The calm in the chaos: a US steel sector seasoned by disruption

Key takeaways from the recent Argus Steel Forum and discussion around the US Steel industry's ability to cope with recent market upheaval.

Argus recently hosted its first US-based steel forum in Chicago, bringing together nearly 90 industry participants. What struck me most was how unphased the industry seemed, despite an environment filled with cacophonous background noise.

Volatile trade policy, global conflicts disrupting supply chains, pending labor negotiations, and upcoming US midterm elections all appeared to elicit little more than a shrug of the shoulders from parties in attendance. These variables are of course hugely impactful to the industry with real supply, demand and pricing ramifications, but for many participants, there was a sense of “been there, done that.”

Unlike many products and sectors now caught in newly launched Section 232 investigations or the Trump administration’s renewed tariff crosshairs, the steel and aluminum industries are grizzled veterans of trade wars following the rollout of tariffs under the first Trump administration in 2018.

While current supply in the US is tight, many in the audience were active in the market in 2021, when post-pandemic recovery created the tightest supply environment in history. As one participant noted, in 2021 it did not matter how large your company’s checkbook was—you could not buy your way to additional supply.

A war-related market disruption may feel like a black swan event, but to the steel industry it is simply another external shock, already experienced in 2022 with the onset of the Russia–Ukraine war. While higher fuel costs and surcharges are driving freight rates higher, the immediate impacts of the Iran conflict are more limited than those felt when the US temporarily lost access to more than 60% of its pig iron imports.

So, what are the key takeaways from the Argus forum? While the market continues to monitor external variables and their potential impacts, it is beginning to find some balance. The industry has now had four months in 2026 to adjust to the effects of last year’s trade policies, many of which were not fully felt until more recently.

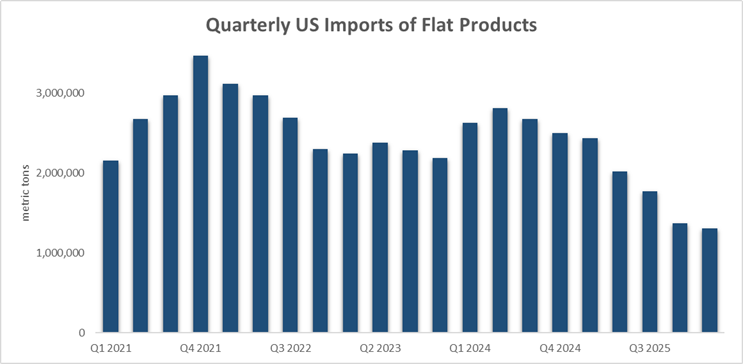

The expectation that US supply would become more readily available in the second quarter has been replaced by a more extended timeline, an outlook that makes sense when considering the sharp decline in flat-rolled imports.

In the first quarter of 2026, the US imported approximately 1.3 million metric tons of flat-rolled products, nearly half the 2.5 million metric ton quarterly average seen between 2021 and 2025.

Source: United States Department of Commerce, Enforcement and Compliance

| Year | First Quarter Imports |

|---|---|

| 2021 | 2,153,817 |

| 2022 | 3,118,011 |

| 2023 | 2,245,954 |

| 2024 | 2,627,997 |

| 2025 | 2,435,879 |

| 2026 | 1,303,401 |

Despite the success of the original Section 232 measures in 2018 incentivizing investment and modernization in US steelmaking, the country has not recorded a meaningful net increase in sheet steel capacity. Since 2020, the US has added an estimated 10.3 million metric tons of rated steelmaking capacity, while shuttering roughly 10.1 million metric tons over the same period, according to Argus estimates.

| Year | Company | Mill | Capacity (mt) |

|---|---|---|---|

| 2021 | US Steel | BRS 1 Phase 2 | +1,496,855 |

| 2023 | SDI | Sinton | +2,721,555 |

| 2025 | US Steel | BRS 2 | +2,721,555 |

| 2025 | Nucor | Gallatin | +1,270,059 |

| 2025 | North Star BlueScope | Delta | +852,754 |

| 2026 | US Steel | Granite City | +1,270,059 |

| 2020 | US Steel | Great Lakes | -2,177,244 |

| 2021 | US Steel | Granite City | -1,270,059 |

| 2022 | Cleveland-Cliffs | Indiana Harbor (#4) | -1,905,089 |

| 2023 | US Steel | Granite City | -1,270,059 |

| 2025 | Cleveland-Cliffs | Dearborn | -2,721,555 |

| 2025 | Cleveland-Cliffs | Riverdale | -725,748 |

| Total - Addition | +10,332,837 | ||

| Total - Reduction | -10,069,754 | ||

| Net | 263,083 | ||

Source: Argus

As a result, a marginal net capacity increase is now scrambling to offset a 1.2 million metric ton decline in supply in just the first quarter alone due to reduced imports. That gap is large enough to keep US supply constrained for the foreseeable future.

