Butane has been heavily affected due to the evenly split nature of Mideast Gulf cargoes versus the US' propane-weighted supply, writes Waldemar Jaszczyk

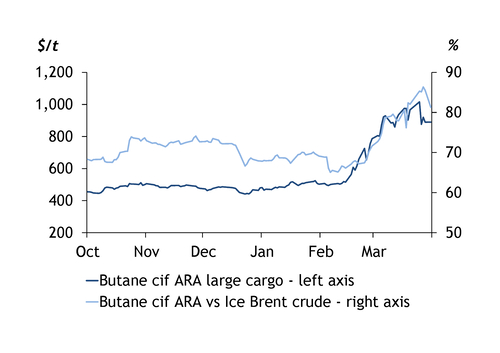

The price of butane imports to northwest Europe hit a four-year high against crude this month, outpacing gains in competing petrochemical feedstocks as the loss of Mideast Gulf exports from the Iran war disproportionately tightened global supply.

The large cargo butane price, basis cif Amsterdam-Rotterdam-Antwerp (ARA), rose by 20 percentage points from the start of the war on 28 February to 86pc of Ice Brent futures by 10 April — the highest since January 2022. Propane by contrast fell to a pre-conflict level of 63pc of crude having climbed to 71pc on 19 March. Firmer support flipped butane to a premium to propane of $131.25/t on 10 April from a $98/t discount a month earlier. The outright butane price stood at $889.25/t on 10 April, down from a peak of $1,016/t on 7 April but up from $515.50/t before the war.

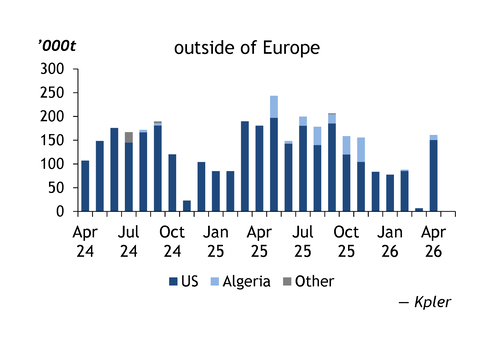

Reduced Middle East butane exports have increasingly pushed Asian buyers to the US, tightening availability for European importers. US butane exports to northwest Europe fell 36pc on the year to 143,000t in March, a five-year low for the month, according to Kpler. The war has affected butane supply more than propane because of the evenly split nature of Mideast Gulf cargoes, while the US' are 75pc propane weighted. Asian butane demand is also more inelastic given its vital use as a cooking and heating fuel, whereas propane use is centred on the petrochemical sector, where operating rates have been drastically cut. High returns from Asia-Pacific's short residential markets drew nearly all available US cargoes east, lifting US butane exports by 39pc on the year to a 10-month high of 1.66mn t last month.

Supply tightness in Europe forced UK petrochemical firm Ineos to bid aggressively for April cargoes, lifting butane's ratio to front-month naphtha by 12 percentage points to parity for the first time since May 2022. This defied seasonal norms, with ratios falling by over six percentage points relative to naphtha in February-April on average over the past five years. Ineos operates an 80,000t butane storage facility in Antwerp, Belgium — one of Europe's two largest above-ground LPG tanks.

But Ineos' demand was partly driven by restocking after strong barge demand from gasoline blenders in March. With steam cracker margins under pressure since 2022, Antwerp storage has focused on local cash sales and capturing spreads between large and small butane cargoes during peak winter blending. At the same time, 400,000 b/d of regional refining shutdowns and high natural gas prices prompting internal product use left Antwerp as ARA's key supply source. Butane fob barge prices relative to large cargoes — the basis for Ineos imports — consequently flipped to a $83.75/t premium in March from a discount of $20/t in 2025. Barge prices then softened as blending demand eased, but prices relative to naphtha remain above the range that typically triggers petrochemical buyers to switch to butane.

Waive goodbye

European buyers could also face stiffer competition for US butane from the country's domestic buyers after the US Environmental Protection Agency waived Reid vapour pressure limits on 25 March for summer-grade gasoline, allowing more butane to be blended. US butane deliveries to northwest Europe usually peak in the summer months as falling blending demand frees product for export.

But strong butane prices may erode the seasonal gains in petrochemical feedstock use at crackers. Butane-to-ethylene margins usually rise sharply in the second quarter, outperforming naphtha and propane by €255.25/t ($301.20/t) and €75.50/t on average. But they fell to -€554.50/t in March, an all-time low, after operators locked in monthly ethylene contracts before the war.

The butane price gains have pushed them above natural gas equivalents, raising the prospect of higher North Sea supply. The large cargo price was at a $154.50/t premium to Dutch TTF gas on 10 April, up from a $102.50/t discount a month earlier.