Weight of Freight: Size Matters – owners and charterers adjust to a changing tanker market

From 1967 until the oil crisis of 1973 there were orders for about 80 very large crude carriers (VLCC) and 40 ultra large crude carriers (ULCC), according to engine manufacturer Wartsila. This boom was followed by the total collapse of the newbuild market for these tankers until the middle of the 1980s. Since then, over 400 VLCC have been ordered, but it took more than 20 years before the next ULCC contract was signed.

The new TI class of ULCCs were delivered in the early 2000s, but within a decade most had been converted to floating production, storage and offloading (FPSO) vessels (FSOs) for use in the Mideast Gulf and southeast Asia. Prizing quantity over flexibility, these ships were wider than the new Panama Canal locks (begun in 2007 and completed in 2016), and could not travel through the Suez Canal unless on a ballast voyage.

Their massive capacity of more than 3mn barrels of crude oil reflected climbing global oil demand – almost double what it was in 1973 – and China’s arrival as the world's largest importer of crude oil. Some forecasters now predict oil demand will peak in 2030, reducing the need for supertankers, but other forces have seen shipowners and others return to newbuilding markets for VLCCs in recent months.

Pandemics, infrastructure projects, price wars and actual wars have moved and lengthened trade flows in the last four years, making larger vessels more attractive because of their economies of scale. These have impacted the make-up of the global tanker fleet in other ways as well, such as prompting a small recovery in interest in small Panamax tankers, which have long been sliding out of existence.

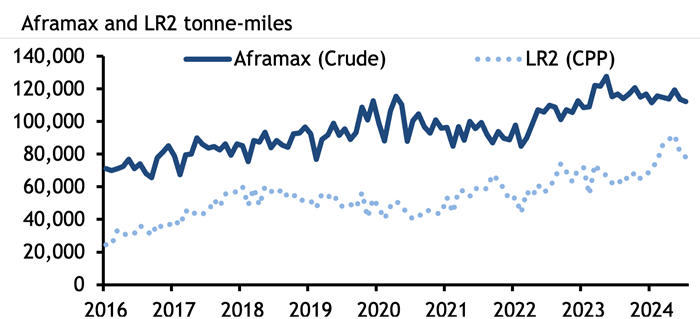

The role of vessel size in tanker freight markets is sometimes underappreciated. In the wake of the G7+ ban on imports of Russian crude and oil and products, and attacks on merchant shipping in the Red Sea and Gulf of Aden by Yemen’s Houthi militants, flows of crude oil have had to make massive diversions. Russian crude oil is flowing now to India and China rather than to Europe, while Europe’s imports of oil, diesel and jet fuel from the Mideast Gulf are taking two weeks longer, going around the Cape of Good Hope to avoid Houthi attacks. This has pushed up tonne-miles – a measure of shipping demand – to record levels. Global clean Long Range 2 (LR2) tanker tonne-miles rose to a record high in May this year, data from analytics firm Kpler show, while tonne-miles for dirty Aframax tankers rose to a record high in May last year. It has also supported freight rates.

High freight rates have brought smaller vessels into competition with larger tankers, at the same time as long routes have increased the appeal of larger ships. The Atlantic basin appears to be key site for increases in production (from the US, Brazil, Guyana and even Namibia), and an eastward shift in refining capacity globally will further entrench these long routes and demand for economies of scale.

Aframax and LR2 tankers are the same sized ships carrying around 80,000-120,000t of crude oil or products. LR2 tankers have coated tanks, which allows them to carry both dirty and clean cargoes, and shipowners may switch their

LR2/Aframax vessels between the clean and dirty markets, with expensive cleaning, depending on which offers them the best returns. But an unusually high number of VLCCs – at least six – have also switched from dirty to clean recently. Shipowner Okeanis, which now has three of its VLCCs transporting clean products, said it had cleaned up another one in the third quarter.

A VLCC switching from crude to products is very rare. Switching to clean products from crude is estimated to cost around $1mn for a VLCC. It takes several days to clean the vessel's tanks, during which time the tanker is not generating revenue. But a seasonal slide in VLCC rates in the northern hemisphere this summer has made cleaning an attractive option for shipowners, while their economies of scale make the larger tankers more attractive to clean charterers as product voyages lengthen.

Argus assessed the cost of shipping a 280,000t VLCC of crude from the Mideast Gulf to northwest Europe or the Mediterranean averaged $10.52/t in June, much lower than the average cost of $67.94/t for shipping a 90,000t LR2 clean oil cargo on the same route in the same period. It is likely these vessels will stay in the products market, as cleaning a ship is a costly undertaking for a single voyage.

