Corrects reason why Turkish scrap prices rebounded in paragragh 2

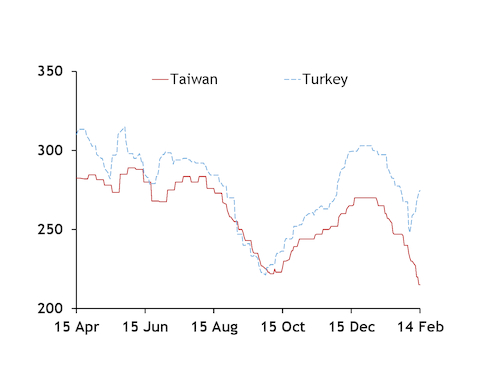

Seaborne bulk and containerised ferrous scrap prices have diverged this month with the coronavirus compounding Taiwan's growth struggles while Turkish steel demand rebounds.

Turkish scrap prices have rebounded on reduced availability for March shipments compared with February, at the same time as mills were aware of pent-up domestic steel demand in Turkey and demand was also expected from the US and the Middle East. Asia-Pacific steel producers still face weak domestic demand, narrowing margins and price pressure from falling Chinese prices.

Prices for Turkish bulk imports and Taiwanese containerised imports usually follow each other, with a 70-80pc correlation between them over the past two years. This year they have parted ways.

The HMS 1/2 80:20 cfr Turkey price has risen by 11pc from a recent low of $248/t on 5 February. The HMS 1/2 80:20 cfr Taiwan price has fallen by 20pc, or around $50/t, from a high of $270/t on 6 January.

The Turkish import price this month has risen by 2.7pc, or $7.20/t, to $274.70/t. The Taiwanese import price has fallen by 10.4pc, or $25/t, to a three-year low of $215/t.

The contrast has left Asian bulk buyers resistant to rising offers, while Taiwan has been able to buy at lower levels.

Vietnam buyers said they were surprised by the fall in Taiwanese import scrap price last week because bulk prices to Turkey and Vietnam increased by more than $10/t.

US bulk offers of HMS 1/2 80:20 to Vietnam rose to $280/t cr last week from $268/t cfr the previous week. Japanese exporters raised offers for HS to $270/t and rejected bids at $263/t last week that were in line with the last deal on 7 February. The latest H1/H2 50:50 scrap offer from Japan to Taiwan was at $231/t cfr.

Domestic rebar prices have fallen in Vietnam, adding pressure to scrap buyers' margins. But Vietnamese bulk buyers have fewer supply options compared with containerised scrap, giving them less bargaining power. Asian bulk buyers for now are choosing to delay purchases, as they expect a price correction in the short term. Their reluctance is borne out in the actual deals done that show an intact downtrend for Japanese scrap into South Korea, Vietnam and Taiwan. The last deals done for H2 was at ¥22,000/t fob Japan, HS at $263/t cfr Vietnam and H1/H2 50:50 at $234/t cfr Taiwan.

Japanese mills are making output cuts, which could divert more Japanese scrap supplies to seaborne markets. Japanese domestic scrap prices are also falling.

Tokyo Steel has lowered its domestic scrap seven times in three weeks in response to poor domestic demand for accumulated cuts of ¥4,500-5,000/t across grades and mills.

The main issue for Asian steel producers outside of China is the threat of the coronavirus outbreak curtailing demand and spilling over into markets beyond China and Asia. The possibility of China exporting excess supplies has already emerged, a trend that if it continues could start to affect Turkish scrap and steel prices.