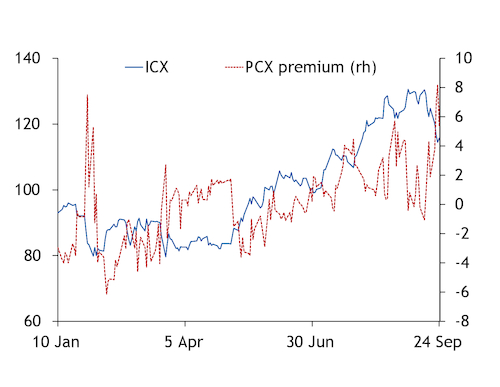

Portside iron ore premiums this week rose to a 13-month high over seaborne prices on support from pre-holiday restocking in China, while rising supply weighed on forward prices.

The Argus PCX 62pc portside fines seaborne equivalent on 23 September rose to a premium of $8.15/dry metric tonne (dmt) over the Argus ICX 62pc seaborne index, its highest premium since August 2019. The PCX index tracks 62pc fines for immediate delivery free-on-truck (fot) basis at Qingdao port, while the ICX index tracks seaborne 62pc for delivery in 2-8 weeks cfr Qingdao basis.

Iron ore prices fell sharply in September from six-year highs as fall peak steel demand was weaker than expected, and as iron ore supply began to build with rising Brazilian supply and Australian shipments showing no signs of weakening.

"Iron ore supply is likely to stay stable in the fourth quarter, and port inventories will keep increasing as China's strong demand and high prices boost shipments to China," a north China-based mill manager said.

The ICX fell by $14.85/dmt or 11pc to $115.70/dmt yesterday from a six-year high of $130.55/dmt on 3 September. It decreased as much as 12.2pc to $114.45/dmt over seven days.

The PCX at 887 yuan/wet metric tonne, or a seaborne equivalent of $121.10/dmt, fell at a slower pace, down by $9.05/dmt or 7pc over the same period.

Portside prices have received support from mills' restocking demand ahead of the 1-10 October National Day holiday in China and limited supply of certain brands including IOCJ, super-special fines and Yandi fines. But overall supply is rising to weigh on benchmark prices.

Inventories of imported iron ore at China's 45 major ports this week rose to a new five-month high for a second consecutive week, up by 1.1pc to 116.2mn t, industry data show.

Drier weather in the second half of the year enabled Brazilian mining firm Vale's shipments to recover from disruptions in from wet weather and Covid-19 lockdowns in the first half. Brazil's exporters have also diverted iron ore supply away from other regions to lift its iron ore exports to China to a new monthly high in August.

"Since August, the shipments from Vale have increased and maintained a high level at 5mn-7mn t per week. The shipments are expected to be higher, reaching or exceeding their guidance," a Beijing-based trader said. "While steel demand will be suppressed as new curbs for the heating season follow, and some mills might cut production amid poor margins. The overall supply will not be tight, and the inventory will continue to increase."

North China localities impose output restrictions from November-March to limit pollution that spikes in winter.

Iron ore deliveries from China's biggest iron ore supplier Australia have been steady after rising to a record high in June, allowing China's steel output to increase to a new record in August. Australian shipments accelerated last week.

Vale's shipments have been running recently at an annualised run rate of 330mn t/yr, a 55pc increase from May, according to a Morgan Stanley report on 23 September. "We are outright bearish iron ore, where we expect to see a surplus market from 4Q 2020, replenishing China port inventories, and a price correction," the bank said, forecasting prices of 62pc at $100/dmt cfr China in the fourth quarter and at $81/dmt in 2021.