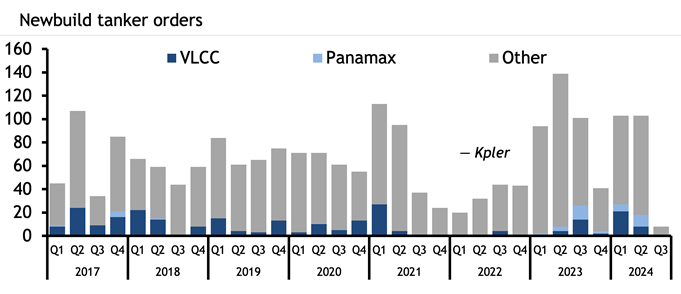

Typically, a VLCC will only carry a clean cargo when it is new and on its inaugural voyage, but just one new VLCC has joined the fleet this year, further incentivising traders to clean up vessels as demand for larger ones increases. This year has seen a jump in demand for new VLCCs, with 29 ordered so far. There were 20 ordered in 2023, just six in 2023 and 32 in the whole of 2021, Kpler data show. But the vast majority of these new VLCCs will not hit the water until 2026, 2027 or later because of a shortage of shipyard capacity.

Last year and 2024 also saw the first substantial newbuilding orders for Panamax tankers, also called LR1s, since 2017. Product tanker owner Hafnia and trader Mercuria recently partnered to launch a Panamax pool. The rationale may be that Panamax vessels can pass through the older locks at the Panama Canal, and so are not subject to the same draft restrictions imposed because of drought that has throttled transits and led to shipowners paying exorbitant auction fees to transit.

Aframaxes and MRs will remain the workhorses of crude and product tanker markets respectively, but the stretching and discombobulation of trade routes (which appear likely to stay) has already driven changes in which vessels are used and which are ordered. When these ships hit the water, they will join a tanker market very different to the one owners and charterers were operating in just four years ago.

Spotlight content

Related news

Economic loss from extreme weather fell in 1H: Swiss Re

Economic loss from extreme weather fell in 1H: Swiss Re

London, 11 August (Argus) — Global economic losses from extreme weather events in the first half of the year were 10pc lower than the 10-year average, but this "masks rising natural catastrophe risk", Swiss reinsurance firm Swiss Re said today. Economic losses globally from natural catastrophes, such as storms and wildfires, stood at $100bn in the first half, down by 34pc on the year, and 16pc lower than the 10-year average, Swiss Re data show. Global insured losses from natural catastrophes were $42bn, the lowest for the first half since 2020, the company said. Insured losses in January-June were less than half of those in the same period of 2025, which were driven by wildfires and severe storms in the US, including wildfires in California in January. But "a less costly first half of the year does not mean the risk has gone away", Swiss Re head of catastrophe perils Balz Grollimund said. "Europe's recent wildfires highlight how hotter and drier conditions are making large wildfires more likely and, with more homes, businesses and infrastructure built in risk-exposed areas, also more costly", he added. Wildfires had by 10 August burnt almost 543,000 hectares in the EU, nearly treble the long-term average, European Commission data show. The recent record heat in much of Europe "created an environment more conducive to wildfires", Swiss Re said. Although wildfires have only incurred a relatively small share of insured losses in Europe to date, it is the "fastest-growing weather peril globally", Swiss Re said. Its research estimates that insured losses from wildfires in Europe have increased by 8-11pc annually in real terms since 1970. Western Europe experienced its hottest July on record , data from EU earth-monitoring programme Copernicus show. The extreme heat and widespread drought has pressured the bloc's power systems and disrupted deliveries made by river . Europe is the fastest-warming continent, heating twice as quickly as the global average since the 1980s. "Strengthening resilience and reducing underlying risk will… be increasingly important in maintaining the affordability and availability of insurance", Swiss Re said. By Georgia Gratton Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Romanian 700MW unit to shut down this week

