Weight of Freight: Size Matters – owners and charterers adjust to a changing tanker market

From 1967 until the oil crisis of 1973 there were orders for about 80 very large crude carriers (VLCC) and 40 ultra large crude carriers (ULCC), according to engine manufacturer Wartsila. This boom was followed by the total collapse of the newbuild market for these tankers until the middle of the 1980s. Since then, over 400 VLCC have been ordered, but it took more than 20 years before the next ULCC contract was signed.

The new TI class of ULCCs were delivered in the early 2000s, but within a decade most had been converted to floating production, storage and offloading (FPSO) vessels (FSOs) for use in the Mideast Gulf and southeast Asia. Prizing quantity over flexibility, these ships were wider than the new Panama Canal locks (begun in 2007 and completed in 2016), and could not travel through the Suez Canal unless on a ballast voyage.

Their massive capacity of more than 3mn barrels of crude oil reflected climbing global oil demand – almost double what it was in 1973 – and China’s arrival as the world's largest importer of crude oil. Some forecasters now predict oil demand will peak in 2030, reducing the need for supertankers, but other forces have seen shipowners and others return to newbuilding markets for VLCCs in recent months.

Pandemics, infrastructure projects, price wars and actual wars have moved and lengthened trade flows in the last four years, making larger vessels more attractive because of their economies of scale. These have impacted the make-up of the global tanker fleet in other ways as well, such as prompting a small recovery in interest in small Panamax tankers, which have long been sliding out of existence.

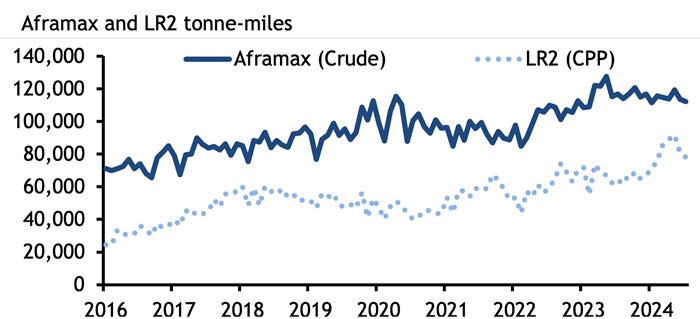

The role of vessel size in tanker freight markets is sometimes underappreciated. In the wake of the G7+ ban on imports of Russian crude and oil and products, and attacks on merchant shipping in the Red Sea and Gulf of Aden by Yemen’s Houthi militants, flows of crude oil have had to make massive diversions. Russian crude oil is flowing now to India and China rather than to Europe, while Europe’s imports of oil, diesel and jet fuel from the Mideast Gulf are taking two weeks longer, going around the Cape of Good Hope to avoid Houthi attacks. This has pushed up tonne-miles – a measure of shipping demand – to record levels. Global clean Long Range 2 (LR2) tanker tonne-miles rose to a record high in May this year, data from analytics firm Kpler show, while tonne-miles for dirty Aframax tankers rose to a record high in May last year. It has also supported freight rates.

High freight rates have brought smaller vessels into competition with larger tankers, at the same time as long routes have increased the appeal of larger ships. The Atlantic basin appears to be key site for increases in production (from the US, Brazil, Guyana and even Namibia), and an eastward shift in refining capacity globally will further entrench these long routes and demand for economies of scale.

Aframax and LR2 tankers are the same sized ships carrying around 80,000-120,000t of crude oil or products. LR2 tankers have coated tanks, which allows them to carry both dirty and clean cargoes, and shipowners may switch their

LR2/Aframax vessels between the clean and dirty markets, with expensive cleaning, depending on which offers them the best returns. But an unusually high number of VLCCs – at least six – have also switched from dirty to clean recently. Shipowner Okeanis, which now has three of its VLCCs transporting clean products, said it had cleaned up another one in the third quarter.

A VLCC switching from crude to products is very rare. Switching to clean products from crude is estimated to cost around $1mn for a VLCC. It takes several days to clean the vessel's tanks, during which time the tanker is not generating revenue. But a seasonal slide in VLCC rates in the northern hemisphere this summer has made cleaning an attractive option for shipowners, while their economies of scale make the larger tankers more attractive to clean charterers as product voyages lengthen.

Argus assessed the cost of shipping a 280,000t VLCC of crude from the Mideast Gulf to northwest Europe or the Mediterranean averaged $10.52/t in June, much lower than the average cost of $67.94/t for shipping a 90,000t LR2 clean oil cargo on the same route in the same period. It is likely these vessels will stay in the products market, as cleaning a ship is a costly undertaking for a single voyage.

