How have diesel trade flows changed since 2019?

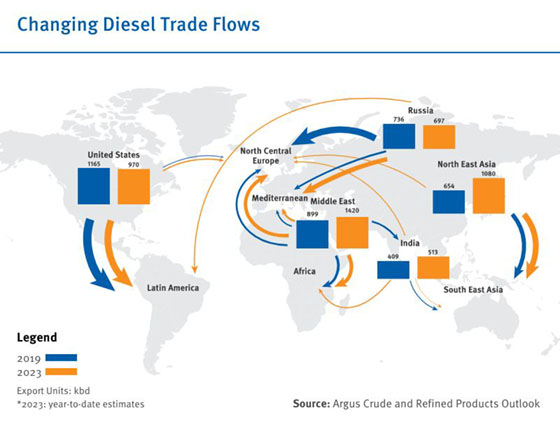

Comparing export volumes from 2019 to today reveals significant changes in diesel’s international trade flows.

New suppliers for the Atlantic basin

North and central Europe and Latin America are the major gasoil importing regions in the Atlantic basin. While the US dominates supply to Latin America, north and central Europe receive imports from a variety of sources. In 2019, the main supplier was Russia, but smaller volumes also came from the Middle East and the US.

Today the picture is very different.

Diesel imports from Russia to north and central Europe halted when the EU introduced a ban on Russian imports in early February 2023. These volumes have been replaced by imports from other suppliers, including the Middle East, Asia and the US. But Russian diesel is still flowing into the wider market largely unhindered.

Turkey has emerged as a major importer of Russian diesel, while growing volumes of Russian diesel have found their way into Latin America. There is speculation that some countries in north Africa and the Middle East may now be re-exporting Russian diesel.

As carbon reduction targets step up in the coming years, it is possible that the European refining sector will need to rationalise its capacity. Middle distillate crack spreads have typically underpinned European refining margins. Increasing global supplies and a weak long-term demand outlook may also spur further capacity closures in Europe.

Middle Eastern capacity expansions

The Middle East is a major source of gasoil exports, supplying north and central Europe, Africa, the Mediterranean and the Indian subcontinent. This export position will grow over the next few years, with the start-up of new refineries including Al Zour in Kuwait, Jizan in Saudi Arabia, Duqm in Oman and Ruwais in the UAE.

The 400,000 b/d Jizan refinery ramped up its operations last year, while the 615,000 b/d Al Zour refinery started commercial operations in November.

All these new plants are complex, with hydrocracking, refining and coking capacity and high gasoil yields. With gasoil supply forecast to exceed demand in the region, export availability is set to increase.

Steady growth for Asia

Southeast Asia is structurally short of middle distillates and is supplied mainly by refiners in northeast Asia. Exports flows have risen steadily since 2019, partly reflecting refinery closures in Australasia. New capacity has been built in Indonesia, but the region will continue to depend on northeast Asia for a significant portion of its diesel supply.

China has become an increasingly significant source of supply to regional markets, with flows determined by government-issued product export quotas. The issue or non-issue of these quotas can have a large impact on product prices and refining margins in both Asia and eventually the Atlantic basin.

Argus is following the changing diesel market closely as global trade flows shift. This summary comes from the Argus Crude and Refined Products Outlook, a monthly service providing price forecasts and valuable forward-looking market analysis to help you plan ahead effectively.

For more insights into the diesel markets, check out our European Diesel hub, where you’ll find our latest podcasts, webinars and more.