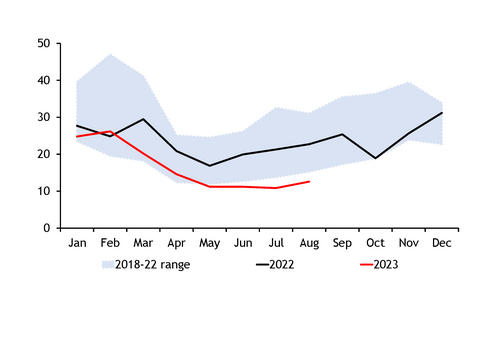

European hard coal-fired generation fell on the year in August because of lower power demand in key markets, high carbon prices and a continued coal-gas fuel switch. But coal-fired generation recovered from the multi-year low in July and is likely to rise in line with season trends towards the end of the third quarter.

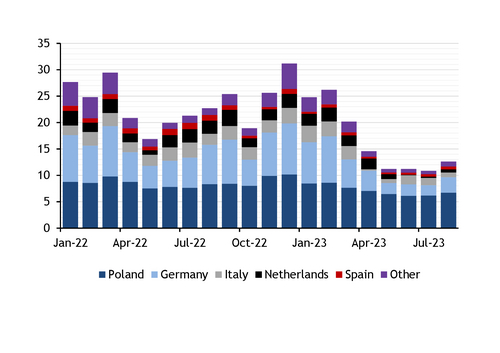

Hard coal-fired generation in key European markets — Poland, Germany, Italy, Spain, France, UK, Ireland, the Netherlands, Denmark, Finland, Croatia and the Czech Republic — fell by 45pc on the year to 12.6GW in August, grid operator data compiled by Argus show.

Generation of 12.6GW is equivalent to 3.5mn t of NAR 5,800 kcal/kg coal burnt in 40pc-efficient plants. August 2022's generation of 24.3GW is equivalent to 6.7mn t of burn.

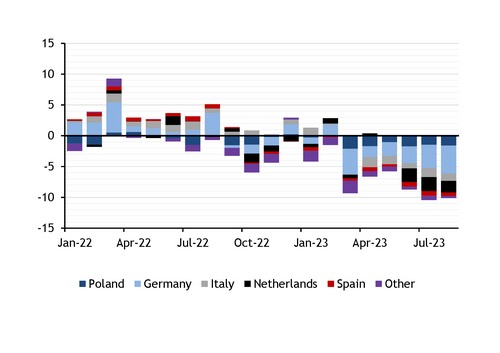

The largest on-year fall in Europe's coal-fired generation in absolute terms was in Germany, where hard coal output fell by 49pc — or 4.5GW — to 2.92GW. This coincided with increasing gas generation, which rose to 10.7GW from 6.1GW in August 2022.

German combined wind and solar output stood at a 2023 monthly low of 18.1GW in August, or 34pc of the generation mix, according to Fraunhofer ISE. Despite the low renewable output, higher electricity imports from neighbouring countries kept German coal and gas-fired generation margins under pressure in August.

Working day-ahead clean dark spreads for 40pc-efficient coal plants remained well below zero at an average of minus €14.11/MWh in August, compared with minus €16.42/MWh in July. And working day-ahead clean spark spreads for a 55pc-efficient gas plant averaged €4.86/MWh in August, down from €7.56/MWh in July.

Poland the largest coal generator

Poland continued to dominate European hard-coal generation in August, with the country generating 6.73GW from imported and domestically produced hard coal, although this was down on the year by 12pc.

The large drop in coal-fired output, compared to the previous year, is partly due to increased onshore wind and solar generation, which averaged 1.7GW and 2.2GW, respectively, in August — around 54pc and 29pc above production in August 2022. Gas-fired generation was also higher year on year, averaging 1.2GW, compared to just 600MW in August 2022.

Persistently high European emissions trading system (ETS) allowance (EUA) costs, and falling power prices have led to less favourable operating margins for coal-fired power plants. The December 2023 EU ETS price averaged €85.99/t CO2 in August, compared with €87.99/t CO2 for the December 2022 contract in August 2022.

Italy was Europe's third-largest hard-coal power generator in August, producing 0.89GW, down by 69pc on the year.

Italian power demand softened considerably in August from a month earlier, owing to cooling temperatures and lower business activity during the Ferragosto holiday season.

Italian power consumption declined by 7GW on the month to 29.3GW, also below 31.8GW in August last year. The sharp on-month decline was mainly due to the two-week holiday period in the middle of August that reduced business activity, although lower cooling demand may have contributed as temperatures fell.

Lower demand reduced the call on Italian gas-fired plants, with generation decreasing by 1.4GW from July to just 9GW, well below the 13.4GW in August 2022. And coal-fired output fell sharply on the year following the coal-gas fuel switch, firm renewables output and the Italian energy ministry's decision in July to roll back its coal and oil "maximisation" plan by reducing coal plant despatches.

Spanish and Dutch hard coal-fired generation in August fell by 53pc and 77pc on the year to 0.56GW and 0.59W, respectively. Some of the Dutch output will include biomass co-firing.

Coal-fired generation from the UK, Ireland, Finland and France fell by a collective 30pc to 0.28GW, from 0.4GW last year.

Aggregate European January-August generation of 16.5GW is equivalent to 35.4mn t of NAR 5,800 kcal/kg coal burnt in 40pc-efficient plants, 28pc lower than the estimated January-August 2022 hard coal burn of 49.6mn t.

European coal supply fundamentals

Coal stocks at Amsterdam-Rotterdam-Antwerp ports currently sit just below 6mn t — elevated by historic standards, while imports have adjusted lower in the face of soft demand.

Coal stocks in Poland have also been building, with the power-sector fines market particularly oversupplied. Mine-mouth stocks in Poland are north of 3mn t, while power plant inventories have climbed above 7mn t.

EU27+UK seaborne thermal coal imports were 5.3mn t in August and 6.2mn t in July, down by 28pc and 21pc on the year, respectively, provisional vessel-tracking data show.

EU27+UK aggregate January-June imports were 32.6mn t, up from 31.8mn t in January-June 2022, Eurostat figures show.

Kazakhstan became Europe's largest supplier in June, taking a 21pc share of total European imports, according to Eurostat data. Firm Polish purchases of Kazakh coal, combined with lower overall European imports, resulted in Kazakhstan leading European imports, likely for the first time ever.