Typically, a VLCC will only carry a clean cargo when it is new and on its inaugural voyage, but just one new VLCC has joined the fleet this year, further incentivising traders to clean up vessels as demand for larger ones increases. This year has seen a jump in demand for new VLCCs, with 29 ordered so far. There were 20 ordered in 2023, just six in 2023 and 32 in the whole of 2021, Kpler data show. But the vast majority of these new VLCCs will not hit the water until 2026, 2027 or later because of a shortage of shipyard capacity.

Last year and 2024 also saw the first substantial newbuilding orders for Panamax tankers, also called LR1s, since 2017. Product tanker owner Hafnia and trader Mercuria recently partnered to launch a Panamax pool. The rationale may be that Panamax vessels can pass through the older locks at the Panama Canal, and so are not subject to the same draft restrictions imposed because of drought that has throttled transits and led to shipowners paying exorbitant auction fees to transit.

Aframaxes and MRs will remain the workhorses of crude and product tanker markets respectively, but the stretching and discombobulation of trade routes (which appear likely to stay) has already driven changes in which vessels are used and which are ordered. When these ships hit the water, they will join a tanker market very different to the one owners and charterers were operating in just four years ago.

Spotlight content

Related news

Biofuel mandates give extra boost to US jet output

Biofuel mandates give extra boost to US jet output

Houston, 7 August (Argus) — The boom in US jet fuel output driven by disruptions from the US-Iran war is getting extra help by the economics associated with biofuel blending in road fuels. US refiners have been on a tear with jet fuel output this year, setting production records as the Mideast war curtailed flows and prices rose. Output has fallen since late June highs, to 2.068mn b/d in the week ended 31 July, according to the latest weekly data by the US Energy Information Administration (EIA), but remains 4.3pc higher than a year earlier. But refiners also have extra incentive to push more of their output toward jet fuel thanks to higher costs associated with meeting the US' Renewable Fuel Standard (RFS) for road fuels. In the four months since the Environmental Protection Agency finalized biofuel blend mandates for 2026 and 2027, prices for renewable identification numbers (RINs) created by blending and the Argus Renewable Volume Obligation (RVO) have reached all-time highs, signaling higher blending costs across the refining space. The RVO, which measures an obligated party's compliance costs for biofuel blending via RIN credit prices, peaked at 39.28¢/USG on 7 July after being valued near 22¢/USG in early March. Unlike diesel, petroleum-based jet fuel is not an obligated fuel bound by the RFS. As a result, refiners with the flexibility to adjust distillate yields may favor jet fuel production over diesel. Higher yields meet global demand Higher jet runs at US refineries have translated into greater export availability at a time when global supply remains disrupted through the strait of Hormuz, where 20-25pc of global jet fuel exports have historically transited. US jet fuel exports rose by 62pc year-on-year to an average of 308,000 b/d in July, according to Kpler tracking data, while EIA statistics indicate weekly volumes reached 445,000 b/d last week, or more than triple levels a year earlier. Yet, inventories remain 5.7pc above year earlier levels at 46.9mn bl. The Gulf coast is driving almost all of the increase in exports as regional production rose by 14.1pc annually to 1.185mn b/d last week, according to the EIA. Production on the US east coast, midcontinent and west coast remained below year-earlier levels. US Gulf exports comprised roughly 90pc of total national jet fuel exports in July, according to Kpler data. US jet cracks have strengthened since early June, peaking near $79/bl on 29 July before declining to roughly $67/bl by 4 August compared to just $23.66/bl at the same point last year. Refiners double-down on jet Refiners are poised to continue taking advantage of strong jet fuel margins in the near term, with multiple jet fuel capacity expansions either planned or recently completed. HF Sinclair completed a project allowing it to switch roughly 7,000 b/d of output between diesel and jet fuel at its 145,000 b/d Puget Sound refinery in Anacortes, Washington. Phillips 66 is planning a two-phase project at its 105,000 b/d Ferndale, Washington, refinery to increase jet fuel capacity by 12,000 b/d over 2026 and 2027. Marathon added 10,000 b/d of jet production capacity at its 253,000 b/d refinery in Robinson, Illinois, and brought 30,000 b/d of jet capacity online at its 617,000 b/d Garyville, Louisiana, refinery in March. The payoff for any jet output expansions may already be underway. In its second quarter earnings call in late July, independent refiner Valero said it expected third quarter margins for jet to widen because of an open arbitrage to Europe and as the US transitions to winter-grade diesel specifications. By Blake Del Papa, Matthew Cope and Anjali Shenoy Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

