A demanda de etanol hidratado projetada para março e abril deve aumentar significativamente em relação ao mesmo período em 2023, à medida que o biocombustível continua ganhando competitividade contra a gasolina na bomba.

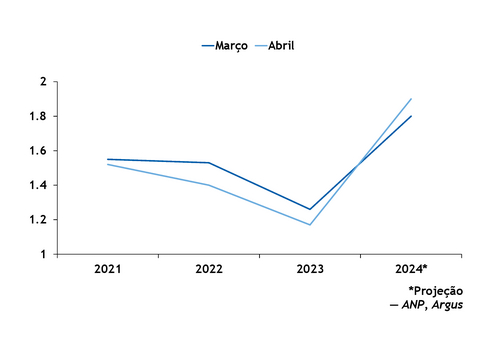

A expectativa é que o consumo do hidratado cresça cerca de 54,6pc em março em relação ao mesmo intervalo do ano passado, atingindo 1,8 milhão de m³, de acordo com uma pesquisa feita pela Argus com participantes de mercado – incluindo distribuidoras, corretoras e consultoras de biocombustíveis.

Uma fonte apontou que o volume consumido no mês pode alcançar até mesmo 2 milhões de m³, graças à procura intensa.

O maior número de dias úteis e o mercado aquecido impulsionarão a busca crescente pelo produto. A paridade de preços em todos o país frente ao combustível fóssil ficou, em média, em 69pc em março até a semana encerrada no dia 16. Em São Paulo, a relação está em 61pc.

O etanol precisa ter um preço de 70pc ou menos do que a gasolina para ser competitivo e atrair a atenção dos motoristas na hora de abastecer.

Já em abril, o consumo do biocombustível deve subir aproximadamente 55,6pc na base anual, para 1,9 milhão de m³, segundo o mesmo levantamento da Argus.

Participantes de mercado esperam uma paridade ainda mais favorável para o mês, com ampliação da defasagem do preço da gasolina.

Avanço do ciclo deve elevar preços

Entretanto, a tendência de crescimento da demanda pelo hidratado não deve se prolongar por toda a safra de cana-de-açúcar de 2024-25, afirmam players consultados pela Argus.

Com o avanço do ciclo, que começa em 1 de abril, o fornecimento pode não ser suficiente para atender à procura, direcionando produtores a elevarem preços para equilibrar oferta e demanda - provavelmente, isso acontecerá no meio do ano.

Esse é o cenário mais provável pois a próxima temporada não deve se igualar aos níveis recordes registrados em 2023-24. Integrantes do mercado estimam que o volume deve ficar, em média, entre 590 milhões de t e 620 milhões de t, dependendo do nível de chuvas até o fim de abril.

O Centro-Sul deve encerrar a safra atual com 650 milhões de t, de acordo com estimativa da Organização de Associações de Produtores de Cana do Brasil (Orplana). A previsão está em linha com os 647 milhões de t calculados pelo relatório mais recente da União da Indústria de Cana-de-Açúcar e Bioenergia (Unica) para o acumulado até o fim de fevereiro.

Paralelamente ao possível aumento de preços no decorrer do ano-safra, participantes temem que uma recuperação da fatia da gasolina dentro do Ciclo Otto afaste os motoristas do hidratado por mais tempo que o desejado. "É muito mais rápido para o consumidor ir do etanol para a gasolina do que da gasolina para o etanol", comentou uma fonte de uma distribuidora.

Assim, a projeção é que o novo ciclo siga um caminho inverso do atual, que começou com o biocombustível em baixa, especialmente por incentivos tributários à gasolina herdados do governo anterior com o objetivo de controlar a inflação, e terminou com o hidratado ganhando tração.

Com a cana-de-açúcar rendendo volumes menores, o etanol à base de milho deve se destacar. Seu consumo para 2024-25 deve ficar entre 7,5 milhões de m³ e 7,8 milhões de m³, segundo especialistas consultados pela Argus. No exercício anterior, a produção de etanol hidratado de milho ficou em 5,3 milhões de m³ na região Centro-Sul, de acordo com a Unica.

Em fevereiro, a procura pelo hidratado já demonstrou estar fortalecida, com as vendas saltando 53pc em comparação ao ano anterior e marcando 1,68 milhão de m³, segundo dados da Agência Nacional do Petróleo, Gás Natural e Biocombustíveis (ANP) divulgados hoje.

Por Laura Guedes