The new line has helped push up Waha prices but has not yet influenced hubs closer to the Texas coast, writes Tray Swanson

Gas producers in the US' Permian basin have at last received pricing relief, with hot summer weather and new takeaway capacity bringing an end to a record four-month period of negative spot prices in west Texas.

The new egress capacity on US infrastructure company Kinder Morgan's 570mn ft³/d (5.9bn m³/yr) Gulf Coast Express expansion (GCX E) pipeline is the first of several projects set to ferry Permian gas to other markets in Texas this year, and part of about 11.5bn ft³/d of new capacity due to be brought on stream by 2030 to transport a flood of associated gas from the US' highest-producing oil basin (see table) .

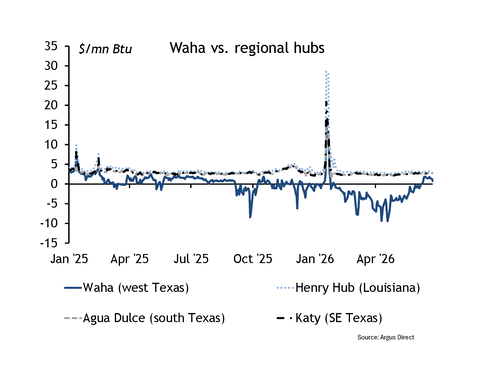

Insufficient pipeline space has frequently sent Permian prices into negative territory since 2019, with production tied to the economics of crude oil rather than gas. But the bottleneck grew particularly dire this year. The Waha hub index — the bellwether price for Permian gas output — this year had its longest run in negative territory since Argus began the assessment in 2008 (see chart: Regional prices spreads in US Gulf). Day-ahead Waha prices averaged -$3.45/mn Btu from 4 February-12 June, sinking to an all-time low of -$9.45/mn Btu on 24 April, meaning sellers without firm transport capacity had to pay buyers to take supplies.

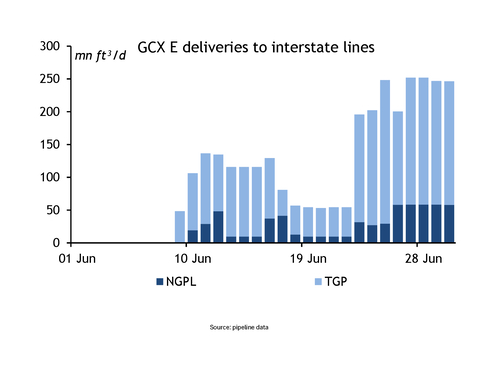

Permian gas flows can be a black box. Much of the basin's takeaway capacity is within intrastate pipeline networks so firms are not required under any federal law to disclose daily flow data. But GCX E delivers gas to two interstate lines in south Texas, so flow data are publicly available. Initial receipts from GCX E climbed throughout June, following its start-up on 9-10 June (see chart: GCX E deliveries to interstate lines), helping flip Waha prices above zero on 15 June. The reversal was aided by hot weather and the end of constraints on Kinder Morgan's El Paso Natural Gas pipeline, which shuttles Permian gas to southwest US. Waha prices have remained positive since then.

The pipeline buildout could ultimately weigh on prices at hubs closer to the Texas coast, but the marginal capacity from GCX E has not done so yet. The new flows helped narrow Waha's differential to the Agua Dulce hub, the receiving end of GCX E and a key supply source for LNG exports at the 31.4mn t/yr Corpus Christi LNG terminal and the upcoming 30.2mn t/yr Grande LNG facility. The Agua Dulce index held a $3.62/mn Btu premium over Waha in the first half of June, then it more than halved to $1.40/mn Btu in the second half of the month. But the basis tightened from Waha rising rather than Agua Dulce falling. Agua Dulce prices averaged $2.68/mn Btu in the first half of June and $2.71/mn Btu in the second half. Prices also barely moved at Katy — a key trading hub west of Houston that serves as a waypoint for Permian gas moving to LNG terminals and industrial consumers on the Gulf coast. Katy prices held a 2¢/mn Btu premium over Agua Dulce in the second half of June, consistent with the differentials before GCX E's start-up.

Key takeaways

While the positive Waha prices are a relief for Permian producers, they are not yet fully in the clear. With pipelines running full, any maintenance that occurs before the planned 4bn ft³/d of new takeaway capacity begins service later this year threatens to send prices spiralling back into negative territory.

In a survey of executives at 24 Permian-focused exploration and production firms in June, two-thirds of respondents told the US Federal Reserve Bank of Dallas that pipeline capacity will not keep Waha prices positive during maintenance until 2027. The most-selected option for capacity to reach this threshold was the first quarter of 2027, which 25pc of participants chose. No respondents expected this to occur during the third quarter of 2026, and just 13pc expect it to happen in the fourth quarter.

| Pipeline projects in the Permian basin | bn ft³/d | |||

| Project | Developer | Destination | Completion date | Capacity |

| GCX Expansion | Kinder Morgan | Agua Dulce | 2Q26 | 0.6 |

| Blackcomb | WhiteWater | Agua Dulce | 3Q26 | 2.5 |

| Hugh Brinson, phase 1 | Energy Transfer | Dallas area | 4Q26 | 1.5 |

| Hugh Brinson, phase 2 | Energy Transfer | Dallas area | 1Q27 | 0.7 |

| Wahalajara expansion | Esentia | Mexico | 1Q27 | 0.3 |

| Eiger | WhiteWater | Katy | Mid-2028 | 3.7 |

| Desert Southwest | Energy Transfer | New Mexico / Arizona | 4Q29 | 2.3 |

| Total capacity | 11.6 | |||

| — EIA, company announcements | ||||