US sheds 23,000 jobs in July, revisions lower

US sheds 23,000 jobs in July, revisions lower

Houston, 7 August (Argus) — The US unexpectedly shed jobs in July and revisions halved gains in the prior two months, suggesting the labor market is weakening in the face of uncertainty spawned by rising energy costs linked to the Mideast Gulf war. The US unexpectedly lost 23,000 non-farm jobs in July, the Labor Department reported. That compared with a median average of about 80,000 job gains expected by economists surveyed by Trading Economics. Job gains in June were revised down to 20,000 from an initially reported 57,000, with May revised lower to 63,000 from an initially reported 129,000, for combined downward revisions of 103,000. "Looking ahead, we expect businesses to remain cautious about hiring in response to higher energy prices and uncertainty about how AI will affect staffing needs," Pantheon Macroeconomics said in a note. Total nonfarm employment averaged growth of 34,000/month for the 12 months prior to July. Average hourly earnings increased by 3.2pc in the 12 months to July, slowing from 3.4pc in June. The unemployment rate ticked lower to 4.1pc in July, the lowest since June last year, from 4.2pc the prior month. Retail trade lost 19,000 jobs in July, including 5,000 losses at gasoline stations and fuel dealers. Financial activities lost 14,000 jobs, and is down by 121,000 since a recent peak in May 2025. Health care added 22,000 jobs. Government jobs lost 53,000, partly reflecting lost teaching jobs as the school year ended. Following the report, odds of a quarter point Fed rate increase at the September meeting fell to 44pc in the CME's FedWatch tool from 55pc the prior day. The Fed has signaled it might hike rates to bring down inflation but signs of mounting labor market weakness could prompt it to hold longer. The report "is another nudge for the Fed to keep policy on hold for an extended period as inflation stemming from higher oil prices, tariffs and the AI buildout fades," Oxford Economics said in a note. Manufacturing added 5,000 jobs while construction added 22,000 jobs. Mining and logging shed 2,000 jobs. Transportation and warehousing added 9,700. Leisure and hospitality lost 40,000. The labor force participation rate, which tracks those employed and those actively seeking work, ticked lower to 61.4pc, the lowest since the Covid pandemic. The lower rate reflects rising retirements and discouraged workers. By Bob Willis Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Lithuania’s Lifosa phosphates plant suspends production

Lithuania’s Lifosa phosphates plant suspends production

London, 7 August (Argus) — Lifosa, Eurochem's phosphate plant in Lithuania, has now suspended production across all products, Argus understands. The suspension could not be directly confirmed with the producer. But it follows reports at the end of July that Lifosa was preparing to come off line because of high raw material costs. The plant has an annual capacity of 1mn t of DAP/MAP/NPS, 220,000t of MCP feed phosphate and 35,000t of tMAP. News of the suspension helped to encourage suppliers to raise DAP prices across Europe in the final week of July. But demand is poor and offers at €870/t fca in Germany and Benelux are so far failing to attract interest. Morocco's OCP this week reported selling 8,000t of DAP/MAP at the equivalent of the low to mid-€850s/t fca west European seaports at current exchange rates. By Tom Hampson Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Saudi Arabia, Turkey and Pakistan sign defence pact

Saudi Arabia, Turkey and Pakistan sign defence pact

London, 7 August (Argus) — Saudi Arabia, Turkey and Pakistan signed a joint defence pact in Mecca today. The agreement aims to "strengthen collective defence" and "stipulates that any armed attack against any one of the three states shall be regarded as an attack against them all", according to a joint statement. The deal follows a period of heightened instability in the Middle East centred around the US-Iran war. Saudi territory, including its oil and gas assets, has been repeatedly attacked by Iran and Iran-backed groups in Iraq and Yemen since the start of the war. It remains unclear what the defence pact commits the three states to in the event of any attack. Turkey was also targeted in the war's early stages. The agreement aligns three Sunni-majority Muslim countries closer together, with each bringing different strengths. Saudi Arabia is Opec's leading member and one of the world's largest oil producers, giving it significant financial power. Turkey has Nato's second largest army and has developed a strong defence industry in recent years, while Pakistan is the world's fifth most populous country and has nuclear weapons. Some analysts see the emerging alliance as a reaction to destabilising moves in the region by the US and Israel on the one hand and Iran and its proxies on the other. It follows an earlier defence pact signed between Saudi Arabia and Pakistan in September. By Aydin Calik Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.