This situation is further compounded by spring maintenance outages and US Steel’s planned reline of its largest blast furnace, scheduled to begin later this month and last approximately 100 days.

Panelists also discussed the fading potential for imports to re-emerge later this year. At an industry event in February, buyers all recognized that, even with tariffs, offshore material could remain cost-competitive amid expectations of rising domestic prices. However, the war with Iran has injected volatility into freight markets and disrupted access to raw materials needed by exporting countries, limiting the likelihood that imports will play a significant role in balancing supply in the second and third quarters.

While the current supply situation in the market takes up much of the focus for conversations, demand, as the other side of the coin, is only whispered about. Those cautious whispers seem to be out of concern that if they say too loudly: “It’s actually pretty good,” the wheels will come off.

The steel demand for data center construction is at the top of the list of drivers but there has been strength in the energy markets, hope for a pickup in nonresidential construction after a brutal winter in the Northeast and Midwest, and the possibility of signs of life in the agricultural markets.

While the global headlines can fuel uncertainty, caution and doubt around the macroeconomic picture – there is a good portion of the steel industry that is still seeing healthy and steady demand. It just seems hard to feel that way.

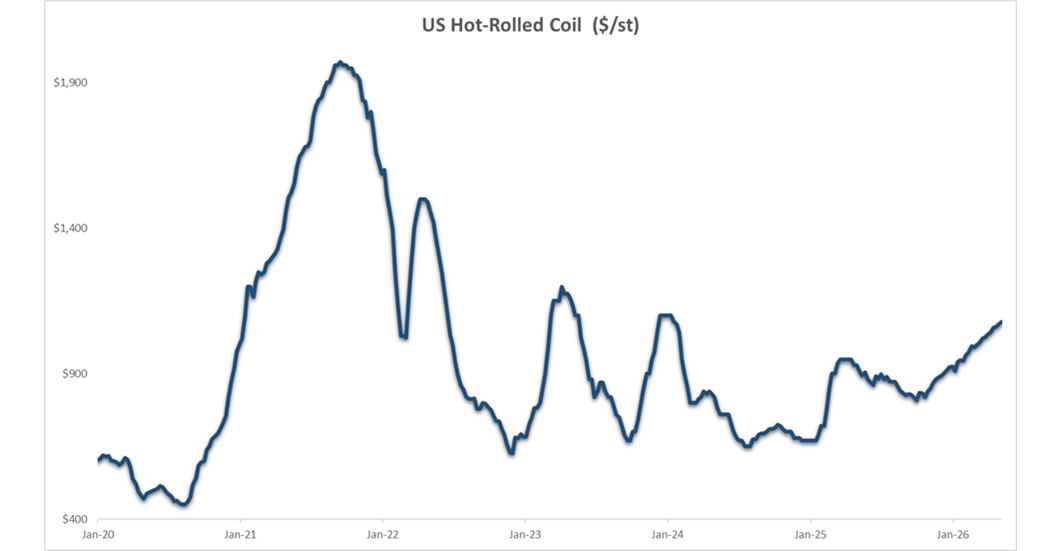

The nagging feeling the wheels will come off is hard to shake. The incremental increases in US sheet prices in 25 of the last 30 weeks have pushed prices close to their highest level in 2.5 years and, what goes up, must come down. But this price cycle has been different than any other over the last decade. The pace at which steel prices have increased is sluggish compared to other run ups where HRC eclipsed $1,000/st.

Source: Argus Global Steel

| HRC Price Cycle | % Change in Price | Days to Break $1,000/st from Low |

|---|---|---|

| 2020 | 122.22% | 147 |

| 2022–2023 | 59.30% | 98 |

| 2023 | 56.72% | 77 |

| 2025–2026 | 24.41% | 178 |

The result is a market that is neither overheating nor weakening, but steadily grinding higher, defying both the volatility of past cycles and the expectations of many participants. The nervousness has kept participants from being lulled into complacency but, with all this, there is a sense of familiarity in the steel market.

The steel industry is no stranger to disruption as trade policy, geopolitical shocks, and supply imbalances have become recurring features rather than exceptions. While everyone will keep a watchful eye on what lies ahead, for now conversations in Chicago seemed to point to an industry doing what it often does best: adapting, absorbing, and moving forward, one cycle at a time.

Author name: Michael Fitzgerald, VP of Business Development - Metals

Argus publishes US-specific steel price data and analysis weekly in the Argus Steel Index US - a supplement to the Argus Global Steel service. To receive a free trial of this report, please contact metals-m@argusmedia.com

Argus publishes US-specific steel price data and analysis weekly in the Argus Steel Index US