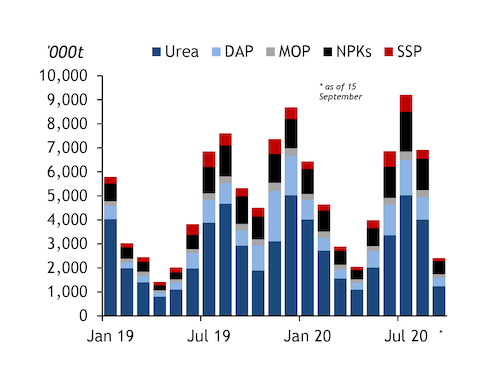

Sales of fertilizers in India are lagging last year's levels this month, continuing the trend set in August.

Domestic sales of fertilizers — urea, DAP, NPKs, MOP and SSP — totalled 2.41mn t as of 15 September, latest provisional data show. September sales last year were 5.3mn t (see chart), indicating that sales this month are set to slip below that level if the current sales rate continues.

Sales of DAP and NPKs have continued to drive offtake, with volumes of 345,000t and 555,000t so far this month, compared with September sales of 633,000t and 1.15mn t last year, respectively.

Sales of urea, the most consumed fertilizer in India, are lagging at 1.24mn t as of mid-September, compared with 2.93mn t sold in the month last year.

The overall lagging sales volumes this month follows a similar trend in August, when sales slipped to 6.9mn t, compared with 7.6mn t in the month last year. Fertilizer sales in India had outstripped 2019 levels by 42pc in January-July, before dropping in August.

The recent drop reflects the earlier onset of strong domestic offtake this year, with farmer buying accelerating from the first quarter onwards, supported by solid agricultural fundamentals and monsoon projections. Sown crop acreage this kharif season, which runs from April to September, has continued to rise, with acreage up by 5.7pc on the corresponding period last year as of 10 September.

Crop sowing has been boosted by the solid monsoon rainfall this year, from June-September, encouraging fertilizer purchases by farmers.

Average countrywide rainfall this season stands at 862mm as of today's latest data, up by 7pc on the long-term average for the corresponding period.