Weight of Freight: TMX spurs new Aframax, VLCC trade in Pacific basin

The first three months of Canada's Trans Mountain Expansion (TMX) have sent a surge of crude to refiners in California and China, shifting tanker demand in the Pacific basin.

The 590,000 b/d TMX project nearly tripled the capacity of Trans Mountain’s pipeline system to 890,000 b/d when it opened on 1 May, linking Alberta's oil sands to Canada's west coast for direct access to lucrative Pacific Rim markets, where buyers are eager for heavy sour crude.

Between 20 May, when the first TMX cargo began loading, and 20 August, about 165,000 b/d of Vancouver crude exports landed at ports on the US west coast, primarily in California, up from about 30,000 b/d in that same span last year, according to data from analytics firm Kpler.

The freight rate for a Vancouver-US west coast Aframax shipment averaged $1.98/bl for Cold Lake between 1 May and 20 August. This ranged from a low of $1.50/bl from 1-3 May when shipowners repositioned to the region in anticipation of TMX to a high of $2.32/bl from 13-14 June, according to Argus data.

The new oil flow into the US west coast has displaced shipments from farther afield in Ecuador and Saudi Arabia. Crude exports from those countries into the US west coast averaged 110,000 b/d and 25,000 b/d, respectively, between 20 May and 20 August, down from 155,000 b/d and 135,000 b/d over the same stretch in 2023, according to Kpler.

The growth of the Vancouver market, which benefits from its proximity to California, has reduced tonne-miles, a proxy for tanker demand, into the US west coast. This has outpaced slightly lower crude demand, which fell in part due to Phillips 66 halting crude runs at its 115,000 b/d refinery in Rodeo, California, in February to produce renewable fuels, as well as weaker-than-expected road fuel demand this summer.

Tonne-miles for US west coast crude imports fell by 14pc to 106bn between 20 May and 20 August 2024 compared with the same period a year earlier, Vortexa data show, while overall crude imports declined just 8.6pc to 1.37mn b/d, according to Kpler.

PAL-ing around with VLCCs

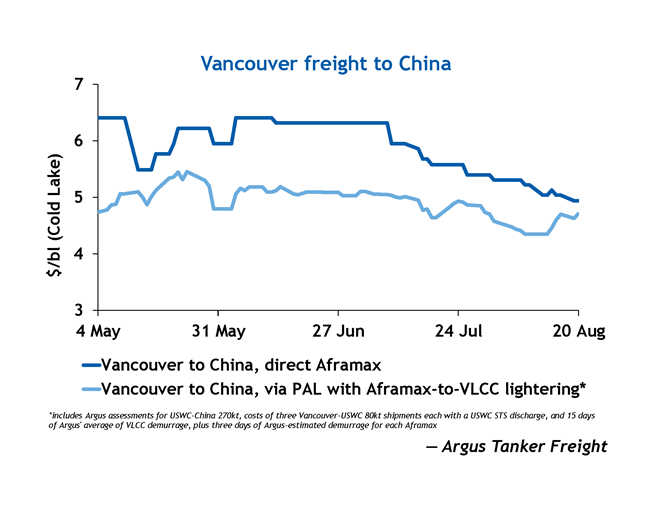

Though much of Vancouver’s exports have been shipped to the US west coast, Canadian producers have found ready buyers in Asia-Pacific as well, where about 160,000 b/d of Vancouver exports went between 20 May and 20 August, compared with none a year prior, Kpler data show.Buyers and sellers have displayed a preference for using ship-to-ship transfers onto very large crude carriers (VLCCs) at the Pacific Area Lightering zone (PAL) off the coast of southern California, rather than sending Aframaxes directly to refineries in east Asia. Of the 30 Vancouver-origin Aframax cargoes that have landed in China, South Korea and India, 19 were transferred onto VLCCs at PAL, Kpler data show. Seven cargoes were sent directly to east Asia on time-chartered Aframaxes — the majority by Suncor — and just four were sent using spot tonnage, likely due to the expensive economics of trans-Pacific Aframax shipments.

The Vancouver-China Aframax rate between 1 May and 20 August averaged $5.90/bl, with a low of $4.94/bl from 19-20 August and a high of $6.41/bl from 1-10 May and again from 4-12 June, according to Argus data.

