose rose by 39pc on the month to a record 201,732t in May on the back of a surge of China-origin arrivals because of tight domestic supply, Global Trade Tracker (GTT) data show. A subsequent price decline in June on the back of the interim peace deal also made importers cautious about committing to shipments given that prices could fall if freight shipping conditions change. Buyers would only pay a premium if the sellers can guarantee prompt shipments, the trader added. Higher freight charges are also stopping Middle East-based producers from cutting offers. Shipping companies signalled surcharges of up to $140/t for movement through the Bab el-Mandeb strait after attacks on Saudi energy vessels. The waterway is especially important for Saudi producers exporting polyolefins to key Asian demand hubs. But Saudi producer Sabic has not observed any disruption to container vessel traffic so far through the strait, it said last week. Buying could pick up in the coming days if domestic inventories are drawn down quickly, a Middle East producer said. Buying shifts to domestic producers Many traders are turning to domestic producers in the short term. The government's reintroduction of petrochemical import duties and the recent jump in import offers had encouraged some buyers to shift to Indian polyolefin suppliers, a key market participant said. Curbs on feedstock usage were mostly removed by New Delhi, prompting most Indian petrochemical producers to raise operating rates to offset the fall in imports. Major Indian producers have lifted LLDPE prices by 11,000 rupees/t ($115/t) and PP raffia prices by Rs12,500/t since 23 July because of higher crude prices and a slowdown in import bookings. If import bookings stay low, supply could tighten from end-August when converters seek material ahead of India's festive season, which typically begins in September. By Sourasis Bose Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil approves new rules for federal gas sales: Update

Brazil approves new rules for federal gas sales: Update

Adds large energy consumers association Abrace's comments. Sao Paulo, 30 July (Argus) — Brazil's national energy council CNPE approved a resolution on 30 July that will allow federally owned natural gas to be sold directly to the liberalized market through auctions, a move the government said could cut gas prices by more than 50pc and boost industrial competitiveness. The measure updates Brazil's policy for marketing state-owned gas and authorizes state-owned commodity trading firm PPSA to hold short-term auctions for 2026-30 and long-term auctions from 2030. The gas will be offered on an economic and competitive basis, with priority given to gas-intensive industries such as chemicals, petrochemicals, fertilizers and steelmaking, the government said. The mines and energy ministry estimates that state-owned gas prices could fall to about $5/mmBtu from around $12/mmBtu currently paid for gas commercialized by state-controlled Petrobras, according to minister Alexandre Silveira. The resolution is part of Brazil's gas-for-jobs program, which aims to increase domestic gas supply and improve competition in Brazil's gas market. The government said studies by state-owned energy research firm Epe indicate that the measure, together with ongoing regulatory actions by hydrocarbons regulator ANP, could generate R95bn ($17bn) in investments and add R79bn to Brazil's GDP. The government also expects the policy to lower gas costs for thermoelectric generation and compressed natural gas transportation. Large energy consumers association Abrace also backed the rules, saying they will create a more competitive environment and provide mechanisms to reduce gas prices for the industry. Abrace also highlighted other advancements made by ANP, such as the wider access to key gas infrastructures , which also help expand Brazil's open gas market. By Rebecca Gompertz Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil approves new rules for federal gas sales

Brazil approves new rules for federal gas sales

Sao Paulo, 30 July (Argus) — Brazil's national energy council CNPE approved a resolution on 30 July that will allow federally owned natural gas to be sold directly to the liberalized market through auctions, a move the government said could cut gas prices by more than 50pc and boost industrial competitiveness. The measure updates Brazil's policy for marketing state-owned gas and authorizes state-owned commodity trading firm PPSA to hold short-term auctions for 2026-30 and long-term auctions from 2030. The gas will be offered on an economic and competitive basis, with priority given to gas-intensive industries such as chemicals, petrochemicals, fertilizers and steelmaking, the government said. The mines and energy ministry estimates that state-owned gas prices could fall to about $5/mmBtu from around $12/mmBtu currently paid for gas commercialized by state-controlled Petrobras, according to minister Alexandre Silveira. The resolution is part of Brazil's gas-for-jobs program, which aims to increase domestic gas supply and improve competition in Brazil's gas market. The government said studies by state-owned energy research firm Epe indicate that the measure, together with ongoing regulatory actions by hydrocarbons regulator ANP, could generate R95bn ($17bn) in investments and add R79bn to Brazil's GDP. The government also expects the policy to lower gas costs for thermoelectric generation and compressed natural gas transportation. By Rebecca Gompertz Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US tariffs to cut Brazil's tallow exports

