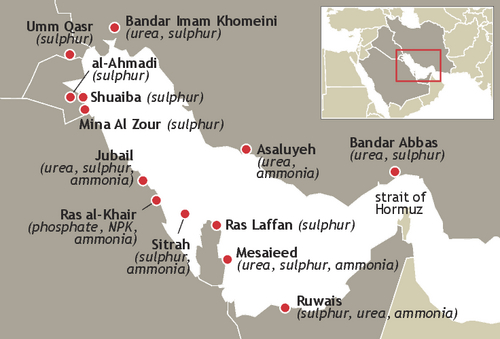

Iran's threat to "close" the strait of Hormuz in response to the US military attack on its nuclear sites over the weekend risks disrupting 20-50pc of international trade in urea, sulphur, phosphate and ammonia.

The risk is primarily to buyers of fertilizer and associated raw materials outside the Mideast Gulf as, with the exception of sulphuric acid, potash and some niche products, the flow of trade is dominated by exports.

Fully half of global seaborne sulphur trade originates from the Mideast Gulf — 20mn t this year, according to Argus Analytics — which goes primarily to China, Morocco and Tunisia, and for mining users in southern and central Africa. Sulphur is a key raw material for making phosphate fertilizers. Some substitution for sulphur by merchant sulphuric acid is possible but the sulphuric acid markets are already tight.

Urea markets also have a substantial degree of exposure to potential disruption to shipments from the Mideast Gulf, with around a third of seaborne trade supplied from the region. Exports from the Mideast Gulf are forecast at around 18mn t this year by Argus Analytics, from a global total of 56mn t. The major destinations for Middle East urea during the third quarter each year are typically Brazil, India, Thailand and Australia.

Ammonia exports from the Mideast Gulf account for around a fifth of global trade. Shipments this year from Mideast Gulf producers averaged around 365,000 t/month, according to Argus' tracking of loaded vessels, with the main buyers being fertilizer producers in India and Morocco, which have taken 830,000t and 315,000t, respectively, and mostly industrial buyers in South Korea, which have taken 335,000t.

For phosphates, the main risk is to the supply of MAP and DAP from Saudi Arabia. Saudi Arabia's Ma'aden produces around 20pc of the 17mn t/yr of seaborne trade in MAP and 14pc of the 12mn t/yr of DAP trade, with India typically the largest recipient of the latter, in terms of quantity, during the third quarter. All DAP and MAP shipments, plus some NPS, are loaded from Ras al-Khair.

On the import side, the greatest impact from any disruption to shipments in the region would be on sulphuric acid. Ma'aden is expected to import around 700,000t of sulphuric acid through Ras al-Khair in 2025, and line-up data show nearly 500,000t of acid will be shipped in the first seven months of the year, mainly from Asia-Pacific origins such as west coast India and China.

Few alternative loading mechanisms are available to bypass any disruption to the strait of Hormuz.

The UAE port of Fujairah in the Gulf of Oman can load bulk cargoes, but in the event of significant regional disruption the port might not be able to prioritise fertilizer exports over other commodities. It is also on the far side of the country from the urea and sulphur production facilities.

Saudi Arabia has several Red Sea ports, but distances overland from production sites close to the Mideast Gulf make this route operationally and commercially challenging.

The threat of disruption has so far not prevented trade in and stevedoring of cargoes within the region — including shipments from Iran's ports of Bandar Imam Khomeini and Asaluyeh — which continued over the weekend.

| Mideast Gulf fertilizer and related raw material exports | ||

| Product | Exports ('000 t/yr) | % of seaborne trade |

| Sulphur | 20,058 | 50 |

| Urea | 17,978 | 32 |

| Ammonia | 3,635 | 21 |

| MAP | 3,480 | 20 |

| includes exports from Bahrain, Iran, Iraq, Kuwait, Qatar, Saudi Arabia, UAE | ||

| — Argus Analytics | ||