Over the same time, the cost to reverse lighter, or transfer, three 550,000 bl shipments of Cold Lake crude from Vancouver onto a VLCC at PAL averaged about $8.055mn lumpsum, or $4.92/bl, with a low of $4.35/bl from 8-13 August and a high of $5.45/bl on 22 May, according to Argus data. This includes $150,000 ship-to-ship transfer costs at PAL, 15 days of VLCC demurrage and three days of Aframax demurrage for each reverse lightering.

VLCC costs could change preferences

Though it may have been cheaper to load TMX crude on VLCCs at PAL since May, volatility in the VLCC market — which often falls to yearly lows in summer before climbing to seasonal highs in the winter — could entice traders to opt for direct Aframax shipments if VLCCs hit their expected peak in the winter.

VLCC costs for shipments from the US west coast to China are influenced by the VLCC markets in the Mideast Gulf and Brazil, where ships look for their next voyage after discharging on the US west coast.

For now, Vancouver-loading Aframax rates are under pressure from the reemergence of VLCCs in what had become an Aframax trade in Thailand, boosting Aframax supply in the Pacific and pulling the class’s rate to ship crude from Vancouver to the US west coast to its lowest level in more than three months on 19 August.

In mid-July, VLCCs resumed discharging via single point mooring (SPM) at Thailand's port of Map Ta Phut for the first time since January 2022, ship-tracking data from Vortexa show. Prior to the SPM's return to service, VLCCs could discharge cargoes only by lightering onto smaller Aframaxes, which would then unload at a different berth in the port.

This created demand for about eight Aframax lighterings each month, but with VLCCs in Thailand again able to discharge directly, that demand is effectively halted, putting downward pressure in the broader southeast Asia Aframax market.

Since July, two Aframaxes have left the southeast Asia market for Vancouver, according to ship tracking data from Kpler: the Eagle Brisbane, which previously was used in lightering operations at Map Ta Phut, and the Blue Sea, which recently hauled fuel oil from nearby Singapore to China.

Spotlight content

Related news

Saudi Arabia, Turkey and Pakistan sign defence pact

Saudi Arabia, Turkey and Pakistan sign defence pact

London, 7 August (Argus) — Saudi Arabia, Turkey and Pakistan signed a joint defence pact in Mecca today. The agreement aims to "strengthen collective defence" and "stipulates that any armed attack against any one of the three states shall be regarded as an attack against them all", according to a joint statement. The deal follows a period of heightened instability in the Middle East centred around the US-Iran war. Saudi territory, including its oil and gas assets, has been repeatedly attacked by Iran and Iran-backed groups in Iraq and Yemen since the start of the war. It remains unclear what the defence pact commits the three states to in the event of any attack. Turkey was also targeted in the war's early stages. The agreement aligns three Sunni-majority Muslim countries closer together, with each bringing different strengths. Saudi Arabia is Opec's leading member and one of the world's largest oil producers, giving it significant financial power. Turkey has Nato's second largest army and has developed a strong defence industry in recent years, while Pakistan is the world's fifth most populous country and has nuclear weapons. Some analysts see the emerging alliance as a reaction to destabilising moves in the region by the US and Israel on the one hand and Iran and its proxies on the other. It follows an earlier defence pact signed between Saudi Arabia and Pakistan in September. By Aydin Calik Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

UAE’s Adnoc expands tanker fleet in $1.3bn deal

UAE’s Adnoc expands tanker fleet in $1.3bn deal

Dubai, 7 August (Argus) — Abu Dhabi state-owned Adnoc's logistics arm has agreed to acquire 11 tankers for $1.3bn, expanding its crude and LPG shipping capacity as the UAE prepares for higher oil and gas exports. The acquisitions comprise six very large crude carriers (VLCCs), each capable of carrying around 2mn bl of oil, and five very large gas carriers (VLGCs). The additions will increase Adnoc Logistics and Services' crude tanker fleet to 14 vessels and its gas fleet to 12. Nine of the vessels were acquired on the secondary market and are due for delivery this quarter, with two newbuild VLGCs acquired through a Chinese shipyard due to follow in the fourth quarter. The VLCC acquisitions come as Adnoc prepares for higher crude exports, with the UAE targeting oil production capacity of 5mn b/d by 2027. They could give the company greater control over deliveries at a time when the US-Iran conflict has disrupted traffic through the strait of Hormuz and tightened tanker availability. Adnoc's 1.8mn b/d Adcop pipeline running from Habshan to Fujairah has provided a partial bypass of the strait since the war began. The company plans to expand the pipeline's capacity to around 3.3mn b/d by 2027, freeing up more crude for export from Fujairah. The latest acquisitions extend a rapid expansion of Adnoc's shipping business. Last month, Adnoc Logistics and Services ordered four LNG carriers worth about $900mn ahead of the planned 2028 start-up of Adnoc's 9.6mn t/yr Ruwais LNG export terminal. The company also added 32 tankers to its fleet through last year's $1.04bn acquisition of an 80pc stake in Navig8. By Rithika Krishna Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Trump promises Hormuz deal 'soon'

