Turkey Holds Firm in Soft Benzene Market

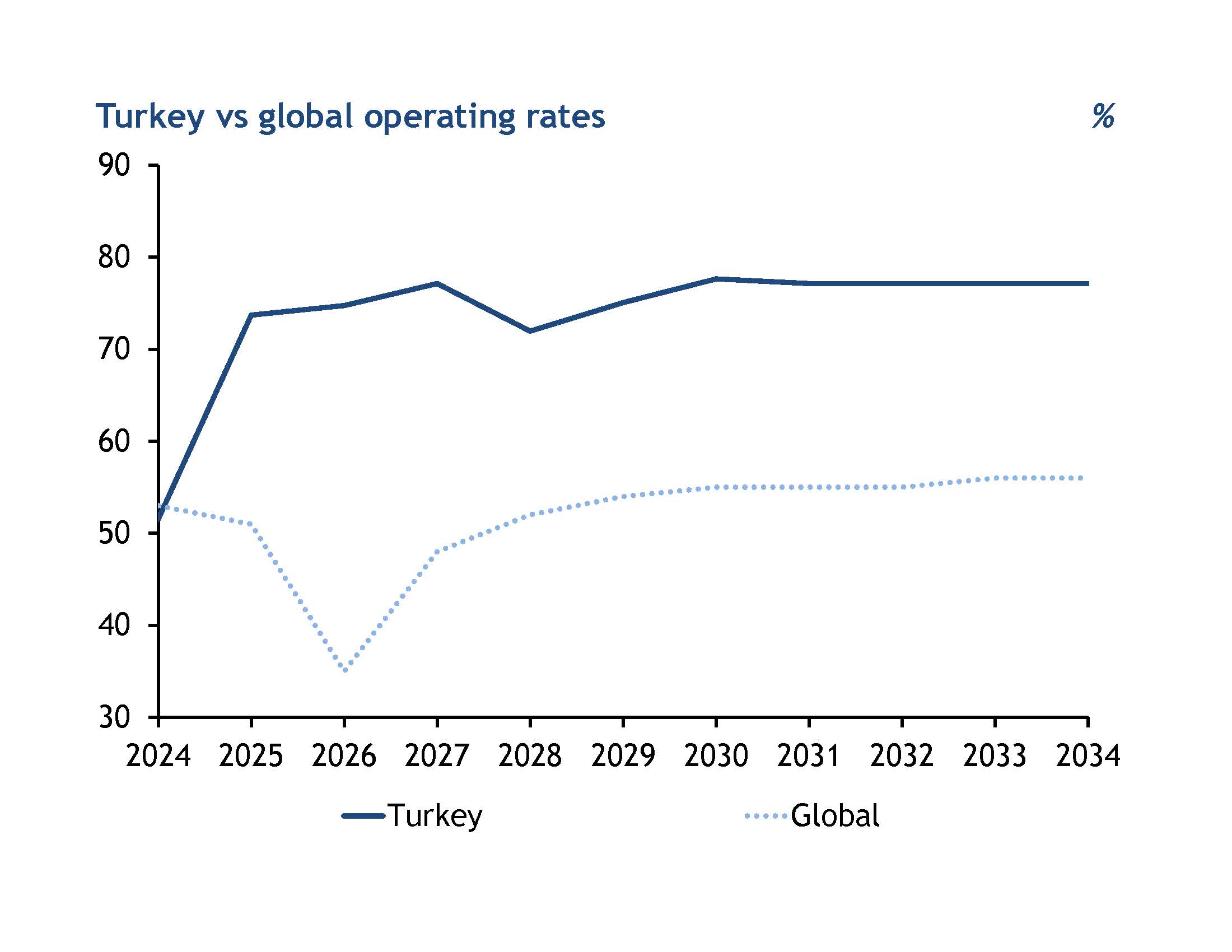

The global benzene market is going through a long period of weak performance. Operating rates are low, and profit margins are under pressure. This is due to weak demand and too much supply. Argus estimates that global operating rates will fall to about 55pc in 2026, followed by a slow recovery.

Against this weak global picture, Turkey stands out. The country is expected to maintain operating rates in the mid-70pc range, much higher than the global average.

This is notable because Turkey has a smaller aromatics industry than major producers in Asia. Its stronger performance is not driven by economies of scale but by favorable regional conditions.

