Sulphur's sustained pre-crisis rally has left little impetus for a fresh spike in price in response to the outbreak of the war in the Middle East, unlike other commodities where prices have spiked.

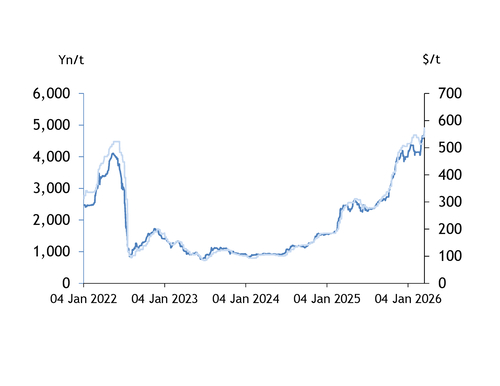

Sulphur prices had risen rapidly through 2024 and 2025, exceeding the heights of 2022, as a result of significant growth in demand from the metals sector alongside increased demand for fertilizer production. The Indonesian nickel industry in particular has seen exponential growth in sulphur demand for nickel refining, prompting a 440pc increase in the cfr Indonesia price, from $101/t cfr on 4 July 2024 to $554/t cfr by 29 January 2026, prior to the start of the conflict. Supply constraints in key production hubs in the latter part of 2025, such as the FSU and parts of the Middle East, added further tightness to the market.

Prices peaked in January but affordability challenges were already becoming evident, particularly from the non-metals sectors, prompting the start of a correction in global prices in the weeks leading up to the war. The market for sulphur had clearly decoupled from its traditional relationship with sulphuric acid and phosphate fertilizers due to the entry of the battery metal industry, and demand destruction was a factor.

By the time the war broke out on 28 February, fertilizer producers and chemical industries, having weathered months of tighter margins as sulphur prices reached unprecedented levels, were already questioning how long these higher costs could be sustained. And although the market was subject to a significant supply shock in the form of the closure of the strait of Hormuz and the subsequent suspension of production at QatarEnergy's Ruwais plant, prices did not immediately react. A sense of caution prevailed in the market over the first two weeks of the conflict with suppliers keen to avoid a surge in global prices for fear of further demand destruction. And with buyers absenting themselves from the market, there was no significant change to prices in the Middle East or related markets over this period. But the weekly fob Middle East price had already risen by $425/t or more than 600pc in the two years to January 2025 when it peaked at $531/t fob.

Many larger consumers have stocks in place and are typically quite resilient to supply chain disruptions lasting a few weeks. This is the result of most seaborne sulphur trade being shipped in solid form, with product able to remain in warehouses or even open air storage for some length of time. Buyers and sellers can therefore wait to see if sales concluded prior to the onset of the conflict can be delivered within a reasonable delay, and if buyers are in a position to wait for these shipments without the risk of double-booking. But as a co-product from oil and gas refining, supply cannot be readily increased in times of scarcity. Landlocked sulphur blocks in long-term storage remain in inland locations such as Alberta province in Canada and Turkmenistan, but this cannot easily be accessed as a result of sluggish processing and inland transportation bottlenecks.

In answer to the question around substitution, some consumers have looked at replacing sulphur imports with sulphuric acid imports, where the burning process is not required for energy generation. This has supported sulphuric acid prices, but not all buyers are able to switch from one product to another owing to logistical and other constraints.

In terms of sulphur itself, some product can be moved from the Saudi Arabian Red Sea ports of Jizan, Yanbu and Rabigh, as well as from Oman's Duqm port that all bypass the closed strait of Hormuz. But even if all vessel owners were prepared to load at Red Sea ports, which they are not, this would still leave in excess of 45pc of global sulphur supply stranded in the Mideast Gulf as long as the strait remains closed.

Defying the trend

Although global prices have barely moved since the start of the war, there is one market where the price has spiked and which has become a bellwether for this market.

Chinese domestic sulphur prices have been increasing steadily over the course of the war to date, reaching record highs of 4,815-4,820 yuan/t ex-works by Wednesday, equating to a rise of more than 20pc in just over two weeks. This market, where small lots trade from river warehouses on a daily basis largely from port stocks of imported product, has always been reactive to global trends. Although not always in strict alignment with global prices, it can provide a good indicator for the health of the market. China relies heavily on the Middle East for its sulphur requirements primarily to feed the domestic phosphate fertilizer industry, taking about half of the 9.6mn t imported in 2025 from the region.

Is the market ultimately turning?

With no immediate end in sight to the conflict and with little in the way of substitution for buyers requiring prompt material, the market may finally be turning.

Some part-cargoes to smaller consumers for prompt delivery and those linked to the metals industry have emerged priced as high as $580-700s/t cfr to the African market for late March-early April loading, with offers no lower than this range for the limited spot tonnes available. But larger fertilizer producers are resisting the latest run-up of prices and are likely to reduce operating rates alongside many smaller fertilizer producers that have already done so, leading to demand destruction on a larger scale. This may create a two-tier market with sales in a wider range to different industries, and will ultimately lead to a price cap on the basis of a lack of operating margin, making fertilizer production uneconomical, and to the potential erosion of prices. This may come prior to the strait fully opening to usual export flows if demand destruction becomes widespread. We are also assuming some sulphur vessels may be able to exit through the strait, with several Chinese-flagged vessels loaded for export assuming a deal can be struck with Iran. Some consumers are reportedly willing to look at booking Middle East volumes despite the lack of clarity on delivery schedules. These factors may smooth out the curve of a spike and crash from the logistical bottlenecks, with the 2022 crash still fresh in the minds of many in the market as profoundly disruptive.

18032026065633.jpg)