Latest news

Military action will not reopen Hormuz: Analysts

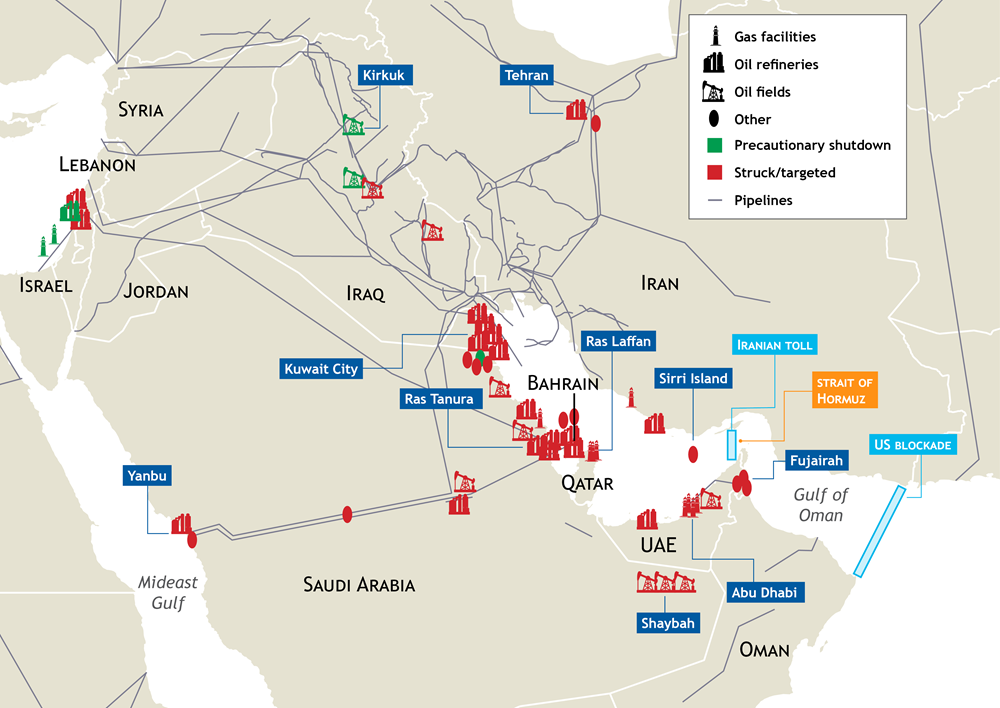

New York, 24 July (Argus) — Iran's ability to control commercial traffic through

the strait of Hormuz is unlikely to be deterred by US military operations given

the effectiveness of Iran's asymmetrical warfare tactics, according to analysts

following the war. The amount of firepower Iranians need to disrupt commercial

shipping is quite small, Center for Naval Analyses (CNA) research program

director Joshua Tallis told Argus, making it very difficult for the US to

degrade Iranian capabilities to a point where they pose no threat to commercial

shipping. "I do not believe, short of a massive ground invasion, that there is a

military solution to the Iranians' ability to disrupt and coerce commercial

traffic moving through the strait," Tallis said. "The only solution is

ultimately a diplomatic negotiated solution." CNA is an independent, nonprofit

research and analysis organization funded by the US government to advise its

military forces. Reducing Iran's motivation to attack, which can be done through

diplomatic means, may prove easier than reducing Iran's ability to attack,

shipping association BIMCO told Argus in March at the outset of the conflict

between the US and Iran. Iran has retained its ability to inflict severe damage

to commercial shipping through the strait of Hormuz using unconventional

tactics, despite intense US and Israeli strikes specifically aimed at degrading

Iran's ability to attack mariners and commercial vessels. Iran's asymmetric

capabilities to pressure vessel traffic in Hormuz include fast attack craft,

cruise missiles and drones. Maritime security firm Windward tracked 219 "speed

crafts" in the strait of Hormuz on 21 July, the largest single-day total since

15 May. Vessel traffic through the strait of Hormuz this week has increasingly

been concentrated in the northern traffic lanes overseen by Iran, suggesting

that its attacks on commercial shipping following other routes has been

successful. Windward data for 20-24 July shows that the northern lane carried

between around 88-100pc of all Hormuz traffic. All vessels that transited the

strait of Hormuz on 24 July did so on the northern Iranian controlled lane,

according to Windward. But commercial vessel traffic through the strait remains

at a fraction of prewar levels, with a combined 12 vessels transiting through

the waterway on 24 July, around 9pc of prewar levels, data from Windward shows.

By Charlotte Bawol Send comments and request more information at

feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights

reserved.