Firms in Germany must increase their rate of net injections into domestic gas storage sites by almost half to meet the 70pc national fill target by 1 November.

German storage sites held 69.35TWh of gas on Thursday morning, equivalent to a 28pc fill level, GIE transparency platform data show. Stocks exited the 2025-26 winter at a near-record low, creating a significant challenge for the summer stockbuild. But injections have lagged, despite the need as of Friday to add 104TWh to reach the 70pc threshold by 1 November.

Injections started relatively briskly in April, averaging 283 GWh/d — below 309 GWh/d a year earlier but above the three-year average of 193 GWh/d. Firms refilled sites by 10TWh last month and booked 6TWh of space for the 2026-27 storage year in parallel. The Middle East war was continuing but had not yet cut gas flows to Germany.

Slower Norwegian receipts and a slump in renewable generation — which boosted the call on gas-fired power plants — have curtailed injections in May relative to a year earlier and the three-year average. Net injections averaged 419 GWh/d on 1-14 May, well below 637 GWh/d a year earlier and the three-year average of 567 GWh/d. If injections hold in line with the rate so far this month, Germany will fall short of the 70pc fill target by 1 November. Net injections must rise by roughly 45pc to achieve the goal, requiring an average stockbuild of 612 GWh/d until 1 November. To do so, the country must avoid net withdrawals, such as those on 12-14 May at 77 GWh/d.

Norwegian deliveries should increase as maintenance winds down, but Europe faces stiff LNG competition from Asia, where cooling demand is emerging. The inter-basin arbitrage for uncommitted US LNG loadings has remained open throughout May, diverting some US LNG cargoes from Europe to Asia. LNG was a key source of German supply for replenishing stocks last summer, with LNG imports — along with Belgian and Dutch pipeline inflows, mostly based on LNG receipts — hitting all-time highs during April-October.

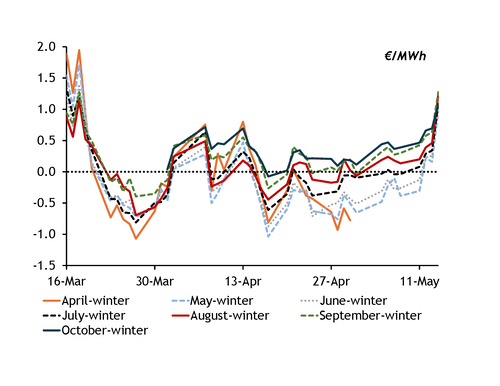

Summer-winter spreads invert again

The THE May price rose above the winter 2026-27 contract this week, further reducing incentives for firms to inject gas.

The THE May-winter 2026-27 seasonal spread normalised on 14 April, having fluctuated since 20 March (see graph). But the spread inverted again on 12 May, and on Thursday the spread widened to a €0.99/MWh premium for May from €0.16/MWh a day earlier. Monthly prices for delivery further out in the summer followed a similar pattern, but inverted earlier and offered even less incentive for summer injections. All remaining summer and October contracts closed above the winter price on Thursday.

About 71pc of German storage capacity is booked for the current storage year, Argus estimates, meaning Germany can technically reach its fill target without more bookings. Firms with booked capacity typically need narrower spreads to make injections economic. But the positive THE May-winter 2026-27 spread provides little incentive to stockbuild, even with existing bookings.

The seasonal spread inversion coincided with the start of net withdrawals. If firms favour withdrawing gas now — planning to re-inject later when spreads normalise — Germany could face severe difficulties in replenishing its stocks, especially if injections are delayed too long. But some injections may continue, as certain firms have hedged volumes and others have contractual obligations for winter delivery, requiring gas to be stored by specific dates.

The challenge extends to storage operators, which have struggled to sell space in recent auctions, allocating only 186GWh so far in May. No auctions for the current storage year took place this week, with the next scheduled for 3 June for 1TWh of space at VNG's Trading VSH product.

This year could prove more strained than last year, when seasonal spreads stabilised from 1 April and supported storage injections for the rest of the summer. The Middle East war is tightening the summer supply balance this year, which combined with persistently inverted spreads raises the prospect that Germany will miss its 70pc target by November. But the government still favours a non-intervention approach.