The New Styrene Landscape as China Reshapes Trade

China’s surge in styrene production has reversed trade flows and reduced import reliance, creating oversupply pressures and forcing global producers to rethink strategy.

China’s rapid industrial growth has reshaped global petrochemical markets. This study of styrene supply and demand illustrates the impact of China’s rapid expansions in the last ten years.China’s surge in styrene production has reversed trade flows and reduced import reliance, creating oversupply pressures and forcing global producers to rethink strategy.

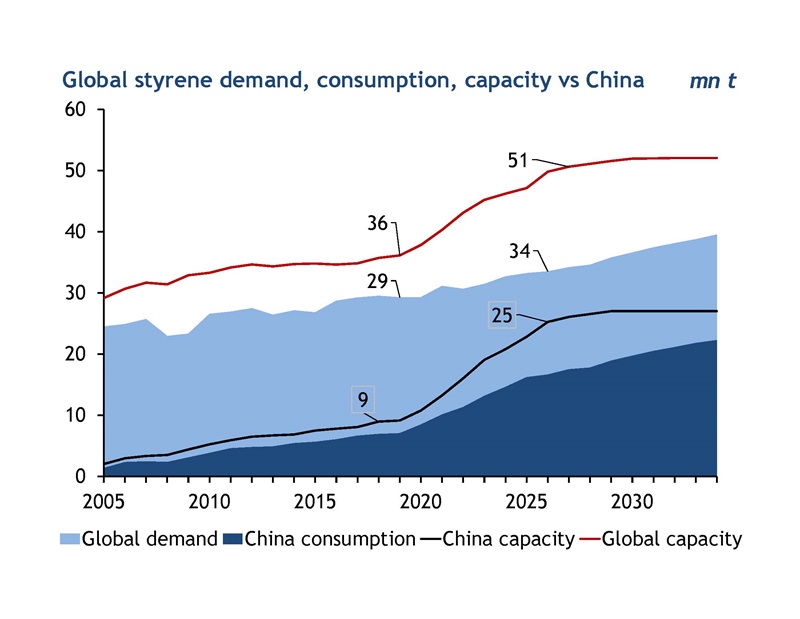

While Chinese styrene demand grew much faster than the global market, its capacity and production grew even faster. This change marks a clear shift: the world no longer relies on China as a styrene importer; the country is now a major exporter. This has resulted in China moving from a minor player to a key price influencer in the market.

Twenty years ago, China made up only 6pc of global styrene demand. Today, the country accounts for almost half of total demand.

While global demand has grown moderately, China’s demand has surged. This sharp rise has reshaped trade flows and influenced investment decisions. It reflects China’s broader industrial growth in sectors such as electronics, home appliances, building materials, and auto parts. Many of these rely on polystyrene (PS), expanded polystyrene (EPS), acrylonitrile butadiene styrene (ABS), and styrene-butadiene rubber (SBR).

Global demand for styrene is growing at a slower pace than other chemicals. It is a mature product and already widely used. Demand also faces pressure from environmental concerns. Some styrene‑based products, such as polystyrene, are being replaced by other materials.

In the last five years, China has more than doubled its styrene production capacity. A wave of new plants puts over half of the world’s total styrene capacity in China today.

This rapid expansion served several goals. China wants to reduce its reliance on imports and secure key chemicals for its factories. By linking raw materials and finished products, it keeps more value at home. Higher self‑supply also lowers the risk from global supply shocks.

This new balance has led to excess supply. Many producers outside China now run at lower rates. Companies around the world are also rethinking where and how they invest for the future.

-Data from GTT

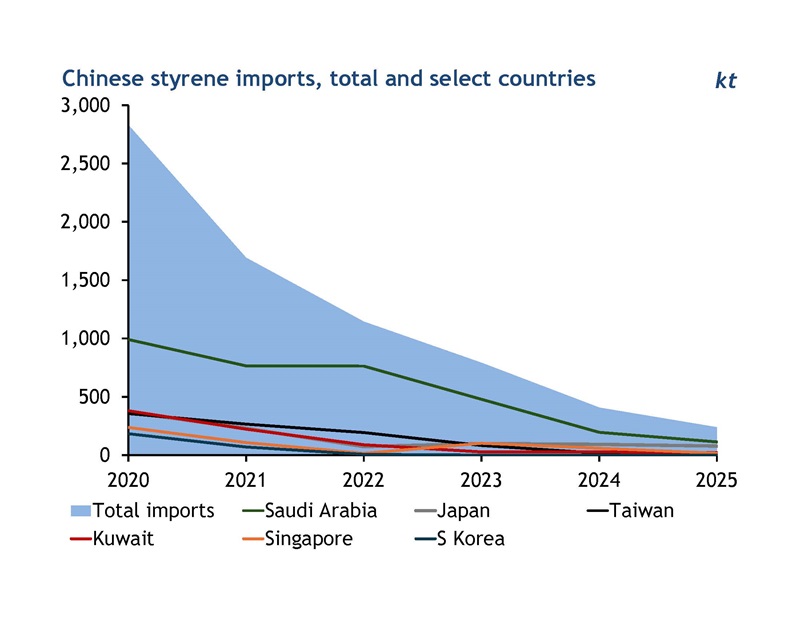

At their peak, Chinese styrene imports made up almost 14pc of global demand. Exporters in South Korea, Taiwan, the Middle East, and parts of Europe depended on China as their main market.

As China increased its own production, import needs dropped quickly. This left a clear gap in global demand. Producers that once sold mainly to China had to find new buyers. Export‑focused styrene producers now face lasting oversupply, weak pricing power and lower profits.

In response, companies are changing direction. Producers in the Middle East are turning increasingly to India, where they benefit from short shipping routes and low‑cost feedstocks. South Korea has started to cut excess petrochemical capacity with a goal of better efficiency and long‑term strength.

Japan also faces pressure. Still, some companies see this as a chance to reset. One example is Asahi Kasei. The company plans to exit the styrene‑butadiene (SB) latex business, ending production at Kawasaki. The site will pivot to synthetic rubber and ion‑exchange membranes to support growth areas such as hydrogen.

In conclusion, this case study of styrene shows how state‑led industrial growth in China has reshaped petrochemical markets in a short timeframe. Companies have been forced to adapt. Looking ahead as styrene capacity growth slows in China, producers can find their footing in the new reality.

Author name: Santosh Navada, Senior Analyst, Chemicals