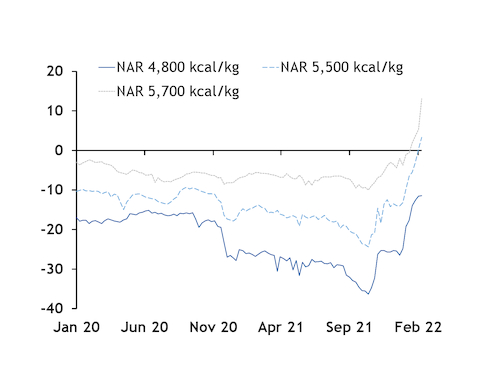

Two of the three off-specification South African coal grades assessed by Argus have moved to a premium to API 4 paper in recent weeks, prompted by tightening supply and firming demand for lower-calorific-value (CV) products.

Richards Bay NAR 5,500 kcal/kg coal — South Africa's most widely exported product — was assessed at a premium to API 4 on 4 February for the first time since Argus started assessing the off-specification differential in September 2019 .

The NAR 5,500 kcal/kg premium then widened from $0.40/t to $3.30/t on 11 February, reflecting firm demand for the product and no abatement in supply.

A similar trend has unfolded with the higher-grade NAR 5,700 kcal/kg differential, which first captured a premium to API 4 on 21 January. The premium has since risen for three successive weeks to be assessed $13.05/t above API 4.

The newly established off-specification grade premia are partly the result of a widening disconnect between the physical and paper markets in recent weeks, sparked by significant price volatility and acute supply tightness globally. There was, for instance, a 50,000t Richards Bay NAR 6,000 kcal/kg March-loading deal concluded on 15 February at $239/t, a premium of $53.30/t to the API 4 swaps assessment on the same day.

The trend has not been limited to South African coal. The midpoint of the best bid-offer in the NAR 6,000 kcal/kg cif ARA multi-optionality April market was $178/t on Tuesday, a premium of $23.05/t to the equivalent Argus April swap settlement on the same day.

But rising prices for off-specification grades have also been sparked in part by sharply reduced global supply prompting buyers to relax their specification requirements, according to market sources.

"The key question currently is: can you find any coal? People are not so fussed currently by [NAR 6,000 kcal/kg] coal and are willing to look at lower-CV grades," said a broker source. "The lack of Indonesian availability has also been a factor. Some buyers have come back to South Africa where they had moved away previously," he added.

A ban on Indonesian coal imports in issued in January has significantly tightened global coal supply, leading to a rally in prices. The ban has been lifted for some producers but continues to restrict the country's export availability.

South African exports fall

Rising prices for all grades of South African coal have been prompted by a sharp drop in exports from the country.

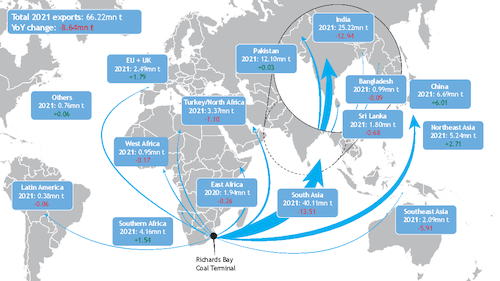

Total exports in 2022 slumped by 12pc on the year to 66.2mn t, customs data showed.

The fall was driven in part by a sharp decline in exports to Vietnam. Deliveries to the country reached just 1.15mn t in 2021, down from 7.5mn t in 2020.

Vietnamese buyers drastically increased imports in mid-2020 — when prices were crushed by coronavirus restriction measures in India and other major coal importers — resulting in a spike in receipts to 1.3mn t/month from South Africa during the spring.

But the significant fall in 2021 suggests exports to the southeast Asian country are returning to normality, with the 2021 figure close to the 2016-19 average, of 827,000t/year. Increased competition from Australian and other origin coal into the Vietnamese market in 2021 also trimmed South African market share.

Exports have also continued to be hit in recent weeks by logistics issues at the dry bulk terminal at Richards Bay.

Production and stocks decline

Falling exports have come in line with a sharp drop in South African production in recent months.

South Africa's coal production fell to its lowest since 2002 last year, as the rail transport disruption resulted in a build-up of stocks at mines and incentivised producers to scale-back output.

South Africa produced 229.7mn t of coal last year, down from 248.2mn t in 2020. Output in December fell by more than a fifth compared with a month earlier, to 15mn t from 19mn t in November. December production was the lowest for any month since at least 2015, when Argus began aggregating the monthly data.

Sharply falling production and exports have also been reflected in declining storage volumes at the Richards Bay Coal Terminal (RBCT).

Inventories at RBCT held just 2.39mn t on 10 February, down 28pc from the same time a year ago and 38pc on average inventories on this day between 2018-21.

Cable theft across South Africa's rail network has limited the amount of coal that can be transported for export. The amount of coal transported weekly by rail to the RBCT has averaged less than 1.1mn t in 2022 so far, well below historical norms of 1.5mn-1.7mn t.

Off-spec outlook

As to when off-specification Richards Bay NAR 5,500 kcal/kg and NAR 5,700 kcal/kg differentials will revert to discounts to API 4, sources said much will depend on the outcome of geopolitical issues — such as the Russia and Ukraine crisis — and the direction of natural gas prices in the months ahead.

Natural gas storage inventories continue to languish well beneath historic norms, with European inventories just 33pc full on 14 February, holding seven percentage points less in store than on the same day a year ago.

This is likely to contribute to continued global gas supply tightness, a factor which will likely support demand for all grades of South African coal in the months ahead.

Forward price valuations based on broker curves for NAR 5,700 kcal/kg are at a premium to API 4 until the fourth quarter of 2022, while NAR 5,500 kcal/kg is at a premium to the index until the third quarter of 2022.