Weight of Freight: Size Matters – owners and charterers adjust to a changing tanker market

From 1967 until the oil crisis of 1973 there were orders for about 80 very large crude carriers (VLCC) and 40 ultra large crude carriers (ULCC), according to engine manufacturer Wartsila. This boom was followed by the total collapse of the newbuild market for these tankers until the middle of the 1980s. Since then, over 400 VLCC have been ordered, but it took more than 20 years before the next ULCC contract was signed.

The new TI class of ULCCs were delivered in the early 2000s, but within a decade most had been converted to floating production, storage and offloading (FPSO) vessels (FSOs) for use in the Mideast Gulf and southeast Asia. Prizing quantity over flexibility, these ships were wider than the new Panama Canal locks (begun in 2007 and completed in 2016), and could not travel through the Suez Canal unless on a ballast voyage.

Their massive capacity of more than 3mn barrels of crude oil reflected climbing global oil demand – almost double what it was in 1973 – and China’s arrival as the world's largest importer of crude oil. Some forecasters now predict oil demand will peak in 2030, reducing the need for supertankers, but other forces have seen shipowners and others return to newbuilding markets for VLCCs in recent months.

Pandemics, infrastructure projects, price wars and actual wars have moved and lengthened trade flows in the last four years, making larger vessels more attractive because of their economies of scale. These have impacted the make-up of the global tanker fleet in other ways as well, such as prompting a small recovery in interest in small Panamax tankers, which have long been sliding out of existence.

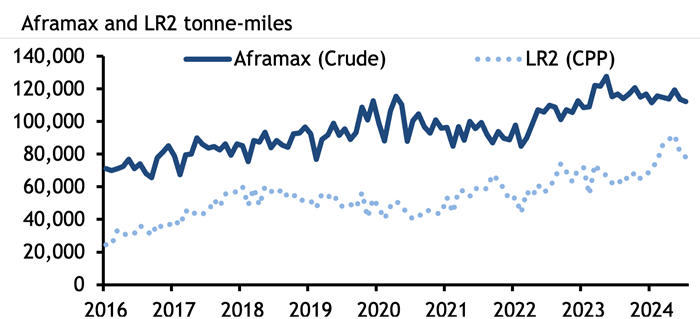

The role of vessel size in tanker freight markets is sometimes underappreciated. In the wake of the G7+ ban on imports of Russian crude and oil and products, and attacks on merchant shipping in the Red Sea and Gulf of Aden by Yemen’s Houthi militants, flows of crude oil have had to make massive diversions. Russian crude oil is flowing now to India and China rather than to Europe, while Europe’s imports of oil, diesel and jet fuel from the Mideast Gulf are taking two weeks longer, going around the Cape of Good Hope to avoid Houthi attacks. This has pushed up tonne-miles – a measure of shipping demand – to record levels. Global clean Long Range 2 (LR2) tanker tonne-miles rose to a record high in May this year, data from analytics firm Kpler show, while tonne-miles for dirty Aframax tankers rose to a record high in May last year. It has also supported freight rates.

High freight rates have brought smaller vessels into competition with larger tankers, at the same time as long routes have increased the appeal of larger ships. The Atlantic basin appears to be key site for increases in production (from the US, Brazil, Guyana and even Namibia), and an eastward shift in refining capacity globally will further entrench these long routes and demand for economies of scale.

Aframax and LR2 tankers are the same sized ships carrying around 80,000-120,000t of crude oil or products. LR2 tankers have coated tanks, which allows them to carry both dirty and clean cargoes, and shipowners may switch their

LR2/Aframax vessels between the clean and dirty markets, with expensive cleaning, depending on which offers them the best returns. But an unusually high number of VLCCs – at least six – have also switched from dirty to clean recently. Shipowner Okeanis, which now has three of its VLCCs transporting clean products, said it had cleaned up another one in the third quarter.

A VLCC switching from crude to products is very rare. Switching to clean products from crude is estimated to cost around $1mn for a VLCC. It takes several days to clean the vessel's tanks, during which time the tanker is not generating revenue. But a seasonal slide in VLCC rates in the northern hemisphere this summer has made cleaning an attractive option for shipowners, while their economies of scale make the larger tankers more attractive to clean charterers as product voyages lengthen.