– Argus analytics

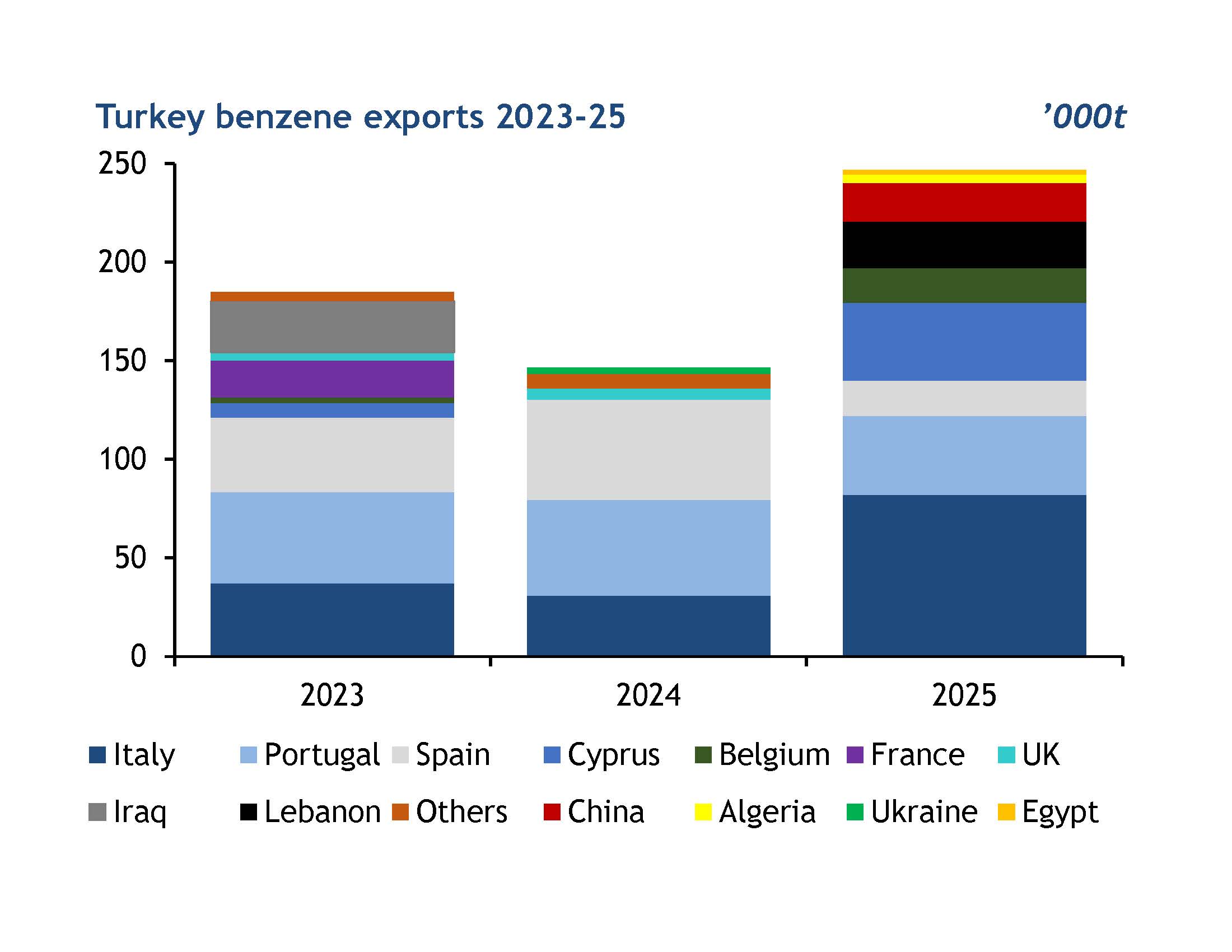

Turkey’s easy access to Europe gives the country an edge over suppliers from Asia. Cheaper and faster shipments help Turkish producers win more orders, especially when Europe faces supply shortages.

The country’s market conditions are also bolstered by feedstock from the STAR refinery. The Petkim complex, where most of Turkey’s benzene is produced, is connected to STAR by a direct pipeline, keeping naphtha and reformate supply stable. Because of this, Petkim can keep running at high rates even when the market is weak.

It is important to note that, from a geographic standpoint, the Mediterranean market has become increasingly insulated. Ongoing disruptions to key shipping routes, especially the Red Sea and the Suez Canal, have made it harder for cargoes to flow in from outside the region. This has reduced import flexibility and limited the usual balancing effect from global trade. As a result, regional supply is playing a much bigger role in shaping market conditions.

At the same time, supply within the region has tightened. The shutdown of Versalis olefin crackers has reduced the availability of aromatics co-products, including benzene. In addition, producers are focusing more on higher-value C6 derivatives such as ethylbenzene-styrene monomer (EBSM) and cumene. This shift is pulling feedstock away from the merchant benzene pool, which further tightens supply and widens the regional gap.

Geopolitical risks are adding to the pressure. Production of benzene, toluene, and xylenes (BTX) at Israel’s Haifa refinery has been disrupted by military action. This has lowered output and reduced exports into the Mediterranean market, creating more uncertainty and removing a key source of supply.

– Kpler data

While Turkey represents a small fraction of the global benzene market, it remains a bright spot in a tough environment.