Central and eastern Europe's (CEE) gas storage injections remain too slow to fully offset a year-on-year deficit, with inventories on track to reach 70pc by 1 November, as conditions diverge across countries depending on supply and storage mandates.

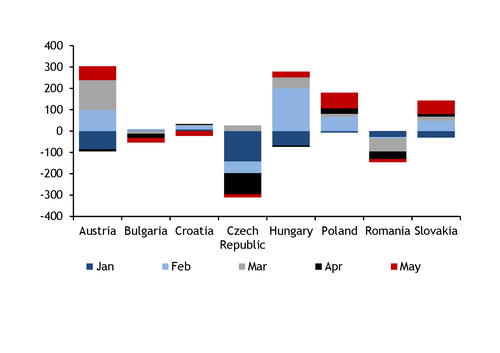

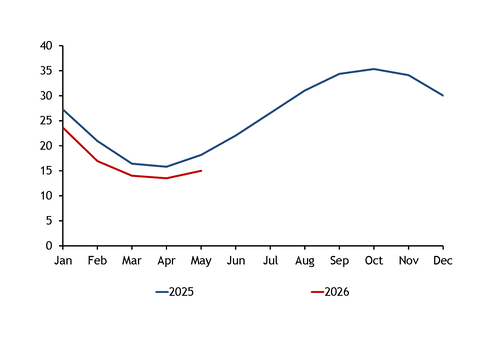

The region's average injection rate was almost unchanged on the year at 69.6 GWh/d over 1 April–25 May, compared with 68.7 GWh/d a year earlier. This kept the storage deficit in place because the EU ended winter with much lower stocks than a year earlier. Austria recorded the largest year-on-year shortfall at 7.6TWh, followed by the Czech Republic at 5.1TWh and Slovakia at 2.5TWh on 26 May, GIE transparency platform data show (see stocks graph). The combined inventory deficit in Austria, Bulgaria, Croatia, the Czech Republic, Hungary, Poland, Romania and Slovakia was 15.7TWh on 26 May.

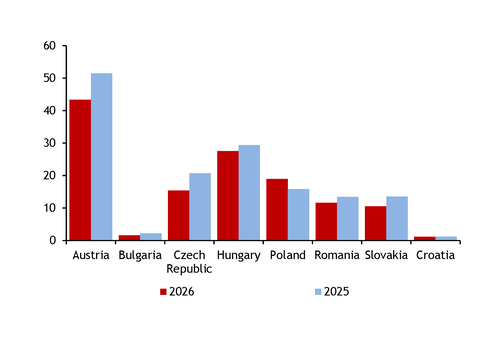

If current year-on-year differences in injection rates hold through the summer, the regional storage fill could reach 70pc by 1 November, down from 82pc a year earlier. Injection patterns vary as national storage mandates and supply portfolios influence filling strategies. Assuming that the summer stockbuild remains at the same deficit to last year in the coming month, storage in Poland is on track to reach capacity in early October, while Slovakia, Hungary, Austria and Romania are projected to reach 80pc on average by 1 November, and 60pc in the Czech Republic. In contrast, Bulgaria and Croatia are on track to reach only 26pc.

National storage obligations accelerated stockbuilding earlier this year in some CEE countries by setting mandatory deadlines. Hungarian and Slovak law require certain market participants to build storage reserves in domestic facilities. And the Czech Republic targets 60pc fill by 1 September and 90pc by 1 November.

Poland's stockbuild rose by around 50 GWh/d on the year on 1 April–26 May, with Slovakia up by 42 GWh/d and Hungary by 18 GWh/d, partially offsetting earlier storage deficits (see injections graph). Assuming this injection pace, storage in these countries could exceed last year's levels and stay above 80pc by 1 November.

Stable supply portfolios have supported these gains, as the countries rely on long-term pipeline deals and offshore production. Hungary and Slovakia remain highly dependent on gas via Turkish Stream, while Poland's supply portfolio includes a substantial share of Norwegian gas. These flows tend to remain stable throughout the year, with interruptions mostly limited to scheduled maintenance.

Prague on track to miss target

The Czech Republic faces the highest risk of missing its target unless it sharply accelerates injections in the second half of the summer.

Czech injections slowed by 58 GWh/d on the year on 1 April–25 May, and in Bulgaria by 20 GWh/d, which may increase reliance on imports later in summer. Bulgaria and Croatia also have limited storage compared with demand and rely heavily on LNG imports.

The persistently weak stockbuild and low inventories in the Czech Republic could widen the year-on-year gap further. At the current trajectory, storage could hold at around 28TWh, or 60pc, by 1 November — well below the 90pc target.

The Czech Republic is very dependent on LNG, leaving it exposed to global competition and cargo diversions to higher-priced markets. Czech state-controlled utility Cez has booked 3bn m³/yr of LNG capacity at the Dutch 8bn m³/yr Eemshaven terminal to the end of October 2027. This covers almost half the country's annual demand last year, showing its growing reliance on LNG. This setup may limit availability and increase both price volatility and supply risk despite secured regasification capacity.