Argus assessed the cost of shipping a 280,000t VLCC of crude from the Mideast Gulf to northwest Europe or the Mediterranean averaged $10.52/t in June, much lower than the average cost of $67.94/t for shipping a 90,000t LR2 clean oil cargo on the same route in the same period. It is likely these vessels will stay in the products market, as cleaning a ship is a costly undertaking for a single voyage.

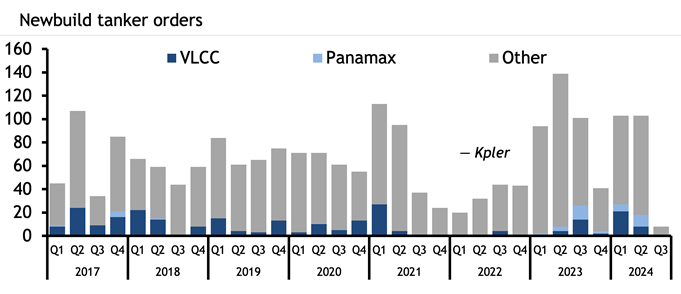

Typically, a VLCC will only carry a clean cargo when it is new and on its inaugural voyage, but just one new VLCC has joined the fleet this year, further incentivising traders to clean up vessels as demand for larger ones increases. This year has seen a jump in demand for new VLCCs, with 29 ordered so far. There were 20 ordered in 2023, just six in 2023 and 32 in the whole of 2021, Kpler data show. But the vast majority of these new VLCCs will not hit the water until 2026, 2027 or later because of a shortage of shipyard capacity.

Last year and 2024 also saw the first substantial newbuilding orders for Panamax tankers, also called LR1s, since 2017. Product tanker owner Hafnia and trader Mercuria recently partnered to launch a Panamax pool. The rationale may be that Panamax vessels can pass through the older locks at the Panama Canal, and so are not subject to the same draft restrictions imposed because of drought that has throttled transits and led to shipowners paying exorbitant auction fees to transit.

Aframaxes and MRs will remain the workhorses of crude and product tanker markets respectively, but the stretching and discombobulation of trade routes (which appear likely to stay) has already driven changes in which vessels are used and which are ordered. When these ships hit the water, they will join a tanker market very different to the one owners and charterers were operating in just four years ago.

Spotlight content

Related news

US extends but narrows Jones Act waiver

US extends but narrows Jones Act waiver

New York, 10 August (Argus) — President Donald Trump's administration said it will continue to waive domestic shipping requirements under the Jones Act for another 90 day, albeit with stronger oversight than the previous waiver. The waiver, first enacted 17 March, will now require the Department of Defense to consult with the US Maritime Administration (MARAD) on the availability of Jones Act vessels prior to an individual shipping voyage before determining whether the waiver can be applied, a White House official told Argus . This marks a shift from the waiver's current iteration, valid through 16 August, that relies on the vessel operator or charterer documenting their reasoning. As of 7 August, MARAD data show that around half of the reasons given for the 212 documented Jones Act waiver voyages simply cite the shipment's coverage under the waiver, while only 19 entries mention Jones Act vessels not being available. The new waiver still covers most products that were covered previously, such a diesel, gasoline, crude, soybean oil and fertilizers, but coal and coal-derived products are no longer allowed, according to the official. US-based shipping groups expressed strong opposition to a waiver extension, particularly under the existing blanket waiver authority used since March. "The government can respond to a genuine emergency without turning an exceptional waiver into a standing invitation for foreign operators to enter routine domestic commerce," former US federal maritime commissioner William Doyle said in an op-ed in the Washington Examiner on 10 August. The Trump administration issued the waiver of the Jones Act — which allowed foreign flagged and owned vessels to carry US-to-US shipments in place of US-flagged, US-owned and US-crewed vessels — on 17 March on national security grounds under section 501a and later extended it by 90 days. But some of the voyages conducted under the waiver have been criticized by the domestic maritime industry as not serving any national security purpose . The waiver was issued to ensure US airfields and military installations are properly supplied with fuel, but has otherwise been highly popular with US refiners. Republican lawmakers urged Trump in July to restore the Jones Act, calling the waiver "a loophole exploited by adversarial countries to erode America's maritime dominance". By Charlotte Bawol Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US tungsten scrap export curbs raise concern

