Argus Launches CCP Prices, Lists More Individual Redd+ Projects

In response to the continued evolution of the voluntary carbon market (VCM), Argus this month launched three enhancements to its suite of price assessments covering the global voluntary carbon market.

Firstly, to reflect the introduction of CCP-labelling for those credits that have been approved by The Integrity Council for the Voluntary Carbon Market (ICVCM) under their Core Carbon Principles, Argus is launching new assessments covering some key project types and geographies.

Secondly, the list of specific projects which are assessed individually has been extended with the addition of seven new projects.

And lastly, leveraging this broadening of the scope of individually-assessed projects, the calculation of the regional REDD+ prices has been changed to reference specific named projects.

In this article, Argus explains these changes in greater detail and why it is making them.

Summary

Argus has reported on the VCM since February 2023, producing weekly price assessments based on spot OTC trade for carbon credits such as REDD+ (Reducing Emission from Deforestation and Forest Degradation), Clean Cookstoves and Renewable Energy. In January 2024, assessments were added for ARR (Afforestation, Reforestation & Revegetation) for China, Colombia and Uruguay, IFM (Improved Forestry Management) for the US and China, and Blue Carbon for the Delta Blue Carbon project reflecting increased liquidity and interest in nature-based removals. The most recent enhancements are in response to two important developments in the market, namely changes in the market for REDD+ credits and also the emergence of the first CCP-labelled credits.

The Core Carbon Principles

A defining feature of the voluntary carbon market to date has been its private-sector and unregulated nature. In the absence of a defined and officially-recognised use case for carbon credits, pricing remains highly subjective and demand fickle. Apart from the lack of a true requirement for private corporations to buy carbon credits, purely voluntary action has also been inhibited by the lack of an adopted supply-side standard. Apart from the crediting programmes themselves, there has not been an independent body providing a standard definition of what qualifies as a bona fide carbon credit.

However, two such initiatives are beginning to emerge: the Integrity Council for the Voluntary Carbon Market (ICVCM) has introduced is Core Carbon Principles and the International Civil Aviation Organisation (ICAO) through its CORSIA programme are both seeking to bring standards to the supply side and it has been the CCPs which have been first to bring price definition to the market.

The core carbon principles have so far been applied to a selected number of methodologies covering landfill gas treatment (LFG), methane leak detection and repair and use and destruction of ozone depleting substances (ODS). This initiative is finally bringing to the market some highly-needed quality standardisation and sellers have already started marketing several credits, mostly based in Bangladesh, Brazil, China and the US. As such Argus will commence new assessments with prices to reflect four main variables: type of credit/methodology, location, carbon registry and vintages. Example: LFG US Verra 2020+. The minimum volume to be considered for our assessment will most likely be 5,000t. In terms of vintages, we will assess any credits of vintage 2020 onwards (2020+).

REDD+

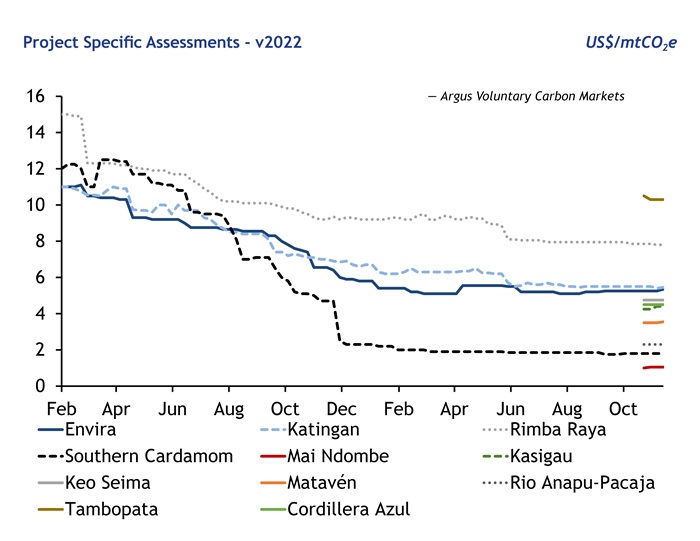

To date, we have had 15 prices covering REDD+ CCB in the first page of the report, five each for Latin America, Sub-Saharan Africa and Southeast Asia. We have assessed these prices based on bids, offers and trades for all the projects based in the three regions. These assessments were appropriate at the very first stages of the market but we have now started to see a clear trend where only two to five major projects in each region receive consistent market interest, on both the buy and sell side, with other projects valued either well above or well below, creating confusion as to what a reliable price average for a specific region should be.

The new system is designed to filter out outliers and create a more robust basket of projects from which to create averages for each region. We have selected the specific projects based on size, liquidity and quality with all of them carrying the CCB label which identifies projects with added benefits for the climate, community and biodiversity. As part of this we are adding prices for seven projects, one each in Southeast Asia, two in Africa and four in Latin America to have a final structure of two African projects (we are also discontinuing prices for Kariba), four in Southeast Asia and five Latin American projects (by far the most liquid market).

The rest of our assessments remain unchanged and we will continue to monitor developments in the CORSIA programme with a view to introducing related pricing at the appropriate time.

Learn more about the Argus Voluntary Markets service, get a free report and request a free trial.

Author: Adam Nye