Low water levels on the Rhine have recently weighed on northwest European hydrotreated vegetable oil (HVO) prices by curbing demand from German buyers, but market participants expect the weakness to be temporary as stronger mandate-driven consumption and tighter global supply fundamentals are likely to support prices later this year.

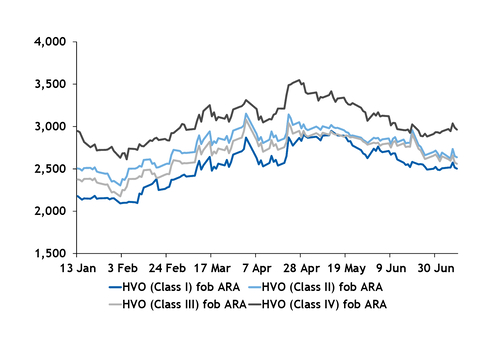

The Argus used cooking oil (UCO)-based HVO Class II and palm oil mill effluent (Pome)-based HVO Class IV outright prices have averaged around $2,765/t and $2,990/t during June and July so far, down from around $2,945/t and $3,290/t during April and May.

The decline has been driven largely by weaker demand from Germany, one of Europe's largest biofuel consumers. The water level at Kaub — a critical chokepoint on the Rhine — is forecast to fall to 50cm today, the lowest since August 2022. The resulting logistical disruptions have encouraged some German buyers to meet their greenhouse gas (GHG) reduction obligations through buying GHG quota compliance from other companies, rather than buying physical HVO. Companies generate the compliance by placing eligible renewable fuels that deliver greenhouse gas reductions compared with fossil fuels on the market.

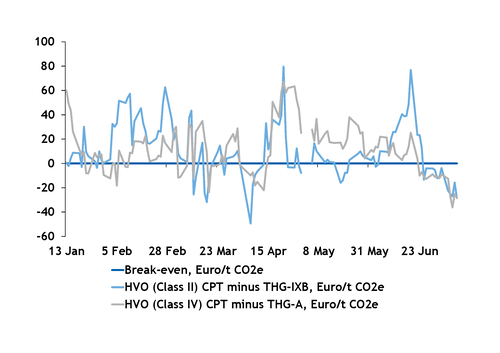

In Germany, when converted to the same unit as the GHG quota compliance certificates, HVO classes II and IV ended the week at €343.97/t CO2e and €451.90/t CO2e, according to Argus calculations (see chart). The 2026 Advanced and Other GHG quota were at €372.50/t CO2e and €480/t CO2e because of strong buying from obligated companies. Comparing in the same unit, called the cost per ticket (CPT), shows whether physical compliance or buying GHG quota is cheaper at any given time.

Renewed volatility in gasoil prices, brought on by the collapse of the fragile ceasefire that followed the signing of the US-Iran Memorandum of Understanding, has also weighed on HVO buying interest. Traders said the uncertainty has encouraged many market participants, particularly smaller buyers, to delay purchases and adopt a wait-and-see approach.

But market participants expect prices to strengthen once Rhine water levels rise, with HVO-specific drivers also pointing to a tighter supply-demand balance in the months ahead.

The case for HVO

RED III compliance targets are set at record levels across many European demand centres this year. In Germany alone, Argus Analytics estimates HVO demand at around 2.1mn t in 2026, up from around 800,000t in 2025, after Germany's RED III implementation entered into law in early June.

The new legislation abolished the practice of double counting for advanced feedstocks listed in part A of RED's Annex IX, which is expected to significantly boost HVO demand this year. Germany will require higher absolute volumes of renewable fuels to meet greenhouse gas (GHG) reduction quotas, supporting demand for drop-in fuels such as HVO.

Increased demand from the Netherlands could also lend support to the market, participants said. Dutch renewable fuel tickets have traded at a discount to physical HVO for most of 2026, partly because ticket generation has increased as a larger volume of renewable transport credits has been created from electric vehicles (EVs) and biomethane than in previous years.

In the Netherlands, on an equivalent basis as the tickets, HVO classes II and IV ended at 40.52c/kg CO2e and 51.69c/kg CO2e on 10 July, respectively, compared with 37.62c/kg CO2e and 48.50c/kg CO2e for the equivalent tickets, LRE-B and LRE-G.

On the HVO supply side, the finalisation of the new US renewable volume obligation in April has created a domestic requirement that is expected to outpace US HVO production. This has effectively eliminated the exportable surplus that previously flowed to Europe, which made the US one of the region's biggest HVO importers. The US had an exportable surplus into Europe of around 750,000t in 2025, according to Argus Analytics.

Europe will have to increasingly rely on HVO supply from Singapore, China, Malaysia and Canada, which could also flow in part to the US.

US output has also faced operational challenges. A reported explosion at PBF's facility in May, combined with hydrocracker maintenance at Phillips 66's Rodeo refinery has reduced available supply. A third US facility may undergo a turnaround this summer.

In Europe, expected maintenance at several production facilities this summer — including Ecoceres and Neste — is expected to constrain supply in the near term, lending further support to prices.

Expectations of firmer prices are reflected in the Class II forward curve. The HVO Class II Argus-settled Ice contract as a differential to gasoil has remained in contango since 6 July and peaks in October.

This structure is partly driven by the backwardation in the gasoil curve, reflecting expectations that tensions between the US and Iran will ease and HVO premiums to gasoil adjust higher as a result. But the outright HVO curve is also slightly in contango, with prices peaking in September. This suggests that HVO-specific fundamentals are likewise pointing to higher outright prices in the near term.