US tungsten scrap export curbs raise concern

Houston, 10 August (Argus) — Tungsten market participants seek clarity on the reach and implementation of US export controls on tungsten waste and scrap, warning that limited domestic processing capacity could constrain the policy's near-term impact and cause oversupply. The US Bureau of Industry and Security (BIS), an agency within the Department of Commerce, announced last week that it will require domestic sellers of tungsten waste and scrap to allocate 100pc of their monthly sales to US buyers for a one-year period starting on 27 August. The order also restricts black mass exports. The upcoming restrictions on tungsten scrap exports are intended to keep more tungsten-bearing material in the US and encourage the development of additional processing capacity in the country. But market participants say limited domestic refining capacity will constrain the measure's near-term impact, as the US lacks sufficient capability to convert scrap into intermediate and finished tungsten products at scale. Many tungsten scrap dealers rely heavily on export markets, particularly in Asia. US exports of tungsten waste and scrap totaled 2,183 metric tonnes (t) from January-June 2026, nearly surpassing exports for the entirety of 2025 at 2,202t. Japan, Germany and South Korea were the largest recipients of US exports over that period. As a result, several tungsten carbide scrap exporters warned of near-term oversupply in the US market, as material that would otherwise be exported may have limited domestic outlets. "This is a death sentence for exporters," one trader told Argus . A second exporter said the new requirements will fundamentally "change the way we do carbide business", having to adjust strategy over the next year. Carbide scrap buying further slows ahead of controls Market participants broadly expect tungsten carbide scrap prices to come under further pressure in the near term as more material remains in the domestic market. For now, buyers and sellers have largely adopted a wait-and-see approach while they assess how the restrictions will be implemented. Only a few exporters reported spot purchases for small volumes under 10,000lbs last week to fulfill current orders before the controls take effect, while avoiding any additional orders. As a result, market participants broadly anticipate that tungsten carbide scrap prices will decline in the coming weeks. Argus last assessed US tungsten carbide inserts and rounds prices at $28-34/lb fob US processor on 31 July, their lowest levels of 2026. Prices decreased 13pc and 12pc, respectively, month over month as most large processors maintained adequate supply for the next few months while operating near maximum processing capacity, limiting purchasing requirements. Some exceptions expected The ruling effectively establishes export controls on tungsten waste and scrap, although companies may request adjustments or exceptions on a rolling basis. Multiple sellers expect export waivers to be granted primarily for material sent overseas for processing and refining with intentions to return tungsten units to the US. Several sources described the measure as more of a control mechanism than a complete export ban, with exemptions expected to be granted provided sufficient material remains available for US defense requirements. While defense demand for tungsten is expected to grow the sector accounts for only around 10pc of global consumption, according to 2025 estimates from Argus Tungsten Analytics , with automotive remaining the largest source of demand. The US Defense Logistics Agency recently sought information on the potential future acquisition of up to 200t of tungsten hard scrap, publishing a request for information (RFI) on 27 July. The RFI does not guarantee that the DLA will issue a tender; rather, it is intended solely for information-gathering and planning purposes. Market participants said waivers may be necessary until additional domestic processing capacity comes online. "With this measure, the US administration is working to foster the growth of processing capacity within the country. The interesting question will be whether funding from the Department of Defense or Department of Energy will be directed toward plant expansions or increasing capabilities within US industry, much as they have done in the rare earths, antimony and tin sectors," Joseph Miller, director at mining company Mission Critical Metals, said. Any new processing capacity could take years to develop, he added, and, for now, existing processors are expected to expand their capabilities rather than new entrants building significant new capacity. By Reagan Patrowicz and Cristina Belda Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Rhine oil traffic stops as water still dropping: Update