Romanian 700MW unit to shut down this week

London, 11 August (Argus) — The Romanian government has started technical preparations for the disconnection of the 700MW unit 2 at the 1.4GW Cernavoda nuclear plant later this week, the energy ministry said today. Given the very low Danube river flows and considering that the forecasts for Danube flows remain unfavourable, the controlled shutdown of the unit is expected this week, the ministry said. The latest forecasts indicate that Danube flows at Bazias will remain well below the 3,900 m³/s historical norm for August at least until the start of next week,remaining at 1,400 m³/s by 17 August, unchanged from this week. The ministry and transmission system operator (TSO) Transelectrica have started preparing for replacement output, including taking state-owned utility CE Oltenia's 300MW Rovinari lignite-fired plant out of reserve. And state-owned hydropower producer Hidroelectrica will use all of the available capacity at its plants, the ministry said. Romanian hydro stocks were at 2.01TWh, or 69pc of stored energy potential, in week 32 , 602GWh below the same period in 2025 and 447GWh below the five-year average for the week. The ministry has reiterated its call for responsible electricity consumption and voluntary reductions during the evening hours of 19:00-23:00. The last resort in the event that the system cannot meet demand is to cut power supply to certain large industrial consumers over those hours, it said. The announcement comes a few days after the government sank four metal barges in the Danube to redirect flows and increase levels near Cernavoda to ensure continued power production at the plant for "at least" the next nine days. Maximum temperatures in Bucharest are forecast to average 31.2°C, or 0.4°C above seasonal norms over the remainder of this week. By Apostolos Tsarikas Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Pupuk Indonesia closes initial DAP buy round

Pupuk Indonesia closes initial DAP buy round

Singapore, 11 August (Argus) — State-owned fertilizer group Pupuk Indonesia has closed the initial submission round for its DAP buy tender on 10 August, according to market participants. The company had issued a tender on 7 August to buy 90,000t of light or yellow granular 16-45 and/or 18-46 DAP for shipment in September-November on behalf of four of its subsidiaries. The date for the e-auction round for price submissions has not been announced. Offers must be submitted on a cfr basis, based on the 18-46 DAP. Offers for 16-45 DAP should be converted to the equivalent 18-46 DAP price. Pupuk Sriwidjaja Palembang (PSP) is seeking 30,000t of DAP for delivery to Boom Baru port, through six shipments of 5,000t each in September-December. Petrokimia Gresik (PKG) is seeking one lot of 20,000t DAP for delivery to Gresik port in October. Pupuk Kalimantan Timur (PKT) is seeking 20,000t of DAP for delivery to Bontang port through two 10,000t monthly shipments in October-November. Pupuk Kujang (PKC) is seeking 20,000t of DAP for delivery to Tanjung Priok and/or Cigading port through one 10,000t lot each in September and November. Pupuk Indonesia last awarded its tender seeking 45,000t of DAP on 16 July at $877/t cfr. By Hui Xuan Lek Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Iran gasoline supply hit as war cuts South Pars output

Iran gasoline supply hit as war cuts South Pars output

Dubai, 11 August (Argus) — Iran's gasoline output has come under pressure after recent US-Israeli attacks cut condensate output at South Pars by around 230,000 b/d, according to NIORDC. The giant offshore field, which Iran shares with Qatar, feeds roughly 60pc of the country's gasoline production, head of state-owned refining company NIORDC, Mohammad Sadegh Azimifar said on 10 August. Iran's refining, fuel storage and transportation infrastructure sustained around $1bn of damage in the attacks, Azimifar said. The attacks destroyed 52 of the 97 tanks at fuel depots in Tehran and Alborz provinces, wiping out around 1bn litres of storage capacity and knocking out some distribution facilities. The strikes have hit refining capacity directly. The Lavan refinery produced about 3mn l/d of gasoline before the war, but now operates at roughly half that following drone attacks in April, according to state-owned news agency Irna. Together with the South Pars condensate loss, the damage has pulled domestic gasoline output lower just as demand climbs. Iran's maximum supply capacity for gasoline and diesel is about 110mn l/d each, against daily gasoline demand of above 130mn l/d and diesel demand of 120mn l/d. The deficit widened during peak holiday periods, when consumption jumped to around 10pc above the annual average. Iran could require around five to seven MR-sized gasoline cargoes, equivalent to roughly 50,000-55,000 b/d in August, to cover the widening supply deficit , according to market participants. Meeting that requirement has become difficult as import routes come under strain. Much of Iran's fuel imports arrived via the southern route, but the blockade has now restricted those flows, Azimifar said. The domestic distribution network has been hit too, with pumping stations at Rey that move products from southern Iran towards Tehran and the north "completely destroyed", he said. Despite the damage, Iran is pressing ahead with delayed downstream projects, with the Mehr refinery and a gasoline quality upgrade at the Tehran refinery both due on line by the end of the year, Azimifar said. By Rithika Krishna Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.