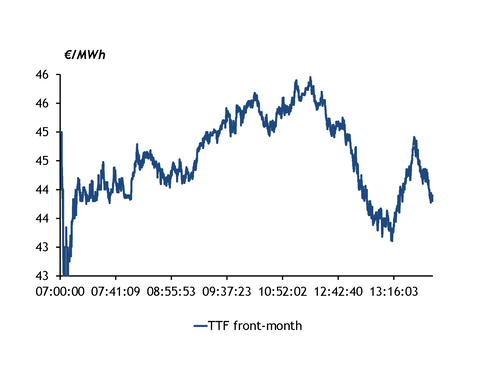

Near-term prices at the Dutch TTF gas hub fell in today's morning trading session on news of a two-week ceasefire between the US/Israel and Iran and efforts to resume LNG production in Qatar.

The front-month price opened at €42.90/MWh, 18pc lower than the previous day's close, after the US and Iran agreed to a two-week ceasefire of attacks. The price then rose above €45/MWh as traders corrected their positions, after the initial TTF open was seen as too low, market participants told Argus. The front-month contract then plunged at 13:15 BST on Bloomberg news that QatarEnergy was mobilising efforts to resume and ramp up LNG production at Ras Laffan, prompted by the ceasefire announcement, and the possibility of reopening the strait of Hormuz.

Trump said he would "suspend the bombing and attack of Iran for a period of two weeks", subject to co-operation from Iran. Iranian foreign affairs minister Seyed Abbas Araghchi said that "for a period of two weeks, safe passage through the strait of Hormuz will be possible via co-ordination with Iran's armed forces and with due consideration of technical limitations".

The front-month contract stood at €43.425/MWh at the time of writing, its lowest since 27 February, but well above the €31.51/MWh on 27 February — the day before the conflict started. But despite the reduced prices pointing to a potential easing of supply, it is unclear whether the US and Iran will honour their agreement, as the US has already bombed an Iranian oil refinery since the ceasefire was announced.

The TTF May price has dropped the most of any contract, as keeping the passage via Hormuz open in the coming two weeks could allow LNG cargoes to arrive to Europe from May at the earliest. And even if the cargoes were delivered to Asia, stronger supply in the Pacific could reduce that region's appetite for Atlantic basin spot cargoes, in turn leaving more of this LNG available for Europe.

Winter price remains at a discount to summer months

The ceasefire news weighed more heavily on contracts for summer delivery than on the winter 2026-27 price.

A potential return of LNG supply transiting the strait of Hormuz to the global balance would result in more available supply in Europe over the summer. That said, the supply outlook for this summer remains tight because of competition with Asia during Qatar's production ramp-up and structurally lower LNG output from Ras Laffan due to earlier attacks. And it is unclear if the ceasefire will extend past the two-week mark. That said, summer contracts' premiums to the coming winter have narrowed throughout today's session, with the May-winter 2026-27 spread narrowing by about €0.70/MWh from the previous close (see table).

The EU has net injected 614 GWh/d over 1-7 April, and storage sites stood at 28.8pc full. Storage sites entered the gas summer at its lowest fill level since 2022, and have to be 90pc full by 1 October-1 December to meet EU-mandated filling targets. Abundant LNG supply over the rest of the summer could aid the filling task, and alleviate some of the pressure on the summer months' contracts.

Further out, the 2027 contract was at €35.84/MWh at about 14:00 BST, 12pc lower than on Tuesday's close at €40.905/MWh. This could point to easing concerns over tight supply over coming years. The 2028-30 yearly contracts also fell, but the fall was less stark.

| Summer month-winter spreads | €/MWh | |

| Contracts | Argus close on 7 April | Ice trading on 8 April* |

| May-winter 2026-27 | 1.380 | 0.683 |

| June-winter 2026-27 | 1.470 | 0.853 |

| July-winter 2026-27 | 1.435 | 1.015 |

| August-winter 2026-27 | 1.355 | 0.848 |

| September-winter 2026-27 | 1.245 | 0.848 |

| *closest spread taken at the time of writing | ||

| — Intercontinental exchange (Ice), Argus | ||