Rhine oil traffic stops as water still dropping: Update

Updates throughout Hamburg, 10 August (Argus) — Barge traffic along the River Rhine has largely come to a standstill, disrupting oil product supply in western Germany, barge operators said. Several terminals on the Lower Rhine will be cut off from barge traffic towards the end of the week. The gauge at the key Kaub bottleneck reached a new record low over the weekend, at 17cm. The federal waterways and shipping administration expects it to fall to as little as 4cm by 14 August, making Kaub practically impassable. Historically low levels have already slashed the number of barges able to pass Kaub, and the loads they can carry without running aground. A German shipowner said last week when levels had reached 23cm that a vessel with a maximum capacity of 1,200t can only carry 180t, and that the voyage to Karlsruhe from the Amsterdam-Rotterdam-Antwerp (ARA) hub now takes five days instead of two. Specialised vessels, which are wider and longer but draw less water, can carry a maximum of 700t. The federal waterways and shipping administration also said the water level in Cologne stood at just under 60cm today. Most inland vessel fleets require water levels of around 1m to reach the loading terminals at Cologne Molenkopf, Cologne-Niehl, Godorf and Wesseling, shipping companies said. This threshold was breached at the end of July, and water levels are forecast to fall further to as low as 40cm by mid-month. Loading terminals in western Germany, including Neuss, Duisburg and nearby Bendorf, may also become inaccessible during the week ending 14 August, shipowners said. German policymakers have introduced emergency measures to ease growing logistical constraints along the river. The federal states of North Rhine-Westphalia, Rhineland-Palatinate, Lower Saxony and Saarland have temporarily lifted restrictions on truck traffic on Sundays and public holidays. But it remains unclear whether the oil product sector will benefit from these steps. Replacing a fully loaded barge carrying 2,400t of diesel would require almost 89 road tankers, each with a capacity of 32m³. Fuel traders also report that their tanker fleets are already running above normal utilisation levels because of longer hauls to more competitively priced loading terminals. Product availability in western Germany, especially for road fuels, has tightened in recent weeks, traders said. Many traders that usually buy at tank farms along the Rhine are diverting to the Miro consortium's 310,000 b/d Karlsruhe refinery in southwestern Germany. But supply in southern Germany has also fallen after a leak at a mild hydrocracker at the Bayernoil consortium's 207,000 b/d Vohburg-Neustadt refinery prompted two local suppliers to pull supply from the spot market on 7 August. The restrictions are likely to last a week. By Natalie Müller and Johannes Guhlke Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US Senate starts recess without permitting deal

US Senate starts recess without permitting deal

Washington, 10 August (Argus) — The US Senate left town on Saturday for a five-week summer break without finishing its work on a bipartisan infrastructure permitting bill, complicating the path to enacting the legislation this year. Getting the bill done before the August recess was the "best chance" for it to become law, Senate Environment Committee chairman Shelley Moore Capito (R-West Virginia) said in June. But on 8 August, the Senate recessed after voting 90-6 for a funding bill that would avoid a shutdown in seven weeks. Senate negotiators have yet to release any text of the permitting bill, and they only have three weeks in session before the midterm elections on 3 November. Oil and renewable industry officials see an increasing likelihood that any votes on the permitting bill will not take place until after the midterms. If Democrats win control of either chamber, Republicans see slim chances to pass a permitting bill in the lame duck session or the next two years because of friction between Democrats and President Donald Trump. "It's going to be almost a dead issue from my perspective, in terms of thinking that the House is going to be able to do something constructive if the House flips," US senator Alan Armstrong (R-Oklahoma) said on 29 July. Congressional negotiators say they are not giving up on permitting, although they are floating the idea of narrowing the bill's scope to focus on issues with bipartisan agreement. Timing will not be an issue if the final bill has broad enough support among Republicans and Democrats, Senate Energy and Natural Resources Committee ranking member Martin Heinrich (D-New Mexico) said in a podcast interview POLITICO published on 3 August. He attributed delays with the bill to the Trump administration rather than his Republicans counterparts. "It has been the White House that consistently throws up new challenges, and that just makes it harder for us to sell any product to our caucuses," Heinrich said. Democrats have spent the last year warning the White House that taking further steps to undermine wind and solar development would make it more difficult for them to support a permitting bill, with little apparent success. The administration halted work on offshore wind projects that were under construction until they were blocked in court. The US Department of Defense was recently ordered by a federal judge to restart reviews of wind farms that had been frozen for a year. A recent proposal by the administration to weaken enforcement of the National Historic Preservation Act was "not helpful" to permitting legislation, Heinrich said. Republicans who are pushing for a permitting deal say it would be short-sighted of Democrats to scuttle a deal just because the administration has been blocking some projects. Armstrong, who was the executive chairman of pipeline company Williams before being appointed to the Senate, said a permitting bill would address the issue Democrats want to resolve. "Our industry's had its toes stepped on plenty of times," Armstrong said on 29 July. "I totally understand the emotions of that, but this is about legislating in a way that we don't have to tolerate that." The White House appears poised to unilaterally make changes to permitting policy even absent any legislation, although oil and renewable industry officials say those changes would not offer the certainty they need to invest billions of dollars in new infrastructure. As early as this month, the administration plans to finalize changes to make it harder for states to block "section 401" water permits for pipelines and to propose new rules for offshore wind permitting, according to a regulatory dashboard. By Chris Knight Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.