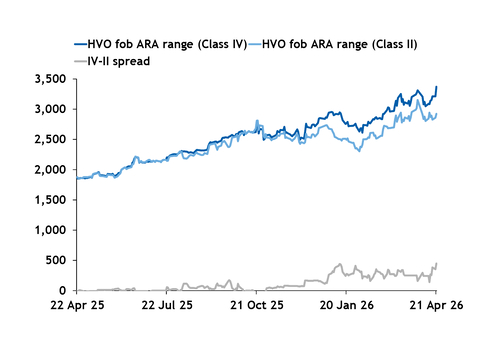

The northwest European HVO Class IV–II spread reached a record high of around $450/t on Tuesday, 21 April, up from $250/t a month prior, driven by scarce Class IV offers and growing expectations of compliance-driven demand.

Hydrotreated vegetable oil (HVO) Class II is produced from used cooking oil (UCO), while Class IV is made from palm oil mill effluent (Pome). Under the EU Renewable Energy Directive (RED), the contribution of Class II — along with other biofuels made from Annex IX B feedstocks — is capped in meeting the transport renewable energy target, whereas Class IV is incentivised alongside biofuels made from Annex IX A feedstocks.

Biofuels made from Annex IX feedstocks are double-counted toward mandate compliance in many member states.

In practical terms, the spread widened because the Class IV premium to gasoil traded higher by $95/m³ on Tuesday's Argus Open Markets (AOM), while Class II only traded higher by $20/m³.

Class IV firmed because of supply-side behaviour linked to regulatory expectations, with market participants attributing the move mainly to a scarcity of Class IV offers in the Amsterdam-Rotterdam-Antwerp (ARA) hub. Expectations that the Netherlands and Germany will abolish double-counting of Annex IX feedstocks from 2026 are likely to significantly boost HVO demand this year. As higher absolute amounts of biofuel would be required to meet greenhouse gas (GHG) reduction quotas, demand for drop-in fuels such as HVO is likely to rise.

Those expectations strengthened following legislative developments in Germany and the Netherlands on Tuesday. The countries are among Europe's largest biofuels consumers.

In Germany, implementation of the updated Renewable Energy Directive (RED III) has been added to the parliamentary agenda on Thursday, while in the Netherlands legislation amending the Environmental Management Act and the Excise Duty Act has been ratified.

Both countries — along with France, Italy and Spain — missed the 21 May 2025 RED III implementation deadline. This had raised questions about whether higher RED III targets and the removal of double-counting would apply retroactively from 1 January 2026. Most market participants now expect the changes to proceed.

In parallel, use of Pome in Germany had been under question, but it is now likely to be allowed for quota generation this year, with a ban anticipated from 2027.

With UCO-based HVO capped, traders said demand could increasingly shift toward advanced grades such as Class IV, leaving scope for further widening in the Class IV–II spread.

Beyond physical fundamentals, market structure may also be contributing to the spread widening. The Class IV increase follows last week's first trade in the Class IV paper contract. Historically, Class IV exposure has often been hedged using the Class II contract, according to participants, but traders said the newly-launched Class IV paper instrument could allow Class IV values to decouple more clearly from the Class II benchmark, supporting a wider spread.

The third quarter Class IV/Class II spread traded at +$350/t ($2,060/t, $1,710/t) on 17 April, with post trade interest described as wide. Ice launched the Argus-settled contract on 7 April. Participants can trade the contract as an outright and as a differential to front-month gasoil.

Additional support for Class IV could be coming from Indonesia, where the government said on Tuesday that fuel blenders will be required to submit plans for implementing a 50pc biodiesel–fossil diesel (B50) blending mandate from 1 July. Indonesia exports refined Pome oil to Europe and Asia-Pacific, although crude Pome exports have been restricted since January 2025. The Argus Pome oil cif ARA price rose after the news, as Indonesia may re-direct more of its Pome supply toward its biodiesel production.