Margins for US LNG offtakers have soared this week as trade disruptions from the US-Iran war send European and Asian LNG prices to multi-year highs while gains at the US benchmark Henry Hub are limited.

The war is unlikely to significantly boost Henry Hub prices despite increased demand for US LNG. Utilization rates at US LNG export terminals were already high before global prices surged, leaving little room for additional shipments.

US terminals shipped 10.75mn t in the 30 days that ended 2 March, Kpler data show, equivalent to a pace of 130.8mn t/yr. This equals a 94pc utilization rate of aggregated peak capacity. The only additional marginal volumes would come from the two projects undergoing commissioning in Texas: Cheniere's 11.45mn t/yr stage 3 expansion project at Corpus Christi LNG and the first train of QatarEnergy and ExxonMobil's 18.1mn t/yr Golden Pass LNG.

Global LNG prices have surged since the US and Israel attacked Iran on 28 February. The conflict has effectively halted traffic through the strait of Hormuz, cutting off supplies from Qatar's 77mn t/yr Ras Laffan and the UAE's 6mn t/yr Das Island export terminals that primarily go to Asian markets. US president Donald Trump announced on 3 March that the US will offer political risk insurance and naval convoys for ships traveling through the Mideast Gulf, but it is unclear how long it would take for volumes to return to the market. QatarEnergy halted production at Ras Laffan on 2 March and will need multiple days to resume operations.

This chokepoint has pushed Asian offtakers to seek replacement supplies, opening the arbitrage for cargoes from the Atlantic basin and creating a competition between European and Asian buyers for LNG. Prices for LNG delivered to northwest Europe in April jumped to $19.33/mn Btu on 3 March, more than double the $9.98/mn Btu on 27 February, Argus data show. LNG cargoes delivered to northeast Asia in May — a month later to account for a longer shipping distance from the Atlantic — increased to $16.87/mn Btu at the end of Singapore's trading day on 3 March, a 66pc gain from $10.14/mn Btu on 27 February.

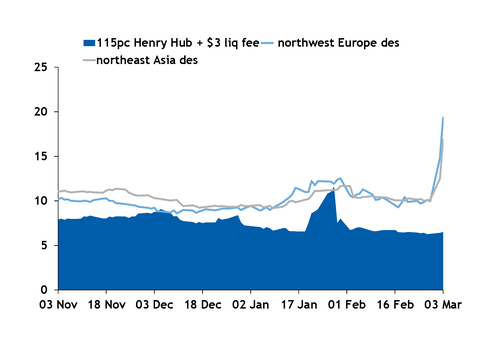

These price increases have far outpaced gains at the Henry Hub, the basis for LNG contracts in the US (see chart). Nymex gas for April delivery at the Henry Hub settled at $3.05/mn Btu on 3 March, just a 6.8pc increase from $2.86/mn Btu on 27 February. Prices have gained for three consecutive sessions since reaching a five-month low on 26 February but sat on the lower end of this winter's price range, which has stretched from $2.83/mn Btu to $7.46/mn Btu.

The muted gains have significantly raised the premium of delivered LNG markets above the indicative long-term LNG contract price, which comprises 115pc of Henry Hub plus a $3/mn Btu liquefaction fee. European LNG's premium over the indicative contract price grew to $12.82/mn Btu on 3 March, up from the February average of $3.59/mn Btu.