Weight of Freight: TMX spurs new Aframax, VLCC trade in Pacific basin

The first three months of Canada's Trans Mountain Expansion (TMX) have sent a surge of crude to refiners in California and China, shifting tanker demand in the Pacific basin.

The 590,000 b/d TMX project nearly tripled the capacity of Trans Mountain’s pipeline system to 890,000 b/d when it opened on 1 May, linking Alberta's oil sands to Canada's west coast for direct access to lucrative Pacific Rim markets, where buyers are eager for heavy sour crude.

Between 20 May, when the first TMX cargo began loading, and 20 August, about 165,000 b/d of Vancouver crude exports landed at ports on the US west coast, primarily in California, up from about 30,000 b/d in that same span last year, according to data from analytics firm Kpler.

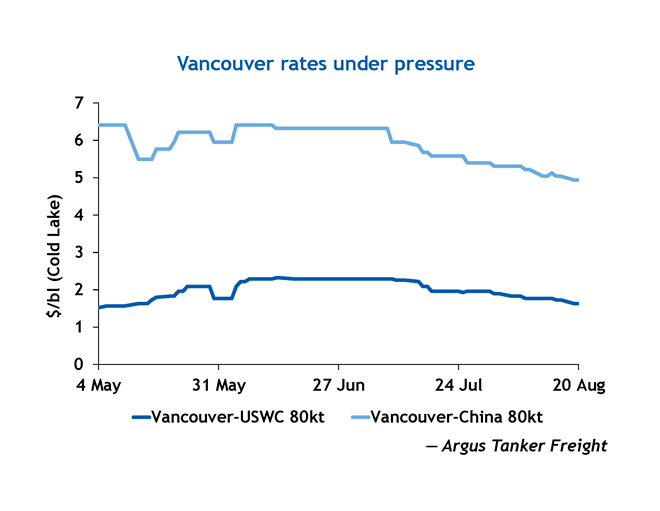

The freight rate for a Vancouver-US west coast Aframax shipment averaged $1.98/bl for Cold Lake between 1 May and 20 August. This ranged from a low of $1.50/bl from 1-3 May when shipowners repositioned to the region in anticipation of TMX to a high of $2.32/bl from 13-14 June, according to Argus data.

The new oil flow into the US west coast has displaced shipments from farther afield in Ecuador and Saudi Arabia. Crude exports from those countries into the US west coast averaged 110,000 b/d and 25,000 b/d, respectively, between 20 May and 20 August, down from 155,000 b/d and 135,000 b/d over the same stretch in 2023, according to Kpler.

The growth of the Vancouver market, which benefits from its proximity to California, has reduced tonne-miles, a proxy for tanker demand, into the US west coast. This has outpaced slightly lower crude demand, which fell in part due to Phillips 66 halting crude runs at its 115,000 b/d refinery in Rodeo, California, in February to produce renewable fuels, as well as weaker-than-expected road fuel demand this summer.

Tonne-miles for US west coast crude imports fell by 14pc to 106bn between 20 May and 20 August 2024 compared with the same period a year earlier, Vortexa data show, while overall crude imports declined just 8.6pc to 1.37mn b/d, according to Kpler.