Trump promises Hormuz deal 'soon'

Washington, 6 August (Argus) — President Donald Trump again said on Thursday that a deal to reopen the strait of Hormuz to navigation is imminent, even though Tehran appears to be insisting on major concessions from Washington. "I am involved in the negotiations," Trump told reporters at the White House, adding that "we're doing fine" and that a deal could be concluded "very soon". Trump may have been referring to the dialogue between Iran and Oman when he began on 2 August to reference ongoing talks with Iran that he said would result in reopening Hormuz within a day or two. Iran and Oman are close to issuing a joint statement specifying "geographical co-ordinates" of a safe transit route through Hormuz, Iran's foreign ministry said on Wednesday. But Tehran is demanding the lifting of the US blockade and other concessions from Washington. The deal with Oman "by itself would not make Hormuz safe for transit", Iran's foreign ministry said. The US naval blockade remains in place, and the strait of Hormuz is "sort of open right now", Trump said on Thursday. But he acknowledged that threats posed by Iran are deterring many shippers from using the Mideast Gulf waterway. "We control it, but they can always shoot something, or drop a mine, and if you have one mine sitting out there, you sort of mess things up because people don't want to take their billion-dollar boats and accidentally get hit by a mine," he said. Trump, who has been expressing unease about elevated energy prices, said on Thursday that "oil prices now are coming down very rapidly, it's down to $75/bl". September Nymex WTI rose by $2.07/bl to $77.29/bl on Thursday, bouncing higher after steep losses earlier in the week. Vessel traffic through the strait of Hormuz on Wednesday remained confined mostly to the Iranian-favored northern traffic lane, with maritime security firm Windward recording nine inbound transits and 11 outbound transits, with two transits in both directions taking place on the US-supported southern traffic lane along the coast of Oman. Iran continues to exert pressure on commercial shipping through the strait by attacking intermittently and by issuing warnings to vessels. A tanker transiting north toward the strait of Hormuz on Wednesday reported two loud explosions in its vicinity, leading it to alter its course and abort transit, according to the UK Trade Maritime Operations (UKTMO). Iran's forces on Thursday confronted "hostile enemy targets" near the Qeshm island in the strait of Hormuz, said Iranian news agency Tasnim, which is tied to the Islamic Revolutionary Guards Corps. The report did not detail whether any vessel came under attack. The Iranian claim has not been independently verified. By Haik Gugarats Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Venezuela's July oil production at 1.2mn b/d

Venezuela's July oil production at 1.2mn b/d

Caracas, 6 August (Argus) — Venezuela crude production reached 1.221mn b/d in July, an increase of 11pc from a year earlier but a dip of 3pc from June, according to state-owned PdV data seen by Argus . The figures include condensates, natural gas liquids and other byproducts. Venezuela is still reeling from twin earthquakes that killed thousands on 24 June. Even if the damage mostly spared the oil industry, acting President Delcy Rodriguez warned Venezuelans on Wednesday night that more trouble lies ahead. A hotter-than-usual August that Rodriguez attributed to the El Nino climate phenomenon means possible further rationing of water and electricity. Frequent power outages and delays in restarting service to earthquake-hit areas has led to protests that expanded to the affected Los Palos Grandes neighborhood on Wednesday evening, joining protestors in Carabobo and other parts of Venezuela. Rodriguez's rationing warning came one day after the top US envoy to Venezuela, John Barrett, toured Venezuela's largest hydroelectric plant Guri with officials from state electricity monopoly Corpoelec. Improved electrical service to support oil production has been a key US demand since the first day of new cooperation between Washington, DC, and Caracas brought about by the violent arrest of former leader Nicolas Maduro on 3 January. PdV did not break down production figures by operational areas but gas processors' association AVPG estimated July production in western Venezuela at 361,000 b/d, higher than the 347,110 b/d the oil ministry reported in June. By Carlos Camacho Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.