US tariffs to cut Brazil's tallow exports

Sao Paulo, 29 July (Argus) — New US tariffs are expected to curb Brazilian beef tallow exports to its largest overseas market, increasing domestic availability and potentially channeling more supply into biodiesel production. Brazilian beef tallow now faces a combined 37.5pc import tariff into the US, comprising a new 12.5pc duty imposed by the administration of President Donald Trump on 24 July and an existing 25pc tariff on Brazilian imports effective since 22 July. The feedstock has lost its competitive edge in the US Gulf coast market, which is a major demand center. Including beef tallow costs, freight costs for cargoes of up to 5,000 metric tonnes (t), the recently imposed tariffs and the value generated by the 45Z clean fuel production tax credit — which could be viewed as an additional cost since it only applies to US domestic feedstocks — imported Brazilian tallow carries an effective cost of around $1,936/t, according to Argus calculations. By comparison, US tallow at the US Gulf coast is available at roughly $1,700/t. Market participants expect only limited volumes of beef tallow to continue flowing to the US, primarily to producers that can take advantage of duty drawback provisions. These provisions allow some renewable diesel and sustainable aviation fuel (SAF) producers to recover duties paid on imported feedstocks when the finished fuel is subsequently exported to destinations such as Canada, Europe and other international markets. 1H export drop Brazilian tallow exports had fallen by approximately 40pc to 141,000t in the first half of 2026 from the same period in 2025, according to trade ministry Mdic data. This reflected the impact of previous US import tariffs, which created market uncertainty and disrupted trade flows to the product's primary export destination. Brazilian beef tallow prices are trending downward as export demand weakens following the closure of the US arbitrage. Further losses, however, are likely to be limited by production costs and slower cattle slaughter rates after Brazil filled its beef export quota to China, reducing tallow output. A drop in the price of the feedstock material will be insufficient to reopen the arbitrage opportunity to the US in the short term, according to traders. Falling beef tallow prices are likely to boost demand from biodiesel producers with the flexibility to process waste-based feedstocks. Tallow in Brazil's central-western Mato Grosso state is currently priced at R5,150 ($1,009)/t, a discount of R625/t to soybean oil, according to Argus indicators published on 24 July. But demand for the biofuel is not reacting as expected, given the backdrop of the conflict between the US and Iran, which has driven up fuel prices and altered economic dynamics worldwide. External demand With Brazil facing the highest tariff burden, US biofuel producers could increasingly turn to alternative sources of tallow, including Australia, New Zealand, and potentially Europe and other South American countries. More favorable tariff treatment for Asian suppliers could also support continued imports of used cooking oil (UCO) into the US, displacing some demand for tallow. But UCO arbitrage opportunities have narrowed in recent weeks, as the spread between origin markets and the US Gulf coast has become less attractive than it was in June. The US Environmental Protection Agency (EPA) finalized its record-high 2026 and 2027 biomass-based diesel blending mandates in March, covering renewable diesel, biodiesel, and SAF. The 2026 mandate represents a 60pc increase from the previous year, with targets set at 9.07bn renewable identification numbers (RINs) for 2026 and 9.20bn RINs for 2027. The announcement removed much of the uncertainty that had weighed on the industry throughout 2025 and provided a clearer demand outlook for biofuel feedstocks in the US. The higher mandates translated into stronger demand for feedstocks such as tallow on the US Gulf coast, where prices climbed to a record high of $1,995.81/t on 3 June. Elevated domestic prices opened arbitrage opportunities for imports during the first half of the year, supporting a recovery in overseas shipments. Although US tallow imports have yet to exceed their historical highs in 2026, they have rebounded significantly from lower levels early in the year. The recovery had boosted confidence among overseas suppliers, who expected import demand to continue strengthening through the remainder of 2026. But the new tariff measures have added fresh uncertainty to that outlook, raising questions about future trade flows and the competitiveness of different supplying regions. This has renewed attention on Europe as a potential destination for Brazilian tallow. European traders do not expect the US tariffs on Brazilian tallow to result in a significant increase in imports into the EU. Market participants had explored diverting Brazilian volumes to Europe when US tariffs reached 50pc in the second half of 2025, but shipments were limited, partly because veterinary approvals, certification requirements and border controls restricted market access. As a result, only small volumes arrived in early 2026 despite concerns over a potential influx. The latest 37.5pc tariff is therefore unlikely to change trade flows materially. Although Spain's RED III implementation is expected to support category 3 demand from 2027 by rewarding greenhouse gas emissions savings and leaving category 3 outside the 1.7pc Annex IX Part B cap, traders said freight costs, high energy prices and regulatory hurdles continue to prevent a viable Brazil-Europe arbitrage. Some market participants instead expect lower US imports from Brazil to support European exports to the US. Most European suppliers to the US do not expect an immediate impact from the latest tariff measures, noting it is too early to assess any shift in trade flows. Under EU animal-by-product rules, tallow is classified into categories 1, 2 and 3. Categories 1 and 2 are recognized as waste feedstocks under RED III Annex 9 Part B, while category 3, although not listed under Annex 9, remains an established biofuel feedstock. Typically, lower-grade category 3 tallow with 10-15pc free fatty acid (FFA) content is exported to the US, while higher-quality material with 5pc FFA or below is consumed within Europe. By Natalia Dalle Cort, Beatriz Pacheco, Anna Prokhorova and Jamuna Gautam Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.