PAL-ing around with VLCCs

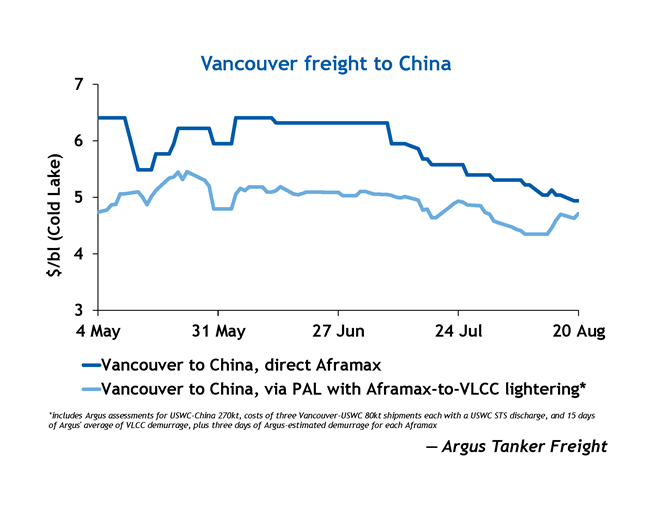

Though much of Vancouver’s exports have been shipped to the US west coast, Canadian producers have found ready buyers in Asia-Pacific as well, where about 160,000 b/d of Vancouver exports went between 20 May and 20 August, compared with none a year prior, Kpler data show.Buyers and sellers have displayed a preference for using ship-to-ship transfers onto very large crude carriers (VLCCs) at the Pacific Area Lightering zone (PAL) off the coast of southern California, rather than sending Aframaxes directly to refineries in east Asia. Of the 30 Vancouver-origin Aframax cargoes that have landed in China, South Korea and India, 19 were transferred onto VLCCs at PAL, Kpler data show. Seven cargoes were sent directly to east Asia on time-chartered Aframaxes — the majority by Suncor — and just four were sent using spot tonnage, likely due to the expensive economics of trans-Pacific Aframax shipments.

The Vancouver-China Aframax rate between 1 May and 20 August averaged $5.90/bl, with a low of $4.94/bl from 19-20 August and a high of $6.41/bl from 1-10 May and again from 4-12 June, according to Argus data.

Over the same time, the cost to reverse lighter, or transfer, three 550,000 bl shipments of Cold Lake crude from Vancouver onto a VLCC at PAL averaged about $8.055mn lumpsum, or $4.92/bl, with a low of $4.35/bl from 8-13 August and a high of $5.45/bl on 22 May, according to Argus data. This includes $150,000 ship-to-ship transfer costs at PAL, 15 days of VLCC demurrage and three days of Aframax demurrage for each reverse lightering.

VLCC costs could change preferences

Though it may have been cheaper to load TMX crude on VLCCs at PAL since May, volatility in the VLCC market — which often falls to yearly lows in summer before climbing to seasonal highs in the winter — could entice traders to opt for direct Aframax shipments if VLCCs hit their expected peak in the winter.

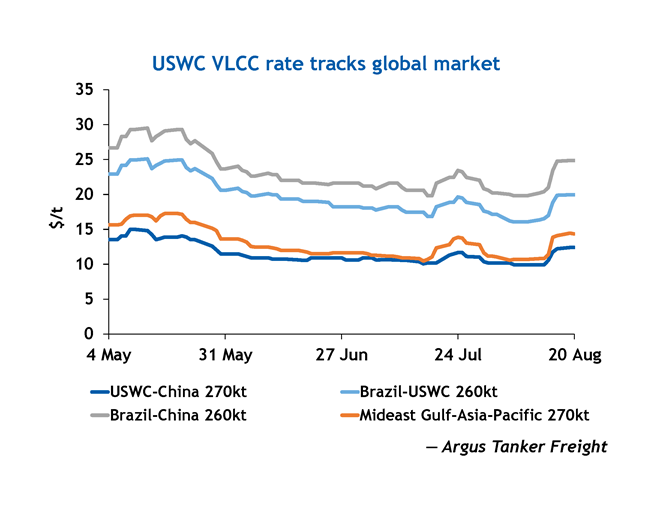

VLCC costs for shipments from the US west coast to China are influenced by the VLCC markets in the Mideast Gulf and Brazil, where ships look for their next voyage after discharging on the US west coast.

For now, Vancouver-loading Aframax rates are under pressure from the reemergence of VLCCs in what had become an Aframax trade in Thailand, boosting Aframax supply in the Pacific and pulling the class’s rate to ship crude from Vancouver to the US west coast to its lowest level in more than three months on 19 August.

In mid-July, VLCCs resumed discharging via single point mooring (SPM) at Thailand's port of Map Ta Phut for the first time since January 2022, ship-tracking data from Vortexa show. Prior to the SPM's return to service, VLCCs could discharge cargoes only by lightering onto smaller Aframaxes, which would then unload at a different berth in the port.

This created demand for about eight Aframax lighterings each month, but with VLCCs in Thailand again able to discharge directly, that demand is effectively halted, putting downward pressure in the broader southeast Asia Aframax market.

Since July, two Aframaxes have left the southeast Asia market for Vancouver, according to ship tracking data from Kpler: the Eagle Brisbane, which previously was used in lightering operations at Map Ta Phut, and the Blue Sea, which recently hauled fuel oil from nearby Singapore to China.

