A contango in spot LNG prices over the second half of this year suggests buyers with oil-linked supply agreements could be encouraged to push these volumes from June-September into the fourth quarter.

Weak prompt oil prices in recent weeks have left oil-linked pricing curves in backwardation through much of the remainder of 2020. These are typically used to price term LNG and gas supply by using a set percentage slope of the average oil price of the previous three or six months — termed 301 and 601 contracts, respectively.

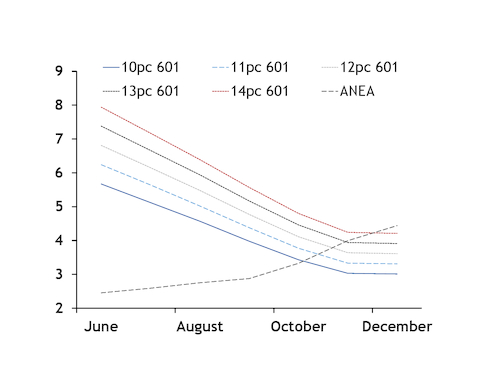

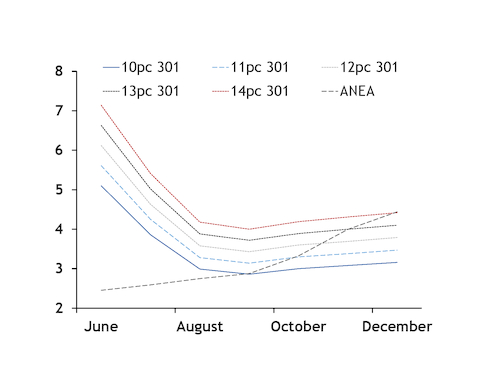

Both curves are often used to price LNG supply agreements in the Pacific basin, with 301 curves yesterday in backwardation until October, and 601 curves for the remaining months this year. This backwardation has offered an incentive for buyers with oil-linked LNG supply to defer term volumes into later this year.

The backwardation in 301 curves against the contango in Argus northeast Asia (ANEA) des prices means ANEA prices hold their widest discount to oil-linked curves in June-September. This suggests that at prevailing prices firms may be able to maximise returns by deferring their term cargoes scheduled for June-September delivery into the fourth quarter and sourcing spot volumes over the four months to meet their selling commitments.

The firms could then cut down spot purchases in October-November as they lift term receipts, when ANEA prices are at a tighter discount to the 301 curves, or at a premium in some cases.

This could weigh on spot LNG demand in the fourth quarter — a period when such demand has historically been highest in a calendar year, and spur spot purchasing over the third quarter, typically a weaker period for spot demand.

Spot LNG prices remain below most 301 curves

ANEA prices remained below most oil-linked delivered prices for October-November yesterday, suggesting there may be little incentive for firms to increase 301-priced contractual volumes above minimum take-or-pay thresholds until December.

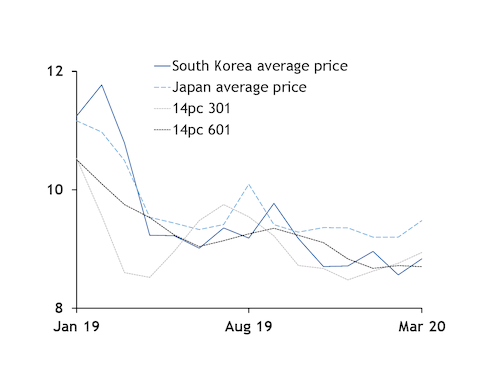

Buyers in Japan and South Korea typically pay above 13pc of average oil prices, although percentages vary by contract.

The ANEA October price remained at a premium to the 11pc slope 301 curve yesterday, but at a discount to the 12pc curve. And the ANEA November price held parity with the 13pc 301 curve.

But the ANEA December price retained a small premium to the 14pc 301 curve yesterday, suggesting there could be limited incentive for firms with 301 contracts priced below 14pc to choose greater term supply than spot volumes.

But a number of firms pay less than a 12pc slope for their supply, such as state-owned buyer Pakistan LNG (PLL), which pays 11.62pc and 11.95pc for its contractual volumes from trading firm Gunvor and Italy's Eni, respectively. For these firms, there would be an incentive to cut their contractual volumes for delivery in the third quarter even further, and displace them with greater spot purchases. This would leave them with a higher proportion of term LNG to take in the fourth quarter to meet minimum take-or-pay thresholds, but with spot prices potentially above the cost of their term supply, it would incur a lower cost to take these additional term volumes compared with sourcing spot cargoes.

Weak spot prices in recent months may have meant that term buyers sought to cut their contractual take to minimum take-or-pay thresholds, allowing them to make up their requirements with significantly cheaper LNG. With spot December prices at a premium to some of these contracts, firms could be incentivised to increase their contractual takes and cut their spot purchasing for December.

Higher contractual sales from export projects could also weigh on spot supply in the Pacific basin, helping offset weaker spot demand in the region. And with global liquefaction capacity growth set to slow in the second half of this year and into 2021, the volume of spot cargoes available because of trains starting commercial operations could also fall from recent years.

ANEA forward rises further above 601 curves

The backwardation in 601 curves, which held for delivery throughout the rest of 2020 yesterday, provided a similar incentive for buyers to defer June-September supply to the fourth quarter.

But the 14pc 601 curve held further below the ANEA December price, suggesting a greater incentive for firms holding 14pc 601 contracts to cut their term supply in the third quarter to avoid spot purchases in the fourth, mirroring the incentive for firms paying a lower percentage on 301 curves.