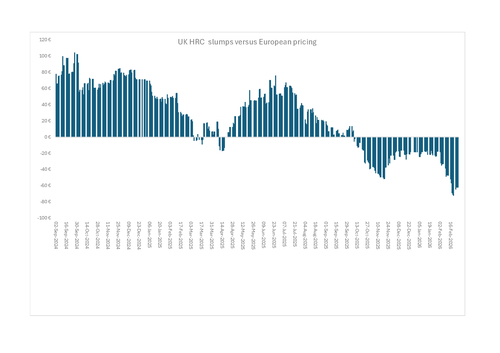

UK hot-rolled coil (HRC) prices have flipped to a large discount versus north European prices since Tata Steel UK closed its last blast furnace in September 2024.

Argus' UK HRC assessment has traded at an average discount of €62/t ($73/t) to the benchmark north EU HRC index this week. The actual price gap would be even bigger as the UK assessment is effective including extras, whereas the north EU index is base and would need extras and delivery charges added on top.

Several factors have likely driven the increasing disparity. The gap has jumped considerably this year, likely because the EU's Carbon Border Adjustment Mechanism (CBAM) has increased the cost of importing into the EU, translating into higher domestic and import prices.

UK imports of HRC have jumped considerably since Tata stopped its last blast furnace on 30 September 2024. Imports rose from around 770,000t in 2023 to 1.1mnt in 2024 and 1.4mn t last year.

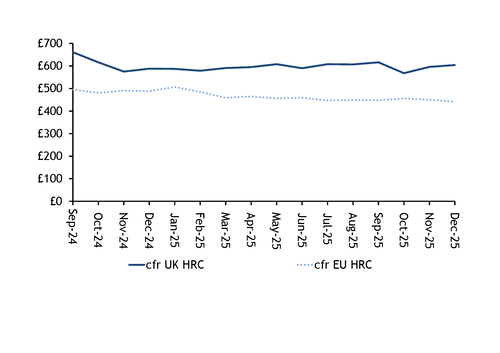

European import prices, on average, are lower than into the UK (see chart). UK values are skewed somewhat by expensive laser-plate clearing as HRC. But the cost of UK imports would typically be lower than the cost of production, given the age of Tata's assets and the fact the country is an exceptionally high-cost jurisdiction for iron and steelmaking.

Some point to competitive prices from a local producer as one factor depressing the UK market — its prices are currently closer to £540/t ddp, whereas some of its EU counterparts are pushing for — but not obtaining — as high as £600/t ddp.

Weak sheet prices are also more of a constraint in the UK than Europe, despite consolidation and high-profile failures in the service centre market in recent years. Some decoilers and service centres are still selling cut sheet at £540-550/t ddp in the UK, whereas north European prices are around £635/t ddp, while even higher prices are being achieved in southern Europe.

European mill sources, bemoaning the gap, suggest they could effectively buy coil or sheet from the UK, and profitably sell it back into the EU market. Some traders are flipping to sheet sales into the EU from coil already, because, in some instances, dumping duties can be negated.

The current price gap and malaise mean there could be an arbitrage to do this with UK material too, an avenue several will likely try to explore.