Spotlight content

Related news

US-assisted Hormuz transits drop to zero

US-assisted Hormuz transits drop to zero

New York, 22 July (Argus) — Vessel traffic through the strait of Hormuz on the US-assisted southern transit route stopped completely in the past day following increased Iranian attacks on vessels at the start of the week. Out of the 10 vessels that transited the strait of Hormuz on 21 July, eight vessels took the Iran-favored northern transit route, while two vessels transited through the center transit lane where most traffic passed before the war, data from vessel tracking service Windward shows. Vessel traffic through the center transit lane has been uncommon since the breakout of the war because of suspected Iranian-placed mines throughout the area. Commercial traffic through the strait of Hormuz since the outbreak of the war on 28 February has been bifurcated between the northern route, which runs along the Iranian coastline, and the southern route along the Omani coast. Transits through the US supported southern traffic lane has been steadily falling following the reprisal of attacks between the US and Iran and slowing traffic through the strait. On 20 July only two vessels out of 15 that transited the strait used the southern transit lanes, according to Tradewind data. This is down sharply from 24 June, the day when vessel transits through the strait of Hormuz reached their highest since the signing of the US-Iran memorandum of understanding that temporarily stopped the fighting, with 25 out of the 41 outbound vessels transiting the strait doing so on the southern lane. The UK Trade Maritime Organization (UKTMO) reported three attacks on tankers transiting through the strait of Hormuz between 20 and 21 July, all occurring in the southern transit lane. Centcom did not respond to a request for comment on whether the US was still offering assistance for commercial vessels looking to transit via the southern lane. Iran amps up Hormuz rhetoric, operations Iranian politicians on Wednesday reaffirmed their commitment to controlling the strait of Hormuz, likely in response to President Donald Trump's vow to bomb Iranian power plants and bridges every time Iran strikes commercial ships in Hormuz. The Iranian Revolutionary Guard Corps (IRGC-N) reiterated its position that it controls the strait of Hormuz via a social media post on X today. "The input and output of the strait of Hormuz are specified and under our definitive control," the IRGC-N said. "Alternative routes are unsafe and dangerous; we warn against their use, as it will have severe and irreparable consequences." "We have repeatedly said that the situation of the strait will not return to pre-war conditions," said Iranian parliamentary speaker Mohammad Bagher Ghalibaf, who headed previous negotiations with the US, in a 22 July post on X. Iranian actions to control traffic in the strait are also evolving. Satellite imagery shows the tanker Kavomaleas , part of Greek shipowner Dynacom's fleet, has been seized by Iran and brought to Iranian waters near Larak. The vessel was attacked by Iranian forces on 20 July , with the crew confirmed safe, according to UKTMO. This is the first reported instance of a vessel attacked by Iran in the strait of Hormuz getting escorted into Iranian waters. "A large IRGC fast in-shore attack craft presence plus one small craft positioned directly alongside the tanker is assessed consistent with an escorted move toward Iranian waters rather than an uncontrolled drift," Windward said. By Charlotte Bawol Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Oil futures: WTI up on supply disruption concerns

Oil futures: WTI up on supply disruption concerns

Houston, 21 July (Argus) — US benchmark WTI crude futures advanced today on mounting concerns over supply disruptions caused by the conflict in the Middle East. August Nymex WTI rose by $1.68/bl to $84.91/bl while September Ice Brent rose by $1.79/bl to $91.01/bl. The September Brent-September WTI spread narrowed by 7¢/bl to $6.67/bl. WTI at the Magellan East Houston terminal was discussed at a prompt 25-35¢/bl premium bid-ask spread to the Cushing benchmark at 3pm ET, according to the Argus Crude Market Ticker, above Monday's 17¢/bl volume-weighted average premium. Vessels are continuing to violate a US blockade on Iranian ports, while commercial traffic through the strait of Hormuz remains overwhelmingly controlled by Iran, despite US official's claims to the contrary. The US Central Command (Centcom) said it redirected seven commercial vessels and disabled one to prevent ships from leaving or entering Iranian ports as of 20 July. US president Donald Trump on Tuesday told reporters during a meeting with Lebanese president Joseph Aoun that the blockade is "like a steel wall" and that no ships are getting through. But data from vessel tracking service Vortexa shows that nine vessels departing or heading to Iran ports have transited through the strait of Hormuz since the US blockade was reimposed on 14 July. Separately, several large tankers on 21 July turned away from voyages passing Yemen's coastline or the Bab el-Mandeb strait in the Red Sea, according to AIS data. Three were very large crude carriers (VLCCs) and one was an Aframax. All had either loaded, or were going to load, crude at Saudi Arabian Red Sea ports. This comes a day after the Yemen-based, Iran-backed Houthis militant group said it imposed a maritime ban on Saudi Arabia. The Houthis today said six ships had turned back, although that could not be verified. Elsewhere, CPC Blend crude loadings remain suspended following recent drone attacks on tankers at the Caspian Pipeline Consortium (CPC) terminal on Russia's Black Sea coast, traders say. Loadings were halted on Monday after the tanker Nelsa was hit while loading at the terminal's SPM 1 single-point mooring buoy. Nymex RBOB rose by 1.69¢/USG to $3.4059/USG while Nymex ultra-low sulphur diesel rose by 0.76¢/USG to $4.1266/USG. By Stephen Cunningham Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Iranian vessels violate blockade, transit Hormuz

Iranian vessels violate blockade, transit Hormuz

New York, 21 July (Argus) — Vessels are continuing to violate the US imposed blockade on Iranian ports while commercial traffic through the strait of Hormuz remains overwhelmingly controlled by Iran, despite US official's claims to the contrary. The US Central Command (Centcom) said it redirected seven commercial vessels and disabled one to prevent ships from leaving or entering Iranian ports as of 20 July. And today US president Donald Trump told reporters during a meeting with Lebanese president Joseph Aoun that the blockade was "... like a steel wall" and that no ships were getting through. But data from vessel tracking service Vortexa shows that nine vessels departing or heading to Iran ports have transited through the strait of Hormuz since the US blockade was reimposed on 14 July. Of those nine vessels, six were empty inbound tankers that hold a combined carrying capacity of around 2.35mn bl of crude and refined products. Commercial vessels transiting the strait of Hormuz have also overwhelmingly continued to use the Iranian-favored northern transit route, following an increase in attacks on vessels using the US-sanctioned southern traffic lane that runs along the coast of Oman. Out of 11 strait of Hormuz transits into the Mideast Gulf on 20 July, 10 were through the northern, Iranian-controlled route while only one transited the southern, US-supported corridor, according to data from vessel tracking firm Windward. Of the vessels exiting the Mideast Gulf, three utilized Iran's northern route on 20 July and one used the southern route. Iran-flagged vessels were also the most common vessels crossing the waterway on 20 July, accounting for six out of 15 total transits, per Windward data. Vessel traffic through the strait remains at around 11pc of prewar levels, according to Windward. "US-assisted commercial transits continued with fewer ships, reflecting heightened operator risk assessments under the elevated threat environment," the UK Trade Maritime Organization said in its 21 July advisory note. "Recent attacks on tankers in Omani waters further influenced operator behavior and contributed to significantly reduced traffic density." By Charlotte Bawol Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

EU recommends three-year pause on methane penalties

EU recommends three-year pause on methane penalties

Brussels, 20 July (Argus) — The European Commission today issued formal recommendations that EU states should not apply penalties for non-compliance with the bloc's methane emissions regulation for three years, from 2027 to 2029, citing a provision in the law to avoid supply disruptions. The commission said all obligations under the methane regulation, adopted in 2024, remain in place and that compliance is still required. The regulation covers methane emissions from imports of oil, gas and coal, as well as domestic production, transport and processing. Implementation for imports begins with methane monitoring requirements from 1 January 2027. One recommendation provides guidance on compliance solutions for importers and on EU state criteria for assessing these solutions. The commission said there is no requirement for physical tracing of molecules, deliveries or cargoes. Firms can use "trace and claim" and "certification" solutions. The second recommendation lays out the three-year suspension of fines by EU states for non-compliance. A senior EU official said industry has perceived the regulation's flexibility on penalties as "uncertainty", adding that "companies cannot really factor in the risk of non-compliance because they do not know what penalty they would be facing in those member states that have not yet established penalties regimes". Even if non-binding, the official said, national courts must take the recommendation into account. "This is both true for the compliance solutions as well as for the penalties," the official said, adding that the security of supply situation justifies not applying penalties for three years, except where there is "deliberate" fraud. Commission executive vice-president Teresa Ribera last week rejected an outright pause to the methane regulation, but said security of supply concerns may justify using an existing flexibility provision in the law on penalties. In June, 16 EU states called for a three-year delay to implementation of the regulation, noting that a recommendation is "non-binding and therefore does not remove significant legal uncertainty for importers negotiating long-term supply contracts". Industry groups FuelsEurope and IOGP have also pushed for a pause to the regulation. Dafydd ab Iago Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.