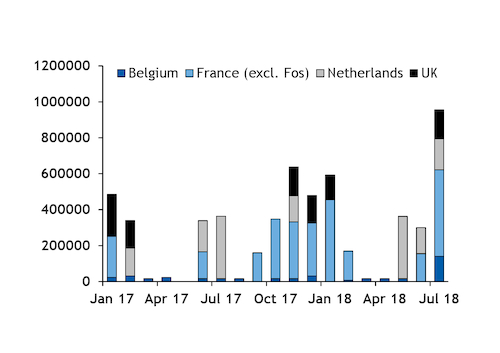

LNG re-exports from northwest Europe rose sharply in July from a year earlier given stronger premiums in Asian markets to European gas hubs. The rise was despite low spot shipping availability.

Northwest European terminals reloaded 955,000m³ of LNG in July, up from 363,000m³ a year earlier, judging by vessel size. These were the second highest reloads on record — the highest was 965,000m³ in July 2016.

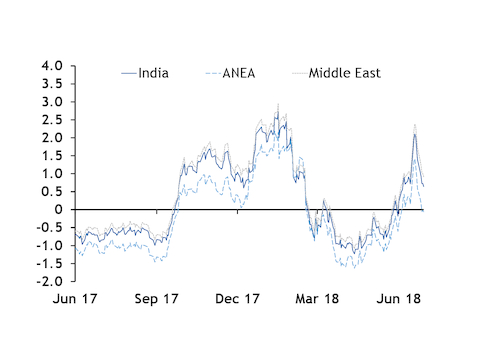

The average profit margin for a front-month reload from the Netherlands' gate terminal to India, based on Indian delivered prices and the TTF front-month market averaged 60¢/mn Btu in June. The equivalent near-curve margin a year earlier had been minus 76¢/mn Btu. India imported a significant portion of July northwest European reloads. The profit margin assumes spot shipping costs and terminal fees.

And prices across Asian markets were driven higher in particular by strong Chinese demand increasing competition for spot cargoes.

Charters tighten the spot shipping market

Northwest Europe reloaded more LNG in July than in any month over last winter, potentially because of firms increasing their term shipping capacity.

The highest number of reloads last winter was 638,000m³ in November. This was lower than in July despite higher potential profit margins from shipping to premium markets in Asia.

Terminal capacity holders in northwest Europe as well as other trading firms may have had greater shipping capacity to reload cargoes in July than during the winter.

The delivery of vessels to the market in the first half of the year combined with some liquefaction project delays increased aggregate spot shipping availability compared with the winter. Some firms with an interest in reloading cargoes from northwest Europe took the opportunity to book these vessels on term charters, shipowner Gaslog said last week. These firms had missed similar reload opportunities last winter, Gaslog said.

This had the consequence of again tightening the spot shipping market — spot rates for west of Suez dual-fuel diesel electric vessels rose above last winter's highs — but it left firms with capacity in northwest Europe more able to perform reloads.

US producer Cheniere was said to have been looking to perform reloads in June because of production constraints at its Sabine Pass facility. And it had already substantially increased its shipping capacity last year.

Total has been left with an LNG portfolio this summer that is "a little bit long" following its acquisition of French utility Engie's LNG business, the major's chief executive Patrick Pouyanne said. Total was using reloads to help manage the length in its portfolio and was using the shipping capacity it had gained from Engie.