Spanish LNG imports fell to a multi-year low in June because of a heavy reliance on flexible spot cargoes, which were pulled away from Europe and towards Asia amid an open arbitrage, as well as slimmer demand on the year.

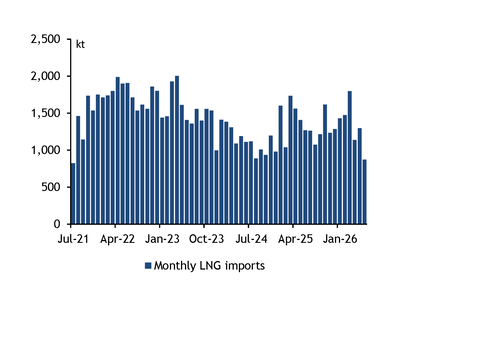

LNG deliveries to Spanish terminals totalled 873,000t last month following the arrival of the 174,000m³ LNG Port Harcourt II at Huelva on 29 June, Kpler data show. This is the lowest volume of unloadings for any June since 2016 when they totalled 861,000t and the lowest overall since 825,000t in July 2021 (see graph).

June unloadings last year were 1.27mn t, indicating a deficit of around 396,000t, or 31pc. This was much wider than the Europe-wide 19pc decrease in LNG imports on the year, dropping to 7.69mn t from 9.47mn t in June 2025.

The drop in LNG imports to Europe on the year hinged on a largely open inter-basin arbitrage during the month, which created a consistent financial incentive for sellers to divert uncommitted Atlantic basin cargoes to Asia from Europe. Periods when the arbitrage was closed were probably too brief to cause any significant diversions away from the Cape of Good Hope towards Europe.

The downturn in imports in Spain may have been especially pronounced because of its greater exposure to spot LNG and, in turn, arbitrage dynamics. Its extensive LNG regasification capacity often allows it to rely more on spot cargoes than other European countries, which tend to have less flexibility and a stronger dependence on long-term contracts. Spain imported 9mn t of spot Atlantic basin LNG in 2025, or 750,000 t/month, according to importers' association GIIGNL's annual report published in May. In Europe, this was second only to the Netherlands' spot imports from the Atlantic basin, which totalled 11.3mn t over 2025, or 942,000 t/month.

But the slowdown in imports was also probably partly demand-driven. Lower power-sector gas burn on the year to 286 GWh/d last month from 328 GWh/d a year earlier has been the principal factor driving down aggregate demand to 795 GWh/d from 851 GWh/d. The total year-on-year difference in demand was 1.7TWh, equivalent to just under two standard LNG cargoes.

Pressure on imports heightens in July

In July, tightening PVB-TTF prompt differentials suggest that Spanish firms have had to raise bids to keep their terminals attractive for cargo deliveries during the month, when demand typically rises.

Aggregate demand typically ticks up from June to July, with the five-year averages for June and July averaging 831 GWh/d and 866 GWh/d, respectively. This suggests that Spain will have to boost gas imports to meet demand relative to June, probably as LNG given that its limited pipeline import routes have been operating at or near maximum capacity in recent weeks.

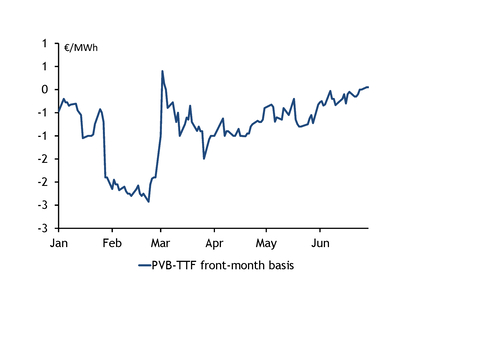

The PVB front-month contract strengthened relative to the TTF over June, which probably reflects continued uncertainty around transits via the strait of Hormuz and about LNG supply in the coming months. In turn, Spanish buyers have had to bid higher to continue to attract the limited number of spot LNG cargoes delivering to Europe. The PVB-TTF front-month basis market has tightened to average minus €0.165/MWh in June, the narrowest monthly average since the outbreak of the Middle East war and the effective closure of the strait of Hormuz (see graph). The differential averaged minus €0.69/MWh in March-May and minus €0.42/MWh in June 2025.

The PVB July contract even rose to a €0.05/MWh premium to the TTF on 29 and 30 June, probably prompting the diversion of the 141,000m³ Seapeak Galicia from Belgium's Zeebrugge facility to now be scheduled to arrive at the Cartagena terminal on 